Commercial general liability (CGL) insurance protects ecommerce stores from third-party bodily injury, property damage, and advertising/copyright claims, paying medical bills, repairs, legal defense, and settlements. Major marketplaces (e.g., Amazon) commonly require at least $1M/$2M liability and most small ecommerce businesses pay about $24, $73/month, making CGL both effectively mandatory for platform compliance and a relatively low-cost way to avoid crippling claims.

- What Is Commercial General Liability Insurance? Why Every...

- How General Liability Insurance Works For Ecommerce Sellers:...

- Why General Liability Insurance Matters: Key Benefits And...

- Common Myths About General Liability Insurance, And The Facts...

- General Liability Insurance: Your Essential Shield Against Ecommerce...

What Is Commercial General Liability Insurance? Why Every Ecommerce Store Needs It, And What It Really Costs

Commercial general liability insurance (CGL) protects your business if you’re held responsible for third-party bodily injury, property damage, or legal claims like copyright infringement. This coverage pays for medical bills, repairs, legal defense, and settlements tied to your operations or products. For online sellers, CGL is the backbone of stress-free insurance, keeping your store compliant and reducing risk.

Every ecommerce store faces exposure. A single delivery driver injury or product-related claim can trigger thousands in bills. Lawsuits target sellers of all sizes. Digital platforms set strict requirements: Amazon, for example, requires merchants with over $10,000 in monthly sales to carry liability coverage with at least $1 million per claim and in total, or sellers risk losing their accounts and income. Most small ecommerce businesses pay between $24 and $73 per month, with many plans falling between $42 and $73.

CGL insurance covers exactly what online sellers need: bodily injury, property damage, copyright or advertising injury, and legal expenses. It’s not optional if you want to keep selling on major platforms or protect your business from costly claims. For details on pricing and how to reduce your costs, see typical coverage costs and ways to lower your premium. Need to check if you’re legally required to have it? Review the real-world insurance requirements for online sellers.

How General Liability Insurance Works For Ecommerce Sellers: Coverage, Eligibility, And Pricing Factors

General liability insurance for ecommerce adjusts to your sales volume, product mix, and risk profile. Unlike static, traditional policies, your premium updates with real business details, location, revenue, product category, and claims history. Higher-risk products or a track record of incidents push rates up. Clean records and lower-risk goods keep costs stable.

