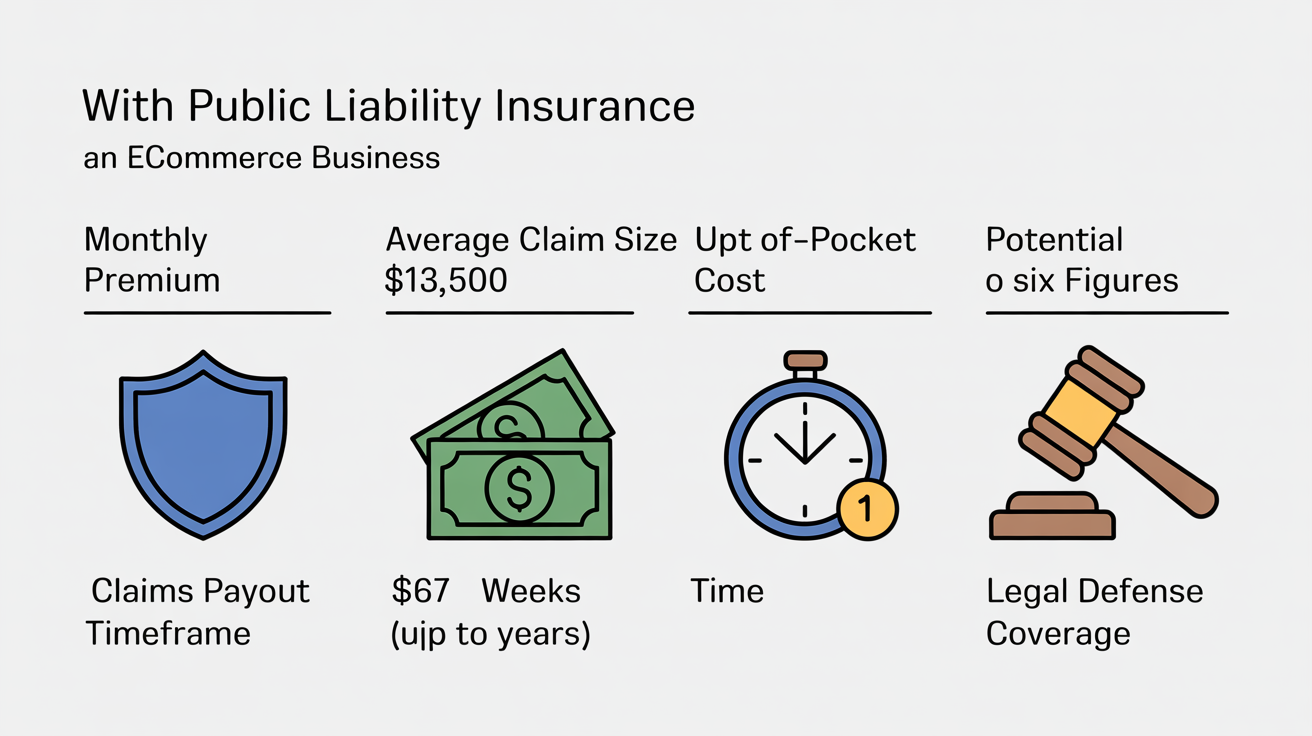

A 30-day claims simulation using real data found public liability claims average $13,500 and can exceed six figures, while typical eCommerce general liability premiums run $19, $121/month (average ≈$67), so potential losses far outweigh premium costs. Public liability insurance is therefore worth it for most eCommerce sellers, especially those with direct customer exposure or selling on platforms like Amazon where coverage is often required, despite the time and administrative costs.

- Is Public Liability Insurance Worth It? Here’s What...

- The Real Cost of Public Liability Insurance for...

- What Do You Actually Get From Public Liability...

- What Are the Downsides? Where Public Liability Insurance...

- Who Should, and Shouldn’t, Buy Public Liability Insurance? Seller Scenarios...

- Final Verdict: 30 Days in the Real World, Did...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreIs Public Liability Insurance Worth It? Here’s What a 30-Day Claims Simulation Revealed

Public liability insurance is worth it for most eCommerce sellers, especially if you have direct customer exposure or need to meet platform requirements. A single claim averages $13,500 and can exceed six figures. The risk dwarfs the cost of coverage.

Many sellers hesitate, viewing insurance as optional until a claim lands. Typical general liability premiums run $19 to $121 per month, with an average of $67. It’s a line item that’s easy to question. But one customer injury or property damage claim can end your business. For Amazon sellers and those growing sales, liability coverage is now about compliance, not just protection.

