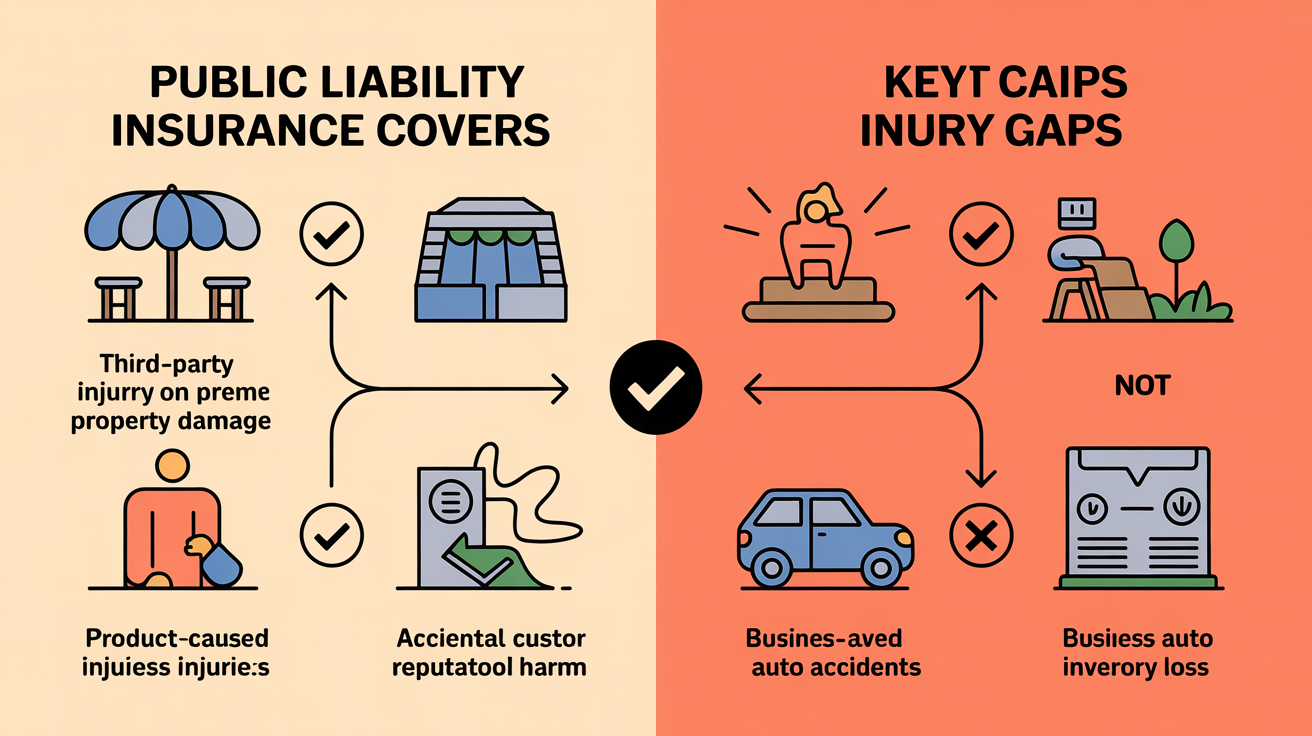

Public liability insurance covers third-party bodily injury or property damage caused by your business (e.g., slips, falls, accidental damage at a home office, pop-up, or during delivery) and pays medical costs, repairs, legal fees, and settlements that can exceed $30,000. However, policies commonly exclude product defects after sale, employee injuries, your own property damage, cyber/data breaches, and many IP disputes, e-commerce sellers must identify these gaps and purchase separate product liability, cyber, and workers’ compensation coverages.

- Public Liability Insurance: What It Covers, and Where the...

- How Public Liability Insurance Functions, and Why Exclusions Exist

- Where Public Liability Delivers, and Where It Leaves Your...

- 4 Common Myths About Public Liability Insurance, And Their...

- Key Takeaway: Know Your Policy, and Close the Gaps...

Public Liability Insurance: What It Covers, and Where the Real Gaps Lie

Public liability insurance covers your business if a third party, like a customer, delivery driver, or visitor, suffers injury or property damage because of your business activities. It pays for medical bills, repairs, legal fees, and settlements tied to incidents such as slips, falls, or accidental damage. For e-commerce sellers, this applies to accidents at your home office, pop-up locations, or deliveries, not just physical stores.