Key Coverage Areas: What’s Actually Protected

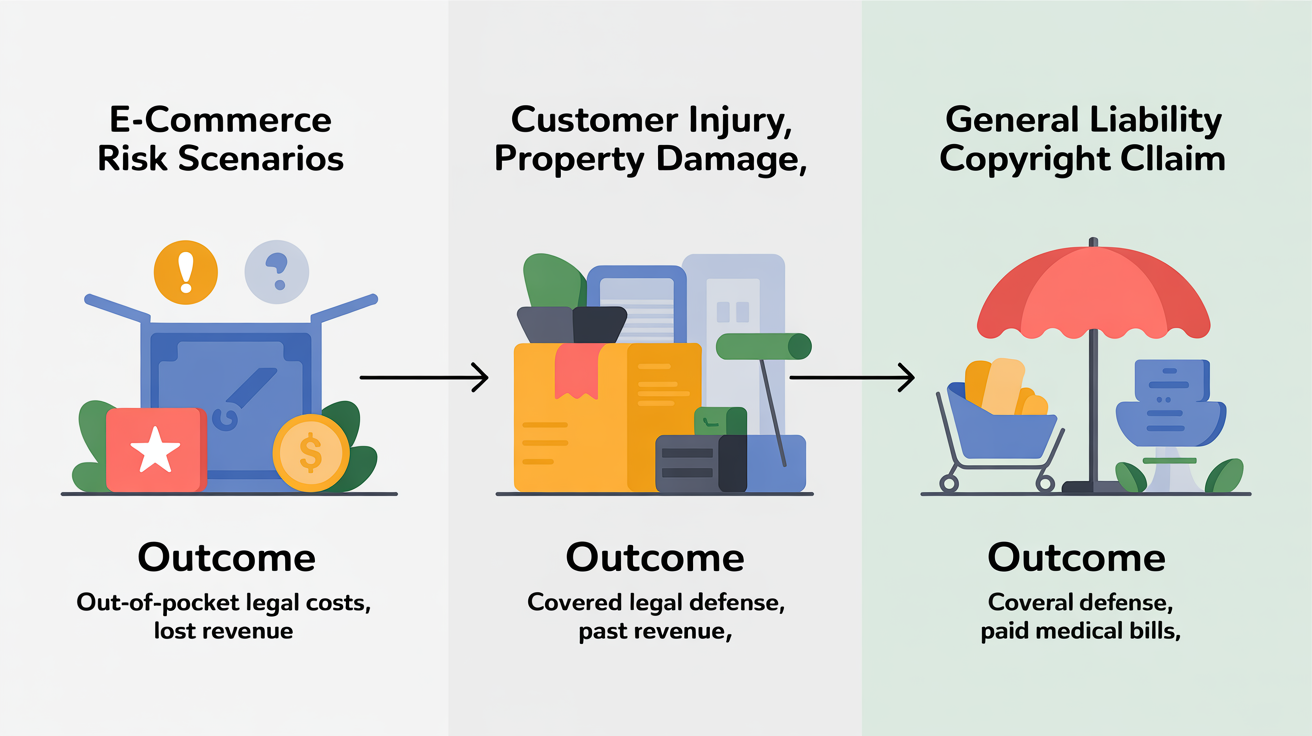

General liability insurance covers three main risk types: bodily injury, property damage, and advertising injury. If a product injures a customer, damages their property, or sparks a copyright or trademark dispute, your policy responds. Example: A customer slips on your packaging at a warehouse. Or a competitor claims your ad copied their trademark. For a breakdown of these scenarios, see what CGL insurance covers and why.

Most ecommerce policies start with a $1 million per occurrence limit and a $2 million aggregate, levels that meet Amazon and Shopify’s compliance standards.

Eligibility: Who Qualifies And What Disqualifies

Online sellers of physical products, solo operators and direct-to-consumer brands, generally qualify. Insurers require accurate details: sales, product types, fulfillment practices. Disqualifiers include prior liability claims, selling prohibited items (firearms, explosives), or incomplete application information.

- Businesses with large prior claims often see 25-100% higher premiums.

- Electronics, supplements, and children’s goods face higher risk classifications and costs.

- International sales or complex supply chains prompt extra review and can raise policy requirements.

Pricing Factors: How Your Premium Is Calculated

Premiums depend on these core factors:

- Location: California averages $82/month; Maine, $64. State regulations and litigation history affect rates.

- Revenue: More sales, more exposure, premiums scale as your store grows.

- Product Type: Apparel sits at the low end. Electronics, toys, and ingestibles trigger surcharges.

- Claims History: Past product injuries or copyright disputes sharply increase rates.

- Required Limits: Marketplace minimums cost less than enterprise-level requests for $5M coverage.

Most ecommerce sellers pay $42, $73 per month with no recent claims and low-risk products. Rapid growth or regulated industries can push costs above $100/month. For details, see how product and general liability affect your store’s bottom line.

Platform Differences: Amazon, Shopify, And Beyond

Insurance requirements vary by platform. Amazon requires $1M per claim and aggregate, plus naming them as an additional insured. Shopify’s terms are lighter for small stores, but bigger sellers must meet stricter benchmarks. Selling on multiple platforms increases exposure and can require broader or higher-limit coverage.

Marketplace compliance isn’t optional. Miss a certificate deadline or lack required coverage and you risk account suspension and lost sales. Confirm insurance needs before launching on any new channel to avoid costly interruptions.

Why General Liability Insurance Matters: Key Benefits And Real-World Scenarios For Online Stores

A single lawsuit can wipe out profits fast, even if you did nothing wrong. General liability insurance acts as a financial backstop, preventing one claim from derailing your business. Legal defense and settlements often top $10,000, draining cash and halting growth if you’re uninsured.

Lawsuit Protection: Medical Bills, Legal Fees, and Settlements

General liability insurance covers claims tied to customer injuries or property damage linked to your store. A customer has an allergic reaction to a cosmetic. A child swallows a toy part. Your policy pays for medical bills and legal defense in these scenarios.

Claims like these are common, and expensive. Over 11 million Americans visit emergency rooms each year because of product-related injuries. Lawsuits can target you even as a distributor or private labeler. Without insurance, you shoulder all legal bills and any settlement or damages awarded.

Advertising and Reputational Risks: Copyright, Slander, Libel

Online marketing brings exposure. Use a copyrighted photo by accident, or publish a product description that disparages a competitor, and insurance covers legal costs and settlements. Even a false advertising claim can cost thousands to defend.

One seller used a supplier’s product image without permission, $15,000 in legal bills and settlement followed. Another published a negative comparison, triggering a slander suit that cost over $20,000. Insurance covers both legitimate and nuisance claims. No marketing freeze. No lost revenue during disputes.

