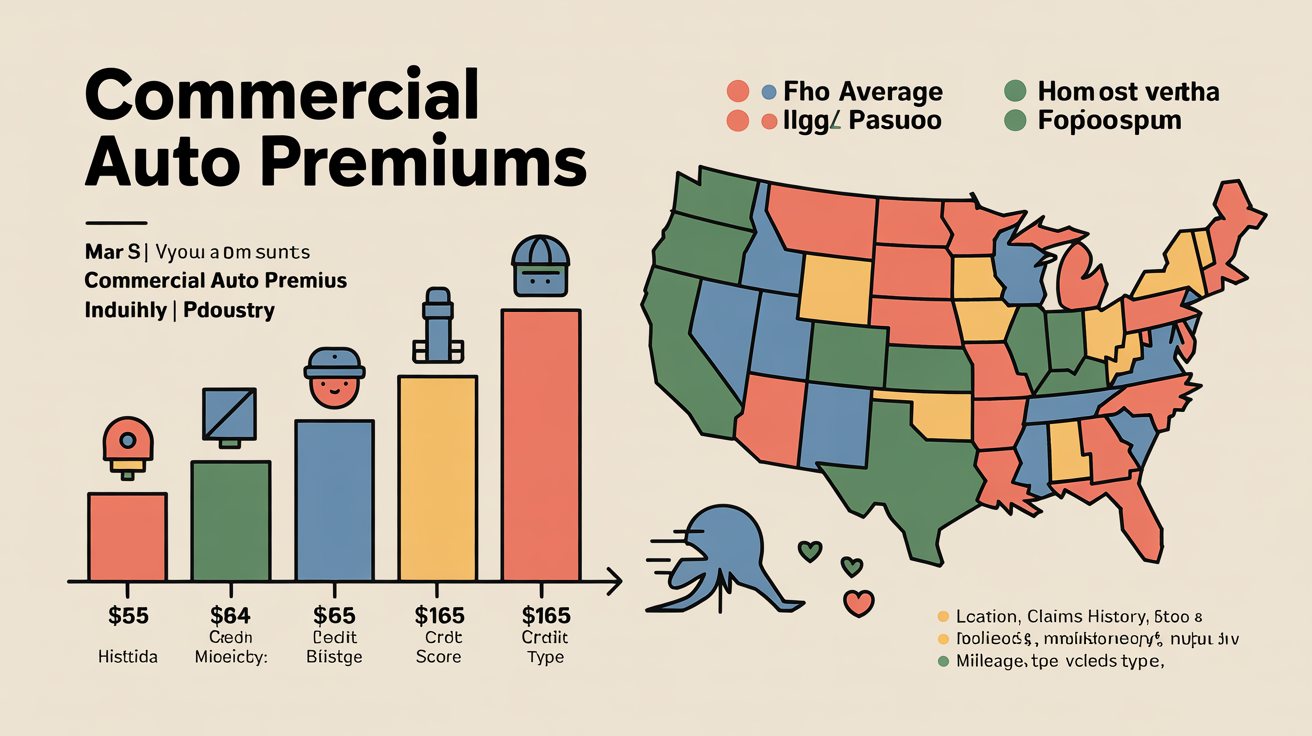

Commercial auto premiums vary dramatically by location and risk factors, Idaho businesses pay about $1,476 annually (up to 45% below the national average) while similar coverage in Florida or Louisiana can exceed $3,600 per year. The key takeaway: geography, driving records, vehicle details, fleet composition and coverage choices (including pay-as-you-sell options for eCommerce) drive these gaps, so small businesses must match policy type and limits to actual use to avoid overpaying or being underinsured.

- Why Commercial Auto Insurance Quotes Vary by as...

- Commercial Auto Insurance by the Numbers: Premiums, Key...

- Interpreting the Data: What Influences Commercial Auto Insurance...

- Emerging Trends in Commercial Auto Insurance Pricing: Inflation,...

- Key Takeaway: Premium Differences Are Wide, But Data Shows...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreWhy Commercial Auto Insurance Quotes Vary by as Much as 45%: The Data Revealed

Idaho business drivers pay up to 45% less for full coverage commercial auto insurance than the national average. In contrast, a business in Florida or Louisiana can see annual premiums soar past $3,600 for similar coverage. The difference is immediate, a delivery team in Miami could spend thousands more each year than a contractor in Boise for the same protection.