Even a small liability claim can stack up quickly. Medical costs, legal fees, and settlements often exceed $30,000. That can drain your cash flow, or force you to halt operations. E-commerce brings extra risk: online and offline exposures blur, and standard policies rarely cover digital risks or product-related injuries by default.

Most public liability policies cover third-party injuries and property damage, but they often exclude claims linked to your actual products once sold. Copyright or advertising injury claims, like using an image without permission, are sometimes covered, but product liability usually requires separate protection. To keep your business fully protected as it grows, know the coverage boundaries and check for policy gaps that leave you exposed.

How Public Liability Insurance Functions, and Why Exclusions Exist

Public liability insurance protects you if a non-employee claims bodily injury or property damage directly caused by your business. Coverage responds only when specific conditions are met, such as a customer injury at a pick-up site or accidental damage during your operations. Coverage isn’t blanket protection; every policy relies on definitions, exclusions, and risk assessment specific to how and what you sell.

What Triggers Coverage, and What Doesn’t

For public liability insurance to respond, a third party, not an employee, must suffer physical injury or property loss directly tied to your business activity. For e-commerce, this could mean a customer trips over a package at a collection point or a courier’s equipment is damaged during a delivery run.

Not every loss qualifies. Employee injuries fall under workers’ compensation. Damage to your own property? That needs a different policy. Data breaches or payment fraud require cyber insurance. Product injuries after sale usually demand separate product liability coverage.

Why Exclusions Exist, and What’s Usually Excluded

Insurers use exclusions to limit unpredictable risks and clarify what’s not covered. These carve-outs prevent overlap with other policies and manage exposures outside their control. Common exclusions for e-commerce include:

- Injuries to employees (covered by workers’ compensation)

- Damage or loss to your own inventory, equipment, or premises

- Product failures or defects that cause harm after sale

- Cyberattacks, data breaches, or payment fraud

- Intentional acts, criminal conduct, or known defects

- Intellectual property disputes unless specifically included

You’ll need separate business property or cyber insurance for those risks, based on your exposure.

How Risk Is Evaluated and Premiums Set

Insurers weigh your revenue, products, sales channels, claims history, and operations. Selling imported goods, high-risk categories like supplements or electronics, or having prior claims pushes premiums higher. With pay-as-you-sell billing, you’re charged for last month’s actual sales, no annual forecasting, no upfront lump sums. Insurance spending tracks your real activity.

Most policies start at $1 million per incident, with annual caps between $2 million and $5 million. Raising your deductible cuts the monthly bill but means more out-of-pocket if you file a claim. Choose limits based on the worst incident you could face, not just on sales volume or what’s standard in your niche.

Policy Issuing, Billing, and Compliance for E-Commerce

E-commerce insurance must keep pace with your business. With pay-as-you-sell monthly billing, you avoid upfront annual premiums and guesswork. Expanding into new categories or markets? Your premium and coverage adapt automatically to last month’s sales data.

Staying fully compliant means providing certificates of insurance and meeting marketplace minimums. Some platforms require A‑rated insurers and on-demand proof. Miss these requirements and you risk suspended selling privileges until you resolve the gap.

Where Public Liability Delivers, and Where It Leaves Your Business Exposed

Public liability insurance covers legal costs and damages if your business activities injure a customer or damage their property during daily operations. One accident, a slip in your warehouse, a dropped box, can trigger a lawsuit that drains your profits for the year. For e-commerce sellers, knowing the limits of this protection prevents gaps that lead to losses.

Protection for Accidents During Business Operations

If a visitor or courier trips over packaging at your facility, public liability covers their medical bills and your legal defense. The core advantage: immediate funds for third-party injuries or property damage linked to your premises or business activities. Example: An e-commerce seller faced a lawsuit when a courier slipped on a wet loading bay and broke a wrist. The policy paid £17,500 in claims and legal fees, protecting the seller’s annual profit.

This coverage follows you to trade fairs, pop-up events, and customer visits. Less disruption. Fewer financial shocks tied to your physical operations.

Legal Defense and Settlement Costs

Legal bills often exceed the actual damages in a liability claim. Public liability insurance pays for attorneys, court fees, settlements, and judgments if your business is found liable. That keeps your cash flow stable and business assets protected, even if the claim is dismissed.

One seller received a $35,000 legal bill after a customer tripped over extension cords during an order pickup. Insurance covered the costs, so business continued without tapping reserves or seeking emergency loans. For more incidents and outcomes, see these real ecommerce insurance claims.