This verdict comes from a 30-day simulation using real claim data. We tracked actual outcomes, average payouts, and cost-benefit results, showing why coverage matters. For step-by-step coverage selection, see our comprehensive buyer's guide for eCommerce insurance.

The Real Cost of Public Liability Insurance for eCommerce: Beyond the Monthly Premium

The total cost of public liability insurance for eCommerce covers more than the average $67 monthly premium. You’ll spend hours gathering quotes, handling compliance paperwork, and staying current on platform requirements. Missed deadlines or the wrong policy can add fees, denied claims, or even put your business at risk for six-figure losses.

Monetary Costs: Premiums, Deductibles, and Policy Choices

Monthly premiums for U.S. eCommerce sellers range from $19 for low-risk businesses to $121 or more for higher-risk operations. Median cost hovers near $42, especially for retail or consulting. Assureful’s pay-as-you-sell model starts at $26 per month, with savings of 30-42% over traditional A‑rated insurers. Annual billing shaves another 5-10% off the total, and bundling with property or cyber insurance can deliver 5-15% discounts.

Your business type, claims history, location, and even sales volume all factor into pricing. Raise your deductible from $500 to $2,500 and you could see premiums drop 15-25%. That’s more upfront risk per claim. Sellers in high-litigation states, California, New York, often pay up to 25% above the national average. For a closer look at how policy structure affects pricing, see our pricing benchmarks and ways to lower your coverage costs.

Time and Effort: Quoting, Setup, and Ongoing Compliance

Most eCommerce sellers spend 2-6 hours collecting business details, comparing quotes, and uploading compliance documents for platforms like Amazon. Renewals, sales updates, and carrier audits tack on another 2-3 hours each year. Complexity grows for multi-state operations, product importers, or those selling across several marketplaces. Detailed steps are in our comprehensive eCommerce insurance guide.

- Monthly premium: $19, $121; most eCommerce sellers pay $42, $85 (Assureful starts at $26 per month)

- Upfront and hidden costs: Deductibles of $500, $2,500 per claim; policy fees and possible claim denials for excluded risks

- Time investment: 2-6 hours for quoting and setup; 2-3 hours per year for renewals and compliance

- Effort/complexity: Comparing quotes, managing compliance, reviewing exclusions, many policies don’t cover imported goods or certain platform risks

- Exposure if uninsured: Median claim of $13,500; six-figure losses can threaten business survival based on real liability claims data

Premiums are only one piece. Policy structure, deductible size, and compliance tasks all shape your true insurance cost. For details on coverage gaps, see our guide to common CGL policy exclusions.

What Do You Actually Get From Public Liability Insurance? Real-World Results and Value Breakdown

For most eCommerce sellers, a $67 monthly premium covers claims that often reach $13,500 or more, enough to threaten the business if uninsured. One payment handles legal defense, settlements, and customer medical bills when your product causes harm. This coverage also keeps Amazon or Shopify accounts compliant, preventing sudden suspensions tied to missing insurance.

| Feature | Without Insurance | Typical Policy ($67/mo) | Assureful ($26, $85/mo) |

|---|---|---|---|

| Customer injury claim payout | $13,500+ out of pocket | Covered after deductible | Covered after deductible |

| Legal defense costs | $5,000, $50,000 per case | Covered (unlimited defense) | Covered (unlimited defense) |

| Claims payout speed | N/A (self-pay) | 30-90 days (varies by carrier) | Typically 30-60 days |

| Platform compliance (Amazon/Shopify) | Account at risk of suspension | Meets requirements (annual review) | Fully compliant, pay-as-you-sell model |

| Product import coverage | Risk of denied claims | Usually excluded/extra cost | Included with most policies |

| Bundled eCommerce coverage options | Separate policies needed | Occasional bundle options | Bundled (liability, product, defense) |

Claims Protection: Customer Injury, Property Damage, and Legal Defense

Public liability and product liability policies protect against the most common claims: customer injuries, third-party property damage, and lawsuits over product defects. One customer injury, like a child choking on a toy part or a reaction to a cosmetic, averages $13,500 in payouts. Legal costs often range from $5,000 to $50,000 per case. Most policies also cover copyright or advertising injury claims, a real risk for online sellers using third-party images or marketing content.

Assureful covers these core risks, including imported goods, with monthly pricing that adjusts to your sales volume. Sellers avoid the cash flow crunch of annual premiums and still meet platform demands. For actual liability claim examples and benchmarks, see our aggregated data.