For small businesses, these pricing gaps hit hard. Overpaying drains profit. Underinsuring leaves you exposed. Location, driving records, vehicle details, and how you use those vehicles all shape your quote. Ignore these factors, and you risk higher costs or gaps in coverage when it matters most. With commercial auto rates trending upward across the country, picking the right policy isn’t optional, it’s essential.

This guide breaks down the main drivers of commercial auto insurance costs. State disparities, coverage choices, claims history, fleet makeup, and even your business sector all influence what you pay. We compare traditional annual policies to Assureful’s pay-as-you-sell insurance for eCommerce. For details on risk and savings, check our guide on protecting the vehicles that move your business, or benchmark your pricing with the complete buyer’s guide to commercial insurance.

Commercial Auto Insurance by the Numbers: Premiums, Key Factors, and Regional Gaps

Location drives real cost differences. In Florida, a business pays about $3,638 per year for commercial auto insurance, more than double the $1,476 average in Idaho. The Hartford pegs the national median premium at $55 per month, but actual rates swing sharply by region, type of business, and credit profile. Knowing these figures means you can budget with fewer surprises and avoid getting blindsided by unexpected costs.

Premium Ranges and National Averages

Monthly premiums for commercial auto insurance usually land between $55 and $165. The Hartford benchmarks small business liability coverage at $55 per month. That number matters for cash flow, especially since some states or industries push it much higher. Annual premiums stretch from $1,476 (Idaho) up to $3,638 (Florida), showing how geography and risk shape costs. For eCommerce sellers with unpredictable sales, Assureful’s pay-as-you-sell model matches insurance costs to actual revenue, critical if you run lean margins or see big swings.

State-by-State Premium Disparities

Your business address changes your rate more than almost anything else. Insuring a van in Idaho costs about $1,476 per year. In Louisiana or Florida, expect to pay over $3,600. Weather risks, traffic patterns, and local insurance fraud rates drive these gaps. For delivery fleets, that difference means thousands more in yearly overhead, affecting your pricing and ability to compete. Find more on how location shapes risk in our guide to protecting the vehicles that move your business.

Top Drivers of Quote Variability

- Location: Premiums can swing by as much as 45% between low- and high-cost states, the biggest factor in pricing.

- Business type: Delivery and rideshare operations pay more due to longer hours and riskier driving patterns.

- Number of vehicles: Fleets of five or more often get bulk discounts; solo vehicles pay more per car.

- Annual mileage: Putting 25,000+ miles on your vehicles each year can raise costs by 25-50% over low-mileage use.

- Vehicle age and value: Insuring a new vehicle (over $40,000) means higher comprehensive and collision premiums than covering older, cheaper cars.

- Driving and claims history: One at-fault accident can increase your premium by 20% or more, staying on your record for up to three years.

- Credit-based insurance scores: Poor credit? Some businesses pay up to 76% more than those with excellent credit, according to national insurer data.

Coverage Choices: Liability-Only vs. Full Coverage

Liability-only policies keep monthly costs close to the $55 median. Add collision and comprehensive, and you’ll likely pay $100 to $165 per month, depending on vehicle value and deductible. Full coverage protects against theft, vandalism, and single-vehicle accidents, but costs more upfront. Older vehicles or limited cash flow? Liability-only may make sense, though it doesn’t cover damage to your own vehicle in an at-fault crash. For more on choosing policy structures, see our complete buyer’s guide to commercial insurance.

How Your Business Profile Alters Pricing

Industry, revenue, and company structure all affect your quote. High-casualty sectors, delivery, rideshare, construction, face steeper rates, especially in cities. A clean claims record earns discounts; safety training can drop your premium even further. Deciding whether to insure under your business or personally? Our guide on structure, licenses, and coverage decisions that matter explains how these choices shape compliance and pricing.

Interpreting the Data: What Influences Commercial Auto Insurance Quotes Most?

Your quote reflects your actual risk. The data shows: businesses with clean records and stable operations pay far less than those with recent claims, new drivers, or added vehicles. Location and insurer-specific methods create big swings, two similar companies can see quotes differ by hundreds each month.