Where Public Liability Stops, And Product Liability Begins

Public liability doesn’t cover injuries or damage caused by your products after they leave your control. If a charger you sold overheats and damages a customer’s home, that's product liability, not public liability. Confusing these risks leaves you exposed to claims your policy won’t handle. For a breakdown of coverage differences, see the differences between public and products liability.

- Covered: Customer slips in your warehouse and breaks an arm, public liability responds.

- Not covered: Paint you sold damages a customer’s floors, product liability applies.

- Not covered: Data breach exposes customer info, requires cyber insurance.

Exposures Beyond Standard Public Liability Coverage

Some risks sit outside public liability’s reach, cyberattacks, business property theft, employee injuries, product recalls, and professional errors all need separate policies. If your inventory is damaged or customer data is stolen, public liability won’t respond. E-commerce sellers must assess all exposures and close gaps before problems hit.

Results: less downtime, fewer uninsured losses, and clear compliance with platform demands for comprehensive business insurance.

4 Common Myths About Public Liability Insurance, And Their Hidden Costs

Many e-commerce sellers mistakenly believe public liability insurance covers every major business risk, everything from cyber incidents to employee injuries and product defects. That mistake leads to denied claims and unexpected gaps. Standard public liability policies exclude critical exposures, leaving sellers exposed if you don’t address them early.

Myth 1: Public Liability Covers Product-Related Claims

The assumption: public liability insurance protects you if a product you sell causes harm or property damage. Many sellers expect their policy to handle any lawsuit, no matter the source.

But public liability only covers injuries or property damage from your business operations, not from defective products you sell. If a kitchen gadget you sell causes a fire in a customer’s home, that’s a product liability claim, not public liability. Without specific product liability coverage, legal bills and settlements land on your desk. For more details, see these unique insurance risks for e-commerce sellers.

Myth 2: Public Liability Protects Against Cyberattacks and Data Breaches

Online business feels risky, hacks, ransomware, data leaks. One in three e-commerce businesses faces a cyber incident each year. Many assume their liability policy includes cyber coverage.

Standard public liability excludes cyber events. Only a separate cyber liability policy covers costs from breached customer data, regulatory penalties, or business interruption due to an attack. Relying on public liability for digital risks leads to large out-of-pocket losses and non-compliance with marketplace requirements. See ways to protect your business and lower liability costs for more.

Myth 3: Employee Injuries Are Covered by Public Liability

Sellers often believe workplace accidents, like warehouse injuries or repetitive strain, fall under public liability. This confusion increases in small teams where roles overlap.

Public liability only responds to claims from non-employees: the public, customers, or contractors. Employee injuries require workers’ compensation insurance, which most states mandate. Relying on public liability for workplace accidents means denied claims and potential legal penalties for non-compliance. Review your coverages for all business activities.

Myth 4: Public Liability Covers Your Own Stock and Property

Some sellers think public liability will pay if their inventory or equipment is damaged, by theft, fire, or water leaks. They assume “liability” stretches to anything that disrupts business.

Public liability never covers loss or damage to your own assets. It protects against claims brought by others only. To shield inventory, fixtures, or equipment, you need commercial property insurance. Missing this distinction leads to uninsured losses when disaster strikes your warehouse or office.

Key Takeaway: Know Your Policy, and Close the Gaps Before They Hurt You

Public liability insurance covers claims from third parties for injuries or property damage tied to your business operations. It protects you against lawsuits from visitors or customers. But it leaves out most risks that e-commerce sellers face. No coverage for product defects. No help if your customer data gets hacked. Losses to your own inventory or digital assets, also outside its scope.

Assuming public liability protects against everything puts your business at risk. Data breaches, faulty products, and warehouse losses each need their own coverage. If you know what your policy covers, and what it doesn't, you can manage risk, keep your marketplace accounts in good standing, and avoid costly disruptions. Skipping this gap analysis risks both your profit margin and your reputation.

Go line by line through your insurance. Match your risks and platform requirements to your actual coverage. Fill protection gaps before they cost you. Next, check the 6 policy add-ons most e-commerce sellers miss and see pricing benchmarks for typical coverage costs to make smarter, more cost-effective choices.

Frequently Asked Questions

Does public liability cover loss or damage to a customer's property while it's in my care, custody or control (for example, repairs, alterations, consignment or storage), or do I need a specific extension?

No, most public liability policies expressly exclude loss or damage to third‑party property while it is in your care, custody or control (the common "care, custody and control" exclusion). You will usually need a specific extension or separate cover such as "goods in custody and control"/"bailee's customer goods" or contract works/stock insurance depending on whether you repair, store or consign items. Check your policy wording and sums insured (public liability limits commonly run from £2m, £10m) and ask your insurer or broker to add the correct extension.