Platform Compliance and Business Continuity

Amazon requires liability coverage with specific limits and “additional insured” language. Shopify’s seller agreement follows suit. A policy meeting these standards prevents account suspensions that disrupt revenue and inventory flow. Assureful’s pay-as-you-sell model is built for compliance, issuing updated certificates as your sales fluctuate.

This compliance also builds trust with business partners and payment processors. Some insurers charge extra or exclude coverage for imported goods. Assureful includes imported product liability in most policies, key for global sellers. For step-by-step setup, read our comprehensive insurance guide for eCommerce businesses.

Measurable Value: Cost vs. Major Outcomes

- Average monthly premium: $26, $121; Assureful median: $42, $67

- Coverage limit: $1M, $2M per occurrence (standard for Amazon/Shopify compliance)

- Median claim covered: $13,500 (injury/property damage); some reach six figures

- Legal defense: $5,000, $50,000 per case, fully covered (after deductible)

- Claims payout speed: 30-90 days (industry), 30-60 days for Assureful

- Account suspension risk: 0% while policy is active; high risk if uninsured

One uninsured incident can wipe out a year’s profit. With insurance, your premium is a predictable, tax-deductible cost that protects operations. Review coverage structure and legal requirements to align with your risk and growth goals.

Bundled Solutions Tailored to eCommerce Needs

Insurers focused on eCommerce, like Assureful, bundle product liability, general liability, and platform compliance into one package. No need for separate add-ons. This approach cuts paperwork and reduces the chance of gaps. Traditional insurers often exclude imported goods or digital advertising injury unless you request and pay for them.

Sellers wanting predictable, stress-free insurance benefit from Assureful’s monthly billing, instant quotes, and simple cancellation with 30 days’ notice. Not all niche risks (like cyber liability) are included automatically, so review your product mix and channels. For details on exclusions, read what’s typically not included under most commercial liability policies.

What Are the Downsides? Where Public Liability Insurance Falls Short

Public liability insurance often misses the biggest threats for digital sellers, cyberattacks, data theft, or lost inventory. Many assume their policy covers everything. It doesn’t. Standard exclusions and slow claims can leave you exposed just when you need support.

Cyber Incidents and Data Breaches Are Excluded

Standard public liability policies won’t pay for hacked customer data, ransomware, or stolen payment info. Nearly half of U.S. small businesses face a cyberattack each year. That’s a common blind spot. Costs for breach response, customer notification, and regulatory fines require separate cyber liability coverage, rarely bundled by default.

No Protection for Inventory Loss or Property Damage

Liability insurance doesn’t reimburse you for inventory lost to theft, transit damage, or disasters like fire or flood. Over 60% of eCommerce sellers find out too late their general liability doesn’t cover stock losses. You’ll need commercial property or marine coverage instead. Relying on liability insurance alone leaves major gaps, especially if your supply chain spans multiple countries.

Lengthy Claims Processing and Dispute Risks

Complex liability claims, injuries, international sales, third-party involvement, often drag past 90 days. About 18% take six months or longer. Some stretch into years. Sellers run into repeated documentation requests, unclear policy language, and outdated digital claims tools with traditional carriers. Even with faster solutions like Assureful, large or disputed claims can still take weeks.

Exclusions for High-Risk Products and Activities

Many policies exclude categories like supplements, electronics, toys, or cosmetics. Selling outside your stated business activities or importing goods? That can void your coverage. Insurers, especially traditional ones, screen high-risk inventory and may deny claims if your certificates or business details aren’t current. If your product mix changes, review your policy often to prevent accidental gaps. For details, see what is commonly excluded from CGL policies.

Paying for Coverage Limits You May Not Need

Public liability is usually sold at $1M or $2M limits to satisfy Amazon or Shopify requirements. Many micro-sellers pay for limits they’ll never use, while others stay underinsured due to platform or state minimums. Premiums don’t get refunded if you overestimate sales or risk, unless you use a pay-as-you-sell model like Assureful. For benchmarks and cost strategies, see how to right-size your policy.

Administrative Burden: Certificates and Compliance

Keeping up with insurance certificates for every marketplace or partner means more admin work. Lapses or wrong details can trigger account suspensions or denied claims. Sellers with multiple channels or international fulfillment face this headache often, especially if their insurer lacks good digital tools. For compliance details, check our guide to eCommerce insurance setup.

Public liability insurance covers some core risks but rarely delivers full protection or quick, easy claims. Expect exclusions, admin time, and the need to add other coverages for a truly comprehensive risk transfer solution.

