About 82% of small-business general liability policies include some product liability, but exclusions and marketplace rules leave about 19% needing endorsements or separate coverage, and product-related lawsuits commonly cost $35,000, $54,000 in legal defense. The key takeaway: don’t assume "general liability" covers your products, review policy language, add endorsements or standalone product liability as required, or use pay-as-you-sell options (e.g., Assureful) to avoid coverage gaps that can force your eCommerce business to pause or shut down.

- 82% of General Liability Policies Include Product Liability:...

- Breaking Down the Data: How Often Product Liability...

- What the Numbers show: Risk Exposure and Where...

- Emerging Trends: Growth in Standalone Product Liability and...

- Key Takeaway: Product Liability Isn’t Always Included, Review Your...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn More82% of General Liability Policies Include Product Liability: Why This Stat Changes How You Buy

82% of small business general liability policies come with some level of product liability coverage. Still, nearly 1 in 3 sellers assume they're always protected, leaving themselves exposed to claims that average $54,000 just in legal defense. One missed detail and your eCommerce business could face a bill that forces you to pause or shut down.

Policy language matters. Many sellers see "general liability" and think every product issue is covered. Not so, especially if you import, rebrand, or sell on multiple platforms. Exclusions and gaps are common. Missed coverage can drain your cash flow, and threaten your ability to operate.

This guide breaks down what general liability and product liability insurance actually cover, how policy fine print shapes your risk, and where most eCommerce sellers get caught off guard. You'll see how pay-as-you-sell options like Assureful eCommerce Insurance compare with traditional policies, so you avoid nasty surprises. For a full side-by-side, see our detailed comparison of product and general liability insurance and our complete buyer’s guide to eCommerce liability insurance.

Breaking Down the Data: How Often Product Liability is Bundled With General Liability, and What It Actually Covers

Most eCommerce general liability policies include product liability, but 19% of sellers still need endorsements or separate coverage to meet marketplace requirements. That gap often surfaces only after a claim. Product-related lawsuits average $35,000, $54,000 per incident, enough to drain small business reserves. If you rely on bundled coverage, a single policy exclusion can determine whether your business survives a major claim.

Rates of Inclusion: How Often is Product Liability Bundled?