If I sell on marketplaces like Amazon, Etsy or Shopify, will a standard public liability policy meet their seller insurance requirements, or do I also need product liability or to be named on the marketplace's policy?

No, a standard public (general) liability policy alone often will not satisfy marketplace requirements: most marketplaces (Amazon in particular) commonly require products liability (products and completed operations) coverage and may require you to list the marketplace as an Additional Insured on your policy or provide a Certificate of Insurance. Requirements vary by platform and product risk, so confirm the exact insurer endorsement and limits the marketplace demands, verify your policy includes products/completed operations (or buy a standalone product liability and recall policy if needed), and get your broker to issue the Additional Insured/COI Amazon or other marketplaces require.

Are claims arising from work carried out by subcontractors or independent contractors working for my business covered under my public liability policy, or should I require proof of their own insurance?

Usually your commercial/public liability (CGL) will respond to third‑party claims arising from subcontractors’ work, but coverage depends on your policy wording and exclusions and it will not cover the subcontractor’s own injuries (those are covered by workers’ compensation/employers’ liability). Because many policies limit or exclude independent‑contractor risk and an uninsured subcontractor can exhaust your limits or raise premiums, you should require subcontractors to carry their own Commercial General Liability (and Workers’ Comp where applicable), provide a certificate of insurance (COI), and name you as an additional insured with primary/non‑contributory wording. Always review your policy and get written indemnity clauses in subcontracts, and confirm specifics with your insurer or broker.

Does public liability cover third‑party claims that arise after my products are shipped overseas, or do I need separate international or territory‑specific liability cover?

You will need separate international/territory‑specific product liability cover or an international extension, public liability generally covers injury or damage from your services/operations, not post‑sale product claims overseas. Products liability covers liability for manufactured, supplied or sold goods, and standard domestic products liability often excludes jurisdictions such as the EU, UK or Canada. Check your policy’s territorial limits and obtain a worldwide or specified‑territory products‑liability endorsement or standalone policy with appropriate limits.

Will public liability pay for the costs of a product recall, customer notification or disposal of unsafe goods, or do I need a dedicated product recall or crisis-costs policy?

No, public/general liability (and standard product-liability) policies do not pay recall, customer-notification, or disposal costs; those expenses are typically excluded and require a dedicated product-recall or crisis-costs policy. Standard CGL/product-liability forms contain a “withdrawal of products” (product‑recall) exclusion that covers third‑party injury/liability but not the costs to remove, notify about, or dispose of unsafe goods. Purchase a standalone product‑recall/product‑contamination or crisis-management endorsement to cover notification, logistics, disposal, PR, and often replacement and business‑interruption costs, and confirm limits and sublimits in the policy wording.

Do public liability policies cover legal defence costs if a claim is baseless or fraudulent, and how should I choose policy limits and excesses for a small e‑commerce business?

Yes, standard public/general liability (and product liability) policies typically pay legal defence costs to defend you even if a claim is baseless, though claims arising from your intentional or fraudulent acts are excluded and insurers can later deny coverage after investigation; verify whether defence costs erode the policy limit or are paid outside the limit. For a small e‑commerce business, base limits first on partner/marketplace/landlord requirements and product risk, with a common baseline of $1,000,000 per occurrence / $2,000,000 aggregate and consider $2M/$4M+ for higher‑risk products (children’s items, ingestibles, electronics) or larger sales volume. Choose an excess you can actually pay (typical small‑business deductibles $500, $5,000, higher excesses cut premiums but increase out‑of‑pocket legal exposure) and confirm exact defence-cost and deductible terms with a broker.

Can I add cover for cyber incidents, advertising/copyright infringement or other media liabilities as endorsements to a public liability policy, or are cyber/media liabilities typically provided as separate policies?

No, cyber incidents and most media/IP exposures are normally handled by separate policies; standard public/general liability (CGL) excludes cyber risk and only gives limited “advertising injury” protection. Advertising-injury is an insuring agreement in many CGL forms but carriers commonly exclude copyright/other IP infringement and online/chatroom activity, so it won’t cover many media claims. Some insurers offer narrow endorsements for media or cyber at extra premium, but full cyber and media/media‑E&O protection is typically bought as standalone cyber and media/tech liability policies.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to famous product liability cases.

Related: Bullock v Philip Morris.

Related: NBA Star Garcia vs Ledraplastic.