Platform and Partner Compliance: Maintaining Access and Sales

Insurance is now a standard requirement for selling on major marketplaces, using fulfillment centers, or maintaining payment processing. Platforms like Amazon demand $1 million in coverage and must be named as additional insured. Miss this, and your account risks suspension or frozen payouts.

- Amazon and Walmart require proof of coverage to keep your listings live

- Warehouses and third-party logistics providers reject inventory without compliant insurance certificates

- Payment processors may freeze funds or end accounts if coverage lapses

Proof of insurance is a routine checkpoint for every growing merchant. Lapses or expired documents can instantly halt sales. For examples of real insurance gaps and their consequences, see case studies from online stores.

Protecting Cash Flow and Enabling Growth

Every dollar spent on defense is lost capital. General liability insurance shields your operating funds and keeps your store running, even when claims arise. Actual ecommerce claims regularly reach $30,000 or more for legal defense, medical payments, and settlements.

With coverage, you can address both genuine errors and opportunistic lawsuits, without draining reserves or pausing campaigns. For a step-by-step view, see how the process works from instant quote to final purchase.

Common Myths About General Liability Insurance, And The Facts Online Sellers Need To Know

The most damaging misconception: if you only sell online, you don’t need general liability insurance. This is false. Online-only businesses face the same legal risks as physical stores. You’re still liable for injuries, property damage, or advertising mistakes connected to your business, no matter where you operate.

Myth: Homeowners or Renters Insurance Covers Your Ecommerce Business

Many first-time sellers assume their home insurance will protect business assets or claims from online sales. Inventory stored at home? They think any loss is just another household incident.

Home insurance policies almost always exclude business activities. If a customer sues over a defective product or someone is injured picking up an order from your home, your claim will likely be denied. Personal policies exclude injuries or property damage related to commercial ventures. Without a separate business policy, you risk out-of-pocket legal bills and product losses. For details, see what’s not covered by a commercial general liability policy.

Myth: General Liability Insurance Always Includes Product Liability

Many sellers believe every general liability policy automatically shields them from product-related lawsuits. They rarely check if injuries or damages from their products after a sale are actually covered.

Product liability is often included, but not guaranteed. Some general liability policies provide limited or no coverage for product claims unless you request a specific endorsement. If your policy only covers injuries during business operations, you could be denied coverage for defects or labeling issues that cause harm after purchase. Sellers often find too late that product injuries fall outside basic coverage. Always confirm your policy specifically includes product liability. Otherwise, a single lawsuit can bankrupt a business.

Myth: Only Large or Storefront Businesses Need Liability Insurance

Some online sellers think lawsuits only target big brands or traditional stores. Ecommerce can feel intangible, and platforms rarely highlight legal risks for small merchants.

Any seller, regardless of size or sales volume, can be sued if a product causes harm or if advertising content infringes on rights. Lawsuits over defects, improper warnings, or copyright disputes routinely target small shops. Platforms like Amazon now require $1 million in coverage because even micro-businesses face litigation risk. Operating uninsured isn’t just risky; in some states and marketplaces, it’s out of compliance or even illegal. See our compliance guide for more on legal and financial pitfalls.

Myth: Ecommerce Platforms or Suppliers Protect You from Lawsuits

Some sellers believe marketplaces, payment processors, or manufacturers will handle legal claims. The idea: being “just a reseller” means someone else is liable, or platforms offer automatic protection.

You’re responsible for every product you sell, no matter your role. Suppliers can be overseas or underinsured. Ecommerce platforms rarely intervene, most state in their terms that sellers alone are liable for claims. Without your own policy, you shoulder all defense costs and settlement risks. Proper insurance is the only reliable shield against unexpected lawsuits in ecommerce.

General Liability Insurance: Your Essential Shield Against Ecommerce Risks And Unexpected Costs

General liability insurance shields your ecommerce business against claims of bodily injury, property damage, and advertising errors linked to your operations. It pays legal fees, settlements, and medical costs if someone is hurt or property is damaged by your business or marketing. Bottom line: you need this coverage to stay compliant and avoid unexpected financial hits as an online seller.

The real risk isn’t missing out on a sale, it’s a lawsuit tied to a product you didn’t even make. Most online marketplaces mandate general liability, usually with a $1 million minimum limit. Monthly premiums typically fall between $24 and $85, shaped by your location, product types, and sales volume. Insurers weigh your risk profile, what you sell, where you sell, your claims history, when setting your rate. Higher-risk products or states push costs up; clean records and low-risk inventory keep premiums down.