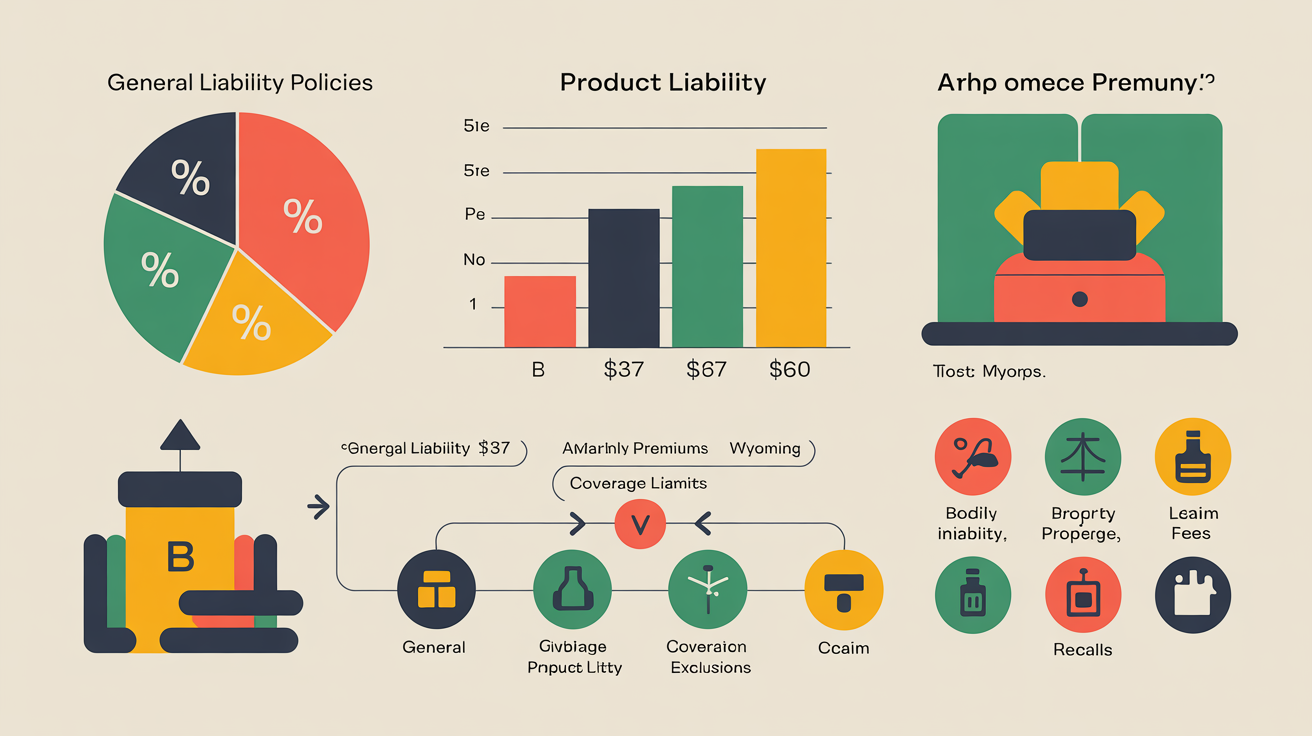

About 82% of small business general liability policies in the U.S. include some form of product liability coverage. The other 18% of sellers either lack any product liability protection or must add endorsements to meet marketplace rules, especially on platforms like Amazon and Shopify. Insureon data confirms that 19% of sellers needed endorsements specifically for marketplace compliance. Multi-channel sellers face even greater risk of gaps, particularly if importing or rebranding products. For a closer look at the differences, see our comparison of product and general liability insurance.

Premium Costs and State-by-State Differences

The median monthly premium for general liability with product liability is $45, based on Insureon data. Costs shift by risk level, sales volume, and state. In Oregon, eCommerce sellers pay as little as $37 per month. Wyoming averages approach $60, a 62% swing driven by claims history and legal climate. Standalone product liability policies typically start higher, especially for high-risk goods. Assureful eCommerce Insurance offers pay-as-you-sell billing starting at $26 per month, often reducing premiums by 42% compared to traditional A-rated insurers.

Coverage Limits: What Do Typical Policies Provide?

Policies for small eCommerce sellers usually start at $1 million per occurrence and $2 million aggregate, matching Amazon’s minimum for sellers above $10,000 in monthly sales. These limits aren’t fixed. Larger sellers or those with higher-risk goods may need $5 million or more in total coverage, especially if manufacturing or importing. Endorsements and policy upgrades become necessary as you branch out or handle complex inventory. See our comprehensive eCommerce liability insurance guide for aligning coverage with your risk.

Common Claim Types and Financial Impact

- $35,000, $54,000 per claim, Average product liability lawsuit cost, including legal fees and settlements (Insureon, industry claims data). This amount can cripple retailers without enough coverage.

- 11.1 million ER visits annually, Consumer product injuries drive millions of emergency room visits in the U.S., showing how frequently sellers get pulled into product claims.

- Most claims name every party in the chain, You’re exposed to lawsuits for defects even if you only imported or distributed the product. Liability doesn’t stop at the manufacturer.

- High-risk categories, Children’s products, ingestibles, electronics, and imports top the list for large claims due to safety, labeling, or design problems.

Policy Exclusions and the Consequences for Sellers

Bundled policies rarely cover every product-related risk. Exclusions often target imported goods, private label or rebranded inventory, and sales outside the U.S. One in four sellers who assumed “general liability” meant full coverage learned of gaps after a marketplace request or claim denial. Review your policy language carefully and check requirements in our guide to identifying CGL policy gaps. Pay-as-you-sell options like Assureful address many exclusions, but always confirm with your provider before changing your product line.

What the Numbers show: Risk Exposure and Where Most Sellers Fall Short

Nearly 20% of eCommerce sellers need extra endorsements just to hit basic product liability standards. Most assume their general liability policy covers every claim, but the data says otherwise. High average claim costs and premium spikes for higher-risk sellers leave many exposed, especially those importing or rebranding products. Too many underestimate their risk and find out too late.

Endorsement Gaps Expose Underlying Risk

One in five sellers needing additional endorsements signals a clear disconnect. “General liability” rarely means blanket protection. Marketplace demands and claim denials highlight real gaps. These gaps show up fast when Amazon or similar platforms ask for product-specific liability proof, forcing sellers into last-minute upgrades or out-of-pocket payouts. Bundled or basic CGL policies usually fall short for imported, private-label, or higher-risk goods.

Claims Involve the Entire Supply Chain

- Average product liability claims cost $35,000, $54,000, lawyers and settlements included.

- Every business in the supply chain gets named: manufacturers, importers, distributors.

- High-risk categories, children’s items, ingestibles, electronics, bring larger claims, often due to safety and labeling failures.

- U.S. emergency rooms record 11.1 million product-related visits a year. Scale and frequency are high.

Even smaller sellers face major financial risk if their policy’s “products-completed operations” language is vague or narrow. Importers and distributors with complex supply chains are especially at risk. Check our guide to product vs. general liability to see where your true exposure sits, before claims arrive.