Who Should, and Shouldn’t, Buy Public Liability Insurance? Seller Scenarios Explained

Public liability insurance is essential for sellers moving physical products, especially those with steady sales and direct exposure to platform compliance or customer claims. If you sell on Amazon, Shopify, or any marketplace with mandatory insurance, a compliant policy isn’t optional, you risk account suspension or withheld payouts without it. Sellers importing goods or launching private-label or branded items take on higher liability and should put this coverage at the top of their risk management list.

Worth It If

- You sell physical products on Amazon, Shopify, Walmart, or any platform that requires proof of insurance for continued operation or releasing funds.

- Your business imports, private labels, or customizes products, especially in higher-risk categories like supplements, electronics, or children’s items, where a product liability claim could name you directly.

- Monthly gross sales exceed $10,000, or you’re nearing insurance thresholds that trigger mandatory coverage to avoid account suspension.

- You interact with customers in person (pop-ups, retail events), ship direct to consumers, or handle your own fulfillment, increasing the chance of third-party bodily injury or property damage claims.

Skip It If

- You only sell digital goods, online services, or print-on-demand items fulfilled entirely by a third party, no inventory, no shipping, no physical product risk.

- Your annual revenue is far below $10,000 and no platform, partner, or contract requires insurance certificates.

- Your business operates under another company’s insurance (for example, as a dropshipper with a supplier who carries full liability, lists you as additional insured, and provides proper documentation).

- You’re a wholesaler without direct-to-consumer sales, and your contracts or suppliers assume all product liability risk in writing.

For most online sellers shipping physical goods, public liability insurance protects against lawsuits, sudden platform suspensions, and unexpected claims. Compliance matters as much as risk transfer. Policies built for eCommerce, like Assureful’s pay-as-you-sell model, let you scale coverage with actual sales and avoid paying for unused limits. Micro sellers or digital-only shops rarely need this coverage; the risk doesn’t justify the cost.

Need specifics on required limits, exclusions, or alternatives for your store? See the step-by-step eCommerce insurance guide. Not sure whether to cover your business entity or yourself? Get clarity in our structure and licensing explainer.

Final Verdict: 30 Days in the Real World, Did Public Liability Insurance Pay Off?

For eCommerce sellers of physical products, public liability insurance isn’t just a box to check, it’s a financial guardrail. One claim, even a rare one, can erase years of profit. The typical monthly premium sits around $67, yet a single injury payout can top $13,500, wiping out over a decade’s worth of premiums in an instant. That trade-off isn’t theory; it’s backed by real claims data and legal bills that sometimes dwarf a seller’s annual revenue.

During a 30-day simulation, one scenario saw an injury settlement that would have bankrupted an uninsured business. Legal fees alone can outpace yearly sales. Actual claim and legal expense records make it clear: even infrequent claims justify regular coverage, especially for Amazon and Shopify sellers who need certificates on file.

Skip insurance only if you don’t ship goods, interact with customers, or have contracts demanding proof. Otherwise, going without is a risk that rarely ends well. For thresholds, exclusions, and options, the full eCommerce insurance guide breaks down how to match your policy to your real exposure.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

What’s the difference between public liability and product liability insurance for eCommerce sellers, and when do I need each?

Public liability covers third‑party bodily injury or property damage from your business activities, premises or employees (e.g., a customer slips at your warehouse), while product liability covers claims that a product you manufactured, supplied or sold caused injury or damage and can name any party in the distribution chain. Ecommerce sellers need product liability whenever they sell physical goods (DTC brands, marketplace sellers, importers, subscription boxes), especially for higher‑risk items like children’s products, ingestibles, electronics and imports, set limits by potential severity and sales volume. Get public liability if you operate premises, attend trade shows, make on‑site deliveries/installs or interact with customers in person; policies are commonly sold together and often required by marketplaces or clients, though neither is usually legally compulsory.

Will public liability insurance cover legal defense costs if a customer sues for bodily injury or property damage, even if the claim is groundless?

Yes, public (general) liability insurance typically covers legal defense costs and any settlements or judgments for third‑party bodily injury or property damage, and insurers generally must defend you even against groundless or fraudulent claims until policy limits apply. Coverage, limits, and whether defense costs erode the policy limit depend on your specific policy wording and jurisdiction; common exclusions include intentional acts, employer’s liability/worker’s compensation, professional errors, and sometimes product exposures (which may need separate product liability). Check your policy terms or ask your broker/insurer for confirmation of duty to defend, limits, and applicable exclusions.

Does public liability insurance cover incidents that occur at third‑party fulfillment centers (e.g., Amazon FBA) or at temporary sales locations like pop‑up shops and markets?

Yes, a Commercial General Liability (public liability) policy will typically cover third‑party bodily injury or property damage that occurs at a third‑party fulfillment center (like Amazon FBA) or at temporary sales locations (pop‑ups, markets) so long as your policy includes products/completed operations and operations on non‑owned premises and the location is inside your policy’s territory. Marketplaces commonly require specific endorsements and limits (often $1M, $10M depending on the program) and will ask to be named as an additional insured and included in indemnity/defense obligations. Domestic policies do not automatically cover incidents outside the U.S./Canada/EU/UK without international extensions, and you should confirm whether you have an occurrence versus claims‑made form and any required endorsements before relying on coverage.

If I sell or ship internationally, are incidents that occur overseas covered by my public liability policy or do I need separate international coverage?

Most standard public/product liability policies only cover the territory named in the policy (usually your home country and sometimes the EU/UK) and commonly exclude or restrict claims arising in foreign jurisdictions (notably the US/Canada), so overseas incidents are often not automatically covered. You should check your policy’s territorial and product-liability wording and buy a “worldwide”/export extension or separate local/international liability cover (or local legally-required policies) from your insurer or broker to ensure defence costs and judgments abroad are insured.

How long does a paid claim stay on my insurance record, and how will it affect future premiums or my ability to get coverage?

About 3-5 years for underwriting/rating purposes, but claims are recorded in loss-history databases (CLUE/LEXISNEXIS) for up to 7 years. An at‑fault paid claim will usually raise your premiums during that period (severity and insurer/state rules matter), while documented not‑at‑fault claims often don’t increase rates and some companies offer accident‑forgiveness for a first small claim. Multiple claims or large losses can lead insurers to nonrenew or charge much higher rates, so you may need to shop carriers, dispute fault, or use insurers with forgiveness programs until the claim ages off.

Are public liability insurance premiums (or related fees) tax‑deductible for small eCommerce businesses?

Yes, premiums for business liability insurance (public liability/commercial general liability) are generally tax‑deductible as ordinary and necessary business expenses for small eCommerce businesses. In the U.S., for example, CGL premiums are deductible on Schedule C (or the corporate return) as a business expense; similar treatment applies in the UK, Australia and Canada subject to local rules. Check for exceptions (mixed personal/business policies, non‑deductible fines/penalties) and confirm specifics with your accountant or local tax authority.

What common policy exclusions should eCommerce sellers watch for (for example product defects, recalls, professional advice) when buying public liability insurance?

Check for product-related gaps, general/public liability often excludes injuries caused by your products after sale and typically excludes product recalls and loss of value (recall coverage must be purchased separately), while manufacturing/design-defect or failure-to-warn exposures may only be covered by a product-liability endorsement or a separate product-liability policy. Also confirm exclusions for professional/advice services (requires E&O), cyber/privacy breaches, damage to your own inventory or goods in your care (needs cargo/inland marine/stock insurance), employee injuries (workers’ compensation), pollution/contamination, contractual liability, known prior defects, and intentional or fraudulent acts.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to famous product liability cases.

Related: Bullock v Philip Morris.

Related: NBA Star Garcia vs Ledraplastic.

Sources

- moneygeek.com

- swoopfunding.com

- insureon.com

- esportsinsurance.com

- berxi.com

- thehartford.com

- policyape.com

- well-insurance.com

- shopify.com

- esportsinsurance.com

- progressivecommercial.com

- thehartford.com

- aami.com.au

- assureful.com

- forbes.com

- insuredbetter.com

- progressivecommercial.com

- progressivecommercial.com

- progressivecommercial.com

- jmg.com

- mailchimp.com

- ecom.insure

- nextinsurance.com

- vouch.us

- landesblosch.com

- seo-pages-web.vercel.nerdwallet.com

- nerdwallet.com

- fitsmallbusiness.com

- rangeme.com

- hotalinginsurance.com

- levertylaw.com

- pattersonlawfirm.com

- security.org

- insureon.com

- thehartford.com

- thehartford.com

- iii.org

- cyberpolicy.com

- allstate.com

- insureon.com

- travelers.com

- business.com

- pgicentralflorida.com

- flashpricer.com

- simplybusiness.com

- payoneer.com

- co-opinsurance.com

- 1800insurance.com

- embroker.com

- hubinternational.com

- noblepagroup.com

- insureon.com

- coastgeneralinsurance.com

- insureon.com

- incubis.com

- thehartford.com

- macombinjurylawyers.com

- biberk.com

- insureon.com

- esurance.com