Location Drives Baseline Costs

Where your vehicles operate shapes your premium. Urban companies in high-traffic zones pay more, thanks to higher accident rates, dense populations, and stricter state rules. Insurers also weigh local litigation and weather risks, example: a bakery in Maine often pays less than a Miami courier, due to lower crash and crime rates. Move your business across state lines and rates can jump 30% or more, even with no change in your operations.

Coverage Structure and Policy Choices

Coverage selection matters. Liability-only keeps premiums near the $55 per month median. Add comprehensive and collision, and that jumps to $100, $165. Raising limits or lowering deductibles also increases costs, but not always by a fixed ratio, a $2 million limit can cost 25-40% more than $1 million. Balancing limits and deductibles keeps you compliant without draining cash flow. For details on structuring policies, see our guide to commercial auto coverage.

Individual Risk Factors: The Hidden Multipliers

- Claims history: One at-fault claim can raise your premium by 20% or more, impact lingers up to three years.

- Credit score: Low credit? Expect costs up to 76% higher than top-rated profiles.

- Fleet size and annual mileage: Adding vehicles or driving over 25,000 miles a year typically pushes premiums up 25-50% per car.

- Industry risk: Delivery, construction, and passenger transport see surcharges, even with clean records and stable locations.

Accurate, complete underwriting info keeps your rates down. Missing or vague details? Insurers default to higher risk ratings.

Why Quotes Vary So Widely Between Insurers

Even with identical business details and coverage, quotes often differ by hundreds per year. Each insurer uses its own system, weighting credit, claim types, local loss data, and details like company structure or past payouts. Some focus on specific industries or vehicle types, causing unexpected outliers. Always compare multiple providers on identical terms. Never take the first offer as the market price.

eCommerce sellers can benefit from Assureful’s pay-as-you-sell model, where premiums track actual sales, no annual forecasts. This approach can lower costs, but monthly changes require careful cash flow tracking. For more on how product and general liability interact, see how liability insurance affects your bottom line.

See how vehicle choice, driver records, and business structure affect your premium in our commercial auto insurance resource hub.

Emerging Trends in Commercial Auto Insurance Pricing: Inflation, Technology, and Risk Shifts

Commercial auto insurance premiums have climbed over 10% each year since 2022. The driver: claim severity, not frequency. Average vehicle insurance settlements increased nearly 5% in 2025, with repair costs up 5.1%. Accident counts have stabilized, but higher vehicle values and rising medical bills keep pushing rates up.

Inflation Drives Persistent Rate Increases

Repair and replacement costs have outpaced general inflation for three years. The Consumer Price Index for motor vehicle insurance rose 4.7% from mid-2024 to mid-2025. Used vehicle prices ticked up 1.8% in the same window, while labor and parts shortages sent repair bills higher. These higher insurer payouts flow directly into premium hikes for small businesses. Even as accident rates flatten, average payout severity keeps premiums climbing. For a breakdown of cost factors, see our coverage structuring resource.

Theft and Loss Trends: A Bright Spot for 2026

Vehicle theft dropped 17% in 2026, the sharpest decline in forty years. This early signal has started to ease comprehensive premium pressure, especially in cities. Fewer theft claims do help, but higher parts and replacement costs still outweigh the relief. Insurers are cautious, waiting to see if lower theft rates hold before moving rates down further.

Regulatory and Scoring Shifts: Credit-Based Pricing Under Scrutiny

Several states now restrict or ban credit-based insurance scoring for commercial auto. This removes both discounts and surcharges tied to credit, making premiums hinge more on claims and driving history. In some places, there's a 76% swing in premiums between top and low credit scores. These regulatory moves signal a real shift. Expect wider quote differences as insurers adjust risk models.

Mileage-Based and Telematics Pricing: Early Adoption, Rapid Expansion

Telematics and pay-per-mile pricing are gaining traction, especially for fleets. Programs like GEICO’s DriveEasy Pro offer discounts for safe driving and verified mileage. Adoption sits below 25% of commercial policies, but demand for usage-based billing keeps rising as businesses seek cost control. This is an early signal. Competitive pressure will likely speed up adoption over the next two years.

For eCommerce sellers, flexible models like Assureful’s pay-as-you-sell coverage deliver predictable monthly bills with no annual forecasts. This matches the industry’s shift toward data-driven, usage-based insurance. Downsides: cash flow varies month to month. Sellers value the transparency and full compliance. For more on vehicle choice and risk, visit our commercial auto insurance resource hub.