Premium Disparities Reflect Risk Management Practices

Prior legal claims or recalls drive premiums up, anywhere from 25% to double. Insurers price in documented risk management: traceability, formal safety testing, quality control. Sellers who can prove these controls see lower costs and avoid steep hikes after incidents. Sourcing or selling overseas, especially under private label, means higher scrutiny and costs unless controls are strong and documented.

Platform Requirements Are Driving Demand for Explicit Coverage

Amazon, Shopify, and others keep tightening product liability compliance. Their insurance demands often exceed what standard policies provide, especially for imports or relabeled goods. Ignoring these demands risks your storefront and can trigger expensive policy upgrades after a claim or audit. Review your policy details before expanding product lines or moving inventory internationally. For aligning limits and endorsements, see our liability insurance buyer’s guide.

Assureful: Pay-as-You-Sell Is Not for Everyone

Assureful’s pay-as-you-sell model delivers predictable monthly costs and skips annual sales forecasting. Instant quotes, cancel anytime with 30 days' notice. Great for scaling online sellers or those with variable sales. But for highly seasonal sellers or those in high-claim categories, monthly costs might swing more than with flat-rate policies. Coverage is fully compliant, backed by A‑rated underwriters, and built for Amazon and Shopify sellers who need explicit product protection. See our policy gap analysis guide for a full breakdown.

Emerging Trends: Growth in Standalone Product Liability and Marketplace Enforcement

Marketplace enforcement is surging. Amazon, Walmart, and similar platforms triggered a 31% year-over-year jump in seller certificate of insurance requests. This pressure drives a sharp rise in standalone product liability: 27% of new policies in 2026 were standalone, up from 16% three years ago. The fastest adoption comes from sellers importing goods or handling higher-risk categories.

Platform Enforcement and Certificate Audits: A Strong Trend

Marketplace insurance requirements are now standard. Amazon and Walmart demand proof of compliant product liability coverage once sellers hit specific revenue levels. Certificate requests climbed 31% compared to last year, and platforms issue more non-compliance warnings and account holds. Sellers lacking pre-existing, fully compliant coverage experience sudden business interruptions and higher premiums when forced to buy insurance quickly. Policy details need regular review. Audits can arrive without notice. This trend is sustained and accelerating.

Standalone Product Liability Policies Gaining Share

Standalone product liability now outpaces bundled options. in 2026, these policies made up 27% of new product liability insurance, a 69% relative increase from 16% three years before. This shift reflects tougher underwriting and clear demand for coverage focused on product risks, especially for imported or private label items. Before peak selling periods, compare standalone and bundled options. Standalone often delivers more targeted protection as you move into new markets or categories.

Rising Import Volumes and Changing Risk Profiles

Imports and cross-border sales keep climbing. Insurance standards follow. High-risk categories, children’s products, supplements, electronics, face higher minimum limits and tighter policy terms. Insurers adjust rates and coverage by shipment origin and compliance records. Sellers using overseas suppliers or adding untested SKUs pay higher premiums and face more frequent policy reviews. For detailed cost impact, see our pricing benchmarks and ways to lower your coverage costs.

Emerging Signal: Stricter Contract Language and Dynamic Risk Pricing

Contract terms are tightening. Underwriters add exclusions, sublimits, and ongoing documentation requirements. Early indicators point to even more dynamic pricing, adjusting monthly by sales mix and geography. Pay-as-you-sell models like Assureful match this environment, offering stress-free insurance with no annual forecasts and predictable monthly billing. Sellers in volatile or high-claim segments may see wide swings in monthly costs, budget predictability can suffer. For a policy model comparison, see how to compare online insurance options.

Expect continued tightening as litigation rates climb and platforms enforce compliance at a granular level. Reviewing product vs. general liability exposure and the latest buyer’s guide is now essential for growing brands.

Key Takeaway: Product Liability Isn’t Always Included, Review Your Policy Before Relying On It

82% of general liability policies include some product liability coverage. But that coverage is rarely complete. Limits, exclusions, and gaps are common, assuming you're fully protected can mean serious out-of-pocket costs if a claim lands.

Online platforms are tightening insurance rules. Relying on generic liability coverage now puts established sellers at risk. More sellers need endorsements or standalone product liability insurance to satisfy platform requirements or higher-risk product categories. Annual reviews won’t keep up with changing sales channels or product mixes. Compliance checks are stricter. Pricing is more dynamic. Litigation and cross-border imports only push risks higher.

Review your current policy in detail, don’t stop at the declarations page. Compare product liability versus general liability directly and use the latest buyer's guide before your next renewal. If your products or business model have shifted, reassess your limits and exclusions to avoid expensive coverage gaps.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

How can I check if my current general liability policy covers product liability?

Check your policy declarations and the coverage pages for a line called “Products and Completed Operations” (sometimes labeled “Products hazard” or “product liability”) and confirm a limits amount; you can also check the certificate of liability form’s “Products” section. If that wording or limits/exclusions aren’t present or aren’t adequate, ask your broker/insurer for written confirmation or an endorsement, or buy a standalone product-liability (or product-recall) policy.

Will my policy cover product recalls?

No, product liability (or standard general liability) policies generally exclude product recall costs. You must buy a separate product recall policy or endorsement to cover recall-related expenses, so consult an independent insurance agent to add appropriate recall coverage and limits.

How much does it typically cost to add a product liability endorsement to an existing general liability policy for a small eCommerce business?

Typically about $300, $2,000 per year, with many small e‑commerce sellers paying roughly $500, $1,000 annually for a basic product‑liability endorsement onto an existing GL policy. Price depends heavily on product risk, sales volume and limits, low‑risk $1M, $2M limits sit at the low end, while large limits or international extensions (e.g., $25M with EU/UK/Canada/Australia) can raise premiums into the tens or hundreds of thousands.

If I dropship products from a third‑party supplier, will my general liability policy cover defects or do I need the supplier’s insurance and/or a separate product liability policy?

Not reliably, many commercial general liability (CGL) policies include limited "products‑completed operations" coverage, but that coverage can exclude manufacturing/design defects, have low limits, or otherwise leave a dropshipper exposed, and you can be sued even if you never handled the product. Require the supplier’s certificate of insurance and a written indemnity or to be added as an additional insured, and carry your own product liability policy with limits acceptable to your marketplaces/retailers (Amazon/Walmart frequently require this). Check your CGL policy wording and limits with your agent to confirm gaps.

How long after a sale will product liability coverage respond to claims for injuries from latent defects (e.g., years after purchase)?

It depends: occurrence policies respond to bodily injury that happens during the policy period even if the claim is made years later, whereas claims‑made policies only respond to claims first reported during the policy period (or during an extended reporting/tail period or if the claim fits the policy’s retroactive date). State law also limits recovery, statutes of limitations for personal injury commonly run 2-6 years and many states impose statutes of repose often around 10 years (varies widely), which can bar latent‑defect claims regardless of insurance. Coverage also won’t respond if you let the policy lapse and didn’t buy tail/prior‑acts coverage.

Are contaminated or spoiled products (food, cosmetics) covered under standard product liability, or do I need a specific contamination/pollution endorsement?

Standard product liability policies typically cover bodily injury or property damage caused by defective, contaminated or spoiled products (many insurers specifically list food contamination and strict liability as covered per policy wording). However, insurers commonly treat food, cosmetics and products with health claims as higher‑risk and will often require a contamination/pollution or product‑recall endorsement, specialized food‑service/product‑contamination cover, or enhanced underwriting and limits, so check your specific policy wording and insurer requirements.

What proof of insurance and minimum liability limits do major marketplaces (Amazon, Etsy, eBay) typically require for sellers to meet product liability rules?

Amazon: sellers with >$10,000/month must upload a Certificate of Insurance (COI) showing Commercial General Liability including product liability (commonly $1,000,000 per occurrence, $1,000,000 aggregate in Amazon guidance), list “Amazon.com Services LLC” as additional insured, and keep policy deductibles under $10,000. Vendor/enterprise agreements (Vendor Central, large retail marketplaces) often demand far higher limits (commonly $10,000,000) and strict additional‑insured/indemnity wording. Etsy and eBay generally do not impose blanket seller product‑liability minimums for ordinary marketplace sellers, though specific programs, high‑volume or business accounts and some categories may require a COI or higher limits; industry practice is to carry $1M, $2M per occurrence.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to eCommerce business insurance.

Related: What Is Not Covered By The Commercial General Liability (CGL).

Related: How Much Is Commercial General Liability Insurance? What It Covers.

Sources

- hotalinginsurance.com

- nextinsurance.com

- mailchimp.com

- vouch.us

- seo-pages-web.vercel.nerdwallet.com

- nerdwallet.com

- landesblosch.com

- jmg.com

- shopify.com

- progressivecommercial.com

- flashpricer.com

- forbes.com

- fitsmallbusiness.com

- moneygeek.com

- assureful.com

- pixelunion.net

- 1800insurance.com

- moneygeek.com

- techinsurance.com

- insurancecanopy.com

- insureon.com

- thehartford.com

- bankrate.com

- blog.hubspot.com

- uschamber.com

- allstate.com

- dealhub.io

- finance.yahoo.com

- insure.com

- anthem.com

- progressive.com

- insureon.com

- piainsagency.com

- esportsinsurance.com

- moneygeek.com

- aflac.com

- checklistguro.com

- vpm-legal.com

- guardianlife.com

- pattersonlawfirm.com

- wsj.com

- wsj.com