Hired and non-owned auto (HNOA) insurance fills a critical gap because personal auto and standard general liability policies usually exclude accidents when owners or employees use rented or personal vehicles for business, and a single claim can exceed $45,000. Small eCommerce sellers should identify activities that trigger exclusions, purchase HNOA limits aligned with sales volume (including pay‑as‑you‑sell options), and keep proof of compliant coverage to avoid denied claims or marketplace/lender penalties.

- Why Hired and Non-Owned Auto Coverage Matters: Costly...

- Understanding Hired and Non-Owned Auto Insurance: Definitions and...

- Securing Hired and Non-Owned Auto Insurance: A Practical,...

- Costly Mistakes When Insuring Hired and Non-Owned Vehicles, And...

- Tools and Resources: Getting Compliant, Seller-Specific Coverage Fast

- Protect Your Store and Your Balance Sheet: A...

Why Hired and Non-Owned Auto Coverage Matters: Costly Gaps Even Small Sellers Miss

One business-related auto accident, just one, can leave you with uninsured losses topping $45,000. Even small eCommerce operations face this risk. Personal auto insurance and standard general liability almost never cover accidents if you or an employee use a personal or rented vehicle for business tasks. Many sellers find out too late: a single claim can erase profit from months or years.

Hired and non-owned auto (HNOA) is the gap. Delivering packages yourself? Sending staff for last-minute inventory? These common activities trigger exclusions in most personal and general business policies. Without HNOA, you're exposed. Worse, some platforms and states require proof of compliant coverage, miss it, and you risk denied claims or even marketplace suspension.

This guide shows you how to assess your exposure, spot the triggers for HNOA, and secure coverage that matches your actual business driving. You'll see real examples, get benchmarks for coverage levels, and compare how "pay-as-you-sell" insurance fits eCommerce workflows, no annual forecasts or upfront guesswork. For more on protecting business vehicles, see our vehicle protection overview. Need a full breakdown of commercial policy types for online sellers? Visit our complete eCommerce insurance buyer’s guide.

Understanding Hired and Non-Owned Auto Insurance: Definitions and Prerequisites for Sellers

Hired and non-owned auto insurance (HNOA) protects your business if you or your employees use personal, leased, or rented vehicles for business tasks. Most personal auto policies and standard business liability plans won't cover accidents that happen during work errands in a vehicle your company doesn’t own. One trip for a delivery or inventory pickup in a non-business vehicle can leave you responsible for legal and repair costs if you don’t have HNOA.

Personal car insurance usually stops at business use, even for a single package drop-off. General liability insurance also leaves out accidents involving non-owned vehicles. HNOA picks up where those policies leave off. It applies when you lease or rent a vehicle for business ("hired auto") or when employees or owners use their personal vehicles for company tasks ("non-owned auto"). If an accident happens, HNOA can cover legal defense, injury costs, and damage to others’ property. Losses after a crash can reach tens of thousands of dollars.

Know these terms before you get started:

- Hired auto: Any vehicle you lease, rent, or borrow for business, except those borrowed from employees or their households.

- Non-owned auto: Employee-owned or owner-owned vehicles used for business errands or deliveries.

- Aggregate limit: The highest amount your policy will pay for all claims within the policy period. Choose limits that fit your sales volume and risk.

- A‑rated underwriters: Insurers with top financial strength and claims reliability. Marketplaces and lenders usually require coverage from these providers.

Check if your business uses personal or rented vehicles for deliveries, inventory runs, or employee errands. Many eCommerce sellers miss these triggers until a claim shows the gap. Review your workflow and sales platforms for any business driving, even if it’s rare. For more on how HNOA fits with other business insurance, see how general liability affects online stores.

Want to compare HNOA with other commercial auto options? See our vehicle protection overview and complete eCommerce insurance buyer’s guide. Need sample premium ranges or deductible tips? Check pricing benchmarks and ways to lower your coverage costs.

Securing Hired and Non-Owned Auto Insurance: A Practical, Seller-First Approach

Skipping hired and non-owned auto insurance leaves your store open to large claims if anyone drives a non-company vehicle for business. The steps below show how to protect yourself, control costs, and stay compliant, even if business driving happens rarely or isn’t scheduled. You’ll avoid overpaying and close coverage gaps that general liability and standard auto policies miss.

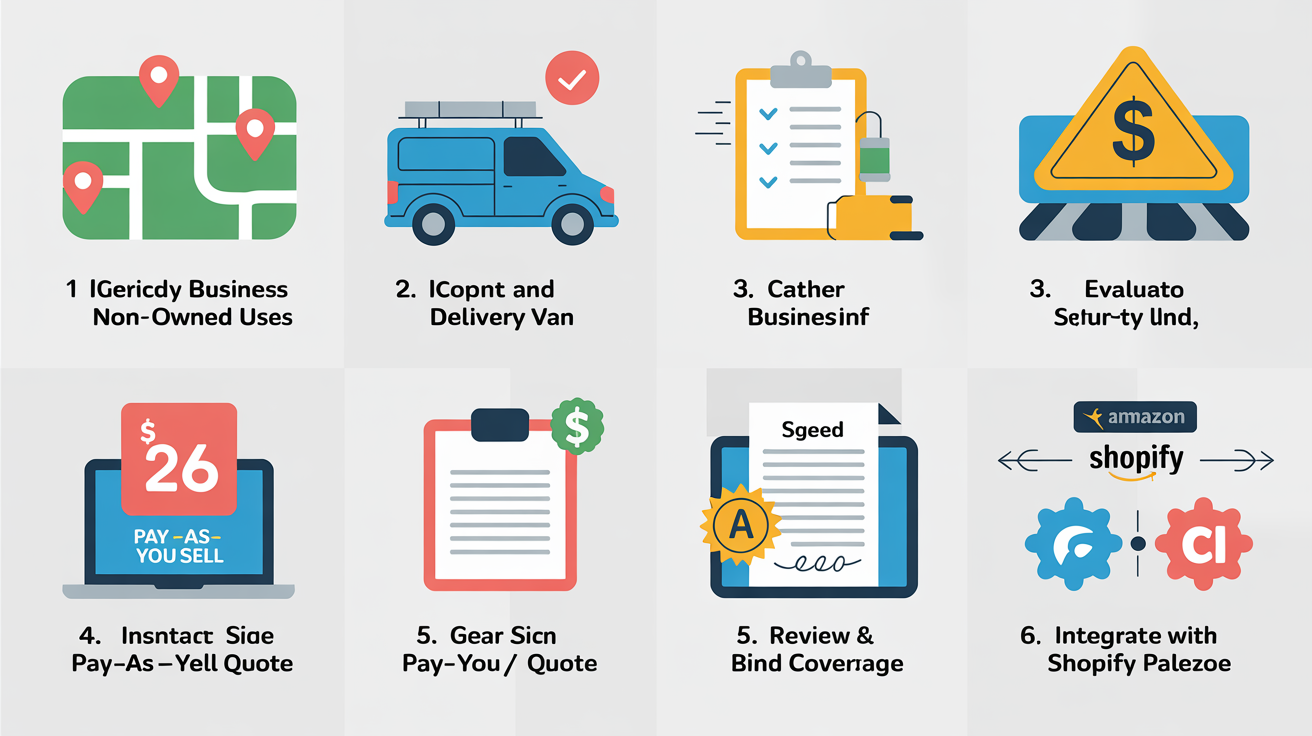

- Map Actual Business Driving. List every situation where you, employees, or contractors use personal, rental, or leased vehicles for business. That includes deliveries, picking up inventory, supplier meetings, or dropping packages at a carrier. If you only use company-owned vehicles, a standard commercial auto policy may be enough. Otherwise, HNOA is required.

- Gather Business Details. Collect your business entity type (LLC, S-corp, sole proprietor), employee count, five-year claims history, and a breakdown of business driving frequency. Record annual revenue and typical delivery value. Missing data leads to inaccurate quotes or denied claims.

- Assess Exposure and Key Choices. Estimate how often business driving occurs and who’s usually behind the wheel, owner, staff, or gig worker. Note the average and max value of goods per trip. If driving is rare but high value, HNOA becomes critical. When all deliveries use a third-party service with their own insurance, focus risk assessment elsewhere.

- Get an Instant Quote with Pay-As-You-Sell. Use a platform offering instant, usage-based quotes, no annual forecasts. Enter real business data to get a monthly premium based on last month’s sales. No large upfront deposits. This model fits seasonal or high-ticket sellers. For details on pricing and cost control, review these pricing benchmarks and ways to lower your coverage costs.

- Check Policy Features and Exclusions. Compare aggregate limits, exclusions for intentional acts, and backing by A‑rated underwriters. Confirm you can cancel with 30 days’ notice and that billing is monthly. Skipping this check can mean overpaying or missing compliance, especially if your business shifts fast. For comparison data, see our commercial auto insurance comparison stats.

- Bind Coverage and Integrate with Your Platform. Bind coverage as soon as you select a policy, don’t wait for the next delivery. Where possible, connect your insurance to your eCommerce platform to automate compliance tracking and reporting. Manual reporting increases the risk of accidental lapses as order volume grows. For workflow automation advice, see our vehicle protection overview.

- Reevaluate as Operations Change. Review your policy every six months or after major shifts, new products, changed shipping models, or sales spikes. HNOA needs can change fast as your store grows. For a full checklist of related coverage, see our complete eCommerce insurance buyer’s guide.

Follow these steps to avoid relying on outdated personal policies or guesswork. You’ll keep your store protected and costs aligned with real business, not inflated projections.

Costly Mistakes When Insuring Hired and Non-Owned Vehicles, And How to Fix Them

Many eCommerce sellers make one critical error: believing a personal auto policy will cover business use. That misconception leads to denied claims, out-of-pocket settlements, and sometimes, shutting down completely. Carrier filings show personal auto insurers almost always exclude commercial use. Each drive for business, by you or an employee, can leave your business exposed.

Assuming Personal Auto Covers Business Use

Plenty of sellers rely on personal auto insurance for order drop-offs or vendor meetings. That confidence often comes from not reading policy exclusions or following outdated advice. Most personal policies exclude claims tied to business activity. An accident during a delivery or while sourcing inventory? Usually not covered.

The fix: get a dedicated Hired and Non-Owned Auto (HNOA) policy for all business driving. Check that commercial use is clearly endorsed. Scrutinize exclusions for business-related claims. For structuring guidance, see this coverage structuring guide.

Overlooking Occasional or ‘Last-Mile’ Deliveries

Some think insurance risk only matters with frequent business driving. That’s not accurate. Even one-off use of a personal or rented vehicle, like dropping off a large order, creates HNOA exposure. Insurers and courts don’t care how often it happens.

If your business ever uses a vehicle it doesn’t own, get HNOA coverage. Each trip brings legal and financial risk. For a step-by-step breakdown, review our vehicle protection overview.

Choosing Fixed Annual Premiums with Fluctuating Sales

Fixed annual premiums based on estimated sales trap eCommerce sellers. During slow periods, you overpay. When sales spike, you risk underinsurance. Usage-based pay-as-you-sell models cut average premiums by 42% compared to annual forecasts, especially with seasonal or high-ticket inventory.

Switch to monthly billing tied to actual prior-month sales. Pay-as-you-sell aligns costs with real revenue and improves cash flow. No more overpayment. Here’s how:

- Pick insurance providers that integrate with your eCommerce platform for automated sales tracking.

- Opt for flexible cancellation, cancel with 30 days' notice.

- Review and adjust your policy as sales change to avoid gaps or excess costs.

For premium benchmarks, check these cost benchmarks and market comparison stats.

Ignoring State or Platform Compliance Requirements

Some sellers miss that certain states and sales platforms require active commercial auto or HNOA coverage before you can list or renew. Manual compliance tracking is risky. Miss one renewal or document update, risk delisting or fines, no warning given.

Avoid disruption by choosing insurance that offers automated compliance tools and direct platform integration. Coverage status updates in real time, reducing the chance of accidental lapses. For a full compliance checklist, see our complete insurance buyer’s guide.

Tools and Resources: Getting Compliant, Seller-Specific Coverage Fast

The best eCommerce insurance tools handle compliance, cut manual work, and keep your attention on selling. Choose solutions with fast, automated quotes, integration with your selling platforms, and real-time certificates, no hidden fees or slowdowns. Speed and accuracy matter when shipments or your store’s status hinge on proof of coverage.

Instant Quotes and Automated Policy Management

Manual quoting and sales projections drag out the process and often inflate your costs. Automated quote engines that connect directly to Amazon or Shopify use your store’s data to calculate risk and set tailored premiums instantly. No more annual forecasts. Adjust coverage as sales change. Enjoy stress-free insurance with clear, predictable monthly bills.

If your revenue fluctuates or you face seasonality, pay-as-you-sell billing keeps costs in line. Compliance becomes far simpler, no last-minute paperwork or guessing next year’s sales. See how to compare online insurance options for a deeper look at digital insurance shopping.

Compliance Tracking and Coverage Verification Tools

Platform rules and state laws shift. Automated compliance trackers flag renewal deadlines, monitor for required policy forms, and generate instant proof-of-insurance certificates. Upload these straight to Amazon, Shopify, or your state portal. This cuts the risk of delisting, fines, or shipment delays from expired or missing coverage.

Seek out tools that offer:

- Automated reminders for expiring policies and compliance documents

- Instant certificate generation and uploads for Amazon/Shopify settings

- Commercial auto and HNOA coverage checklists by state, updated as regulations change

- Dashboards showing coverage status across all business lines

If you manage vehicles, deliveries, or outside contractors, start with our vehicle protection overview to map out your insurance needs.

Comparison and Customization Resources

Choosing a policy isn’t just about price. Use comparison tools that highlight differences in exclusions, claims processes, and aggregate limits, not just the monthly cost. Sellers who import products or hold higher-risk inventory need to review details closely to avoid gaps that could void future claims.

Online calculators and comparison aids help you benchmark pricing, see how risk factors affect your premium, and spot gaps early. For specifics, check our cost benchmarks and tips to lower premiums and side-by-side commercial auto comparisons.

Best-in-Class Solution for eCommerce Sellers

For stress-free insurance built for eCommerce, including general and product liability, commercial auto, and HNOA, look for a provider with pay-as-you-sell billing, A‑rated underwriters, and instant compliance tools. Assureful delivers all of this: platform integration, immediate coverage, and cancellation with 30 days’ notice. You get fully compliant, customizable protection that adjusts as your store grows.

Need a step-by-step process and platform checklist? Use our insurance buyer’s guide for eCommerce sellers. It covers every step from instant quote to ongoing compliance, so you control your protection with less hassle.

Protect Your Store and Your Balance Sheet: A Smarter Approach to Hired and Non-Owned Auto Insurance

One delivery or pickup in a personal, employee, or rental vehicle can create major liability gaps for your store. Standard business insurance doesn’t cover accidents in vehicles the business doesn’t own. Hired and Non-Owned Auto (HNOA) coverage closes that gap, protecting your finances if there’s an accident on company business.

Map every way your business uses vehicles, supply runs, returns, even casual errands. Then match coverage to those exposures. Start with a step-by-step check using vehicle protection for ecommerce sellers. Price check with our cost benchmarks and premium reduction tips. Look for policies from A‑rated underwriters, monthly billing by usage, and tools that handle compliance, upload certificates, and send reminders. No fines. No lapsed coverage.

For online sellers, stress-free insurance means pay-as-you-sell coverage you can adjust or cancel with 30 days’ notice, managed in minutes. That’s what Assureful eCommerce Insurance was built for. See the full checklist and comparison process in our insurance buyer’s guide for eCommerce sellers. Protect your store and your balance sheet as you grow.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

How much does hired and non-owned auto insurance typically cost for eCommerce businesses?

About $171 per month (≈$2,050/year), Insureon reports a median commercial auto cost for eCommerce small businesses that includes hired/non‑owned exposures. Actual premiums vary by state, number of drivers and vehicles, limits and claims history and can be lower for occasional use or higher for heavier exposure.

Are there state or marketplace requirements for commercial auto insurance that affect eCommerce sellers?

Yes. State laws typically require commercial auto insurance for vehicles titled to or principally used by a business (including delivery of inventory), with minimum liability limits and registration/classification rules that vary by state. Marketplaces more commonly mandate general/product liability, but platforms that involve delivery or transport (or large sellers) can and do require commercial auto coverage or specific certificates/endorsements, check your state DMV and each marketplace’s insurance rules for exact limits and proof requirements.

Can I add hired and non-owned auto coverage as an endorsement to my existing business liability policy, or do I need a separate commercial auto policy?

Usually you can add hired and non‑owned auto (HNOA) as an endorsement to your commercial auto policy or your general liability policy, though some carriers offer HNOA as a standalone policy or will require a separate commercial auto policy if you own or regularly operate company vehicles. HNOA covers liability for rented, leased, or employee‑owned vehicles used for business (third‑party bodily injury and property damage) but typically does not pay for collision or physical damage to those vehicles. Check with your insurer and any contract/COI requirements because carrier rules and underwriting (frequency of use, number of vehicles, and vehicle value) determine whether endorsement or a full commercial auto policy is required.

Does hired and non-owned auto insurance cover physical damage to a rented or employee-owned vehicle, or only liability for third-party injuries and property damage?

Answer: Hired and non‑owned auto (HNOA) is liability coverage, it pays for third‑party bodily injury and property damage your employees cause while driving rented or employee‑owned vehicles, but it generally does NOT pay for physical damage to the rented or non‑owned vehicle itself. To insure the vehicle’s collision/comprehensive damage you must buy the rental company’s loss‑damage waiver/CDW or carry a commercial auto policy (or confirm the employee’s personal auto policy covers business use and physical damage).

When an employee is at fault in their personal car on a work errand, which insurance pays first, the employee’s personal policy or my business’s HNOA? How does that claims process work?

The employee’s personal auto policy is primary; your business’s HNOA (hired/non‑owned auto) is excess and only pays after the employee’s limits are exhausted or their carrier denies coverage. The usual process is the employee files the claim with their personal insurer first while you promptly notify your commercial/HNOA carrier; the HNOA insurer will investigate and step in to defend/pay amounts above the employee’s limits (or if the employee’s policy excludes business use). If the employee has no coverage or their policy expressly excludes business use, the HNOA can become primary; note HNOA typically covers liability only (not physical damage to the employee’s vehicle) unless you’ve purchased a specific physical‑damage endorsement.

Will HNOA protect my business when I use independent contractors or gig drivers (e.g., same-day couriers or app-based drivers), and what conditions or documentation do insurers require for contractor coverage?

Yes, Hired & Non‑Owned Auto (HNOA) can protect your business for liability when independent contractors or app/gig drivers use non‑owned vehicles on your behalf, typically kicking in after the driver’s own auto policy limits are exhausted to pay third‑party bodily injury or property‑damage claims. Carriers commonly require contractors to carry their own auto liability insurance and supply a Certificate of Insurance (often naming your company as certificate holder or additional insured), a written contractor agreement/independent‑contractor declaration (and sometimes MVR/background checks), and proof you maintain required general/commercial liability coverages; note HNOA usually won’t cover damage to the contractor’s vehicle, cargo, commuting incidents, or business‑owned vehicles.

What specific documents do insurers or marketplaces typically ask for to prove HNOA coverage or to support a claim (e.g., certificate of insurance, rental agreements, driver logs) and how quickly must I provide them?

Insurers/marketplaces typically ask for a certificate of insurance and the HNOA policy endorsement or declarations page; the rental/lease agreement and any loss‑damage‑waiver (LDW) receipts; the driver’s license and motor‑vehicle record; signed employee authorization/permission to drive and driver/mileage logs; the police/accident report, photos of damage, repair estimates, medical bills/witness statements, employer incident report, and invoices/payroll records for lost time or damages. Timing: carriers require prompt notice, commonly initial notification within 24-72 hours and immediate submission of critical docs (police report, rental agreement); full supporting documentation is generally expected within 7-30 days or “as soon as reasonably possible” per your policy. Marketplaces usually require a COI or proof of HNOA before listing or within a few days of onboarding and must be updated at renewal, so check the platform’s and policy’s specific deadlines.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

Related: What Is Not Covered By The Commercial General Liability (CGL).

Related: How Much Is Commercial General Liability Insurance? What It Covers.

Sources

- fitsmallbusiness.com

- policyape.com

- shopify.com

- 1800insurance.com

- thehartford.com

- moneygeek.com

- nerdwallet.com

- seo-pages-web.vercel.nerdwallet.com

- landesblosch.com

- insureon.com

- forbes.com

- constructioncoverage.com

- vouch.us

- hotalinginsurance.com

- travelers.com

- cyberpolicy.com

- norrisinsurance.com

- marketwatch.com

- totalcsr.com

- progressivecommercial.com

- progressivecommercial.com

- allstate.com

- nextinsurance.com

- moneygeek.com

- insurancebusinessmag.com

- quora.com

- thesmokedrop.com

- noblepagroup.com

- trackmage.com

- vargasinsurance.com

- regulaforensics.com

- thehartford.com

- biberk.com

- deloitte.com

- macombinjurylawyers.com

- thehartford.com

- thehartford.com

- progressivecommercial.com

- pgicentralflorida.com

- progressive.com

- thehartford.com

- geico.com

- berxi.com

- statefarm.com

- geico.com

- insuredbetter.com

- embroker.com

- nextinsurance.com