Still deciding? Compare risk and budget using our ecommerce insurance cost guide. For details on structuring policies and choosing between business or personal coverage, see coverage decisions that matter.

Frequently Asked Questions

Does commercial general liability cover product recalls and the costs of removing or refunding affected items?

No, a commercial general liability (CGL) policy covers third‑party bodily injury and property damage caused by your products (the products‑completed operations hazard), but it does not pay for the costs to remove, recall, withdraw, replace or refund defective items. Those recall/withdrawal expenses require separate product‑recall or product‑withdrawal/contamination insurance (and CGL also excludes expected or intentional injuries).

Will CGL cover injuries to my employees or independent contractors, or do I need workers' compensation and/or employer liability coverage?

No, Commercial General Liability (CGL) does not cover injuries to your employees; you need workers’ compensation (and the Employers’ Liability coverage that accompanies it) to cover employee workplace injuries and related suits. For independent contractors it depends: if they’re properly classified and carry their own workers’ comp you’re generally not required to cover them, but many states treat certain subcontractors as employees or require you to provide coverage, so check state law and contract/policy language.

Is product liability insurance different from general liability, and when should an ecommerce seller buy a separate product liability policy?

Yes, product liability specifically covers bodily injury or property damage caused by a product (manufacturing/design defects, failure to warn), while general liability covers premises/operations, advertising injury, and other third‑party claims. Many general liability policies include “products and completed operations” coverage, but you must check limits and exclusions. Buy a separate product liability policy if you sell physical goods (including dropship or resale) and especially for higher‑risk categories (children’s products, consumables, electronics, medical/cosmetics), if you manufacture or private‑label items, if your GL has low limits or exclusions for products, or if marketplaces/partners (e.g., Amazon, Walmart) require it.

Does general liability insurance protect against cyber incidents like data breaches, hacked customer payment information, or ransomware?

No, general liability (GL) policies typically do not cover cyber incidents like data breaches, stolen payment data, or ransomware. GL is designed for third‑party bodily injury and property damage and usually excludes non‑physical/intangible cyber losses (coverage may only apply if a cyber event causes physical injury or property damage). You need a dedicated cyber liability/data‑breach policy or specific cyber endorsements (or E&O/professional liability for some data‑handling claims) to cover legal fees, notification and credit‑monitoring costs, PR, ransomware payments, and remediation.

If I sell internationally, will my CGL policy cover claims from customers or incidents that occur outside the United States?

No, standard CGL policies (the ISO CGL form) limit the “territory” to the United States (including its territories and possessions), Puerto Rico and Canada, so incidents that occur overseas are generally not covered. Some policies will still respond if a suit is brought in the U.S. for an overseas incident, and you can purchase endorsements (foreign/territory extension or worldwide liability) or a separate international liability/products policy to add coverage. Check your policy’s Territory clause and talk to your broker/insurer to obtain the specific endorsement or foreign liability product you need.

I run my store from home, does my homeowners insurance cover business-related claims, or do I need a separate CGL policy for a home-based ecommerce business?

No, standard homeowners policies generally exclude business-related claims and inventory, so they won’t cover liability or property losses from a home-based e‑commerce business. You need a commercial General Liability policy or a Business Owner’s Policy (BOP) that bundles GL and commercial property (many small-business BOPs run around $95/month) and you should also consider product-liability and cyber-liability coverages to protect inventory, customers, and online risks. For very occasional, low‑risk activity a limited home‑business endorsement might suffice, but regular sales, customer visits, or significant inventory require a separate business policy.

How do I prove I have the required coverage to marketplaces (e.g., obtaining a certificate of insurance), and can I add a marketplace like Amazon as an additional insured on my policy?

Get a Certificate of Insurance (COI) from your insurer showing Commercial General Liability with Products Liability (preferably an Occurrence form) and upload that COI to the marketplace (Seller Central); insurers familiar with Amazon can typically issue a COI in 24-72 hours after application, quote acceptance and first payment. Yes, marketplaces commonly require you to name the platform as an additional insured (for Amazon, name “Amazon.com Services LLC” and its affiliates/assignees); for Amazon Pro sellers the minimum is typically $1M per-occurrence/$1M aggregate with a deductible under $10,000 and an insurer rated A- or better, while Vendor Central/enterprise agreements often require much higher limits (e.g., $10M) and contain extensive indemnification obligations. Make sure your company name and address on the policy exactly match your Seller/Vendor account before uploading the COI.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to eCommerce business insurance.

Related: What Is Not Covered By The Commercial General Liability (CGL).

Related: What Does Commercial General Liability (CGL) Insurance Cover? A Cost.