Key Takeaway: Premium Differences Are Wide, But Data Shows Where You Can Save

Commercial auto insurance premiums vary by more than 40% based on state, risk factors, and policy structure. That’s a significant swing. If you know where you land in this range, you can avoid overpaying and compare your renewal or new policy against national averages.

Premium calculations are getting more complex. Regional price gaps are growing. Claims history, credit, and inflation carry more weight. Insurers now favor data-driven, usage-based pricing over annual forecasts, especially for businesses with multiple vehicles. Expect more questions about your operations, driver records, and miles driven each month, quotes will likely differ more than before.

Review all the coverage structuring factors before committing. Benchmark your quote against other carriers. For ways to save through vehicle choices, clean driver records, or usage-based policies, visit our commercial auto insurance resource hub. Comparing options and understanding these shifts is essential to managing insurance costs in 2026.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

Is it cheaper to pay commercial auto insurance premiums annually or monthly?

Paying commercial auto insurance annually is usually cheaper because insurers often add installment fees or finance charges to monthly plans and sometimes give a small prepayment discount. Exact savings vary by carrier and state, typically a few percent or a flat monthly fee, so compare the insurer’s annual premium to the sum of monthly payments before deciding.

Does commercial auto insurance cover contents inside the vehicle?

No, standard commercial auto policies typically exclude coverage for business contents inside the vehicle. To insure tools, equipment, inventory or personal property carried in a vehicle you must add an endorsement or separate policy (for example a tools-and-equipment endorsement, business personal property/inland marine (floater) coverage, or other contents extension); check limits and deductibles with your agent.

What coverage limits should small businesses consider for commercial auto insurance?

Carry at least a $1 million combined single limit (CSL) or $1 million per-occurrence liability as a practical baseline, and buy higher limits or an umbrella policy when your exposures (vehicles, cargo, employee drivers, or contractual requirements) could exceed ~$500,000. Plans marketed to small businesses range from $100K CSL for basic coverage up to $1M CSL for “best” coverage, and large buyers (e.g., Walmart) often require $1M per occurrence and $2M aggregate. Match limits to vehicle/cargo value, contract/vendor insurance requirements, and potential lawsuit severity.

Are all business vehicles and drivers automatically covered under a commercial auto policy?

No, commercial auto policies generally cover vehicles owned by the business and employees operating those company vehicles, but they do not automatically cover rented, leased, or employee-owned (non‑owned) vehicles. To insure rented, leased or personal cars used for business you must add Hired and Non‑Owned Auto (HNOA) coverage or a specific endorsement. Personal auto policies also typically won’t cover accidents that occur while the vehicle is being used for business, so check your policy language and endorsements.

What specific actions can a small business take to lower commercial auto insurance premiums (e.g., driver training, telematics, vehicle selection)?

Hire and vet drivers (MVR and background checks), require defensive-driving and distracted-driving training with documented completion, and enforce drug/alcohol testing and a written cell‑phone policy. Install telematics/IVMS and GPS (speeding, harsh‑braking, hours logged), choose newer vehicles with ADAS/automatic emergency braking and anti‑theft devices, keep strict maintenance and mileage limits, and route‑plan to reduce miles. Bundle policies, raise selective deductibles, keep clean loss runs, provide insurers telematics/loss data and training certificates for discounts, and shop carriers or usage‑based/pay‑per‑mile programs via a broker.

Does commercial auto insurance cover employees who use their personal vehicles for business (hired and non‑owned autos), and how do I add that protection?

No, commercial auto policies don’t automatically cover employees driving their own or rented cars for company business; you must add Hired and Non‑Owned Auto (HNOA) coverage (aka Hired/Non‑Owned Auto Liability) to protect the business for liability arising when employees use personal or rental vehicles on the job. Add it by requesting the HNOA endorsement from your insurer or agent (provide details on employee drivers, estimated business use and rental exposure); note HNOA generally covers liability only, buy hired auto physical damage or require employees’ personal policies to cover collision/comprehensive, and consider higher limits or an umbrella for excess exposure.

What documentation and vehicle/driver details will insurers require to produce an accurate commercial auto insurance quote?

Insurers will want business documentation: legal business name, industry, EIN/FEIN, years in operation, number of employees, annual revenue, all business locations/garaging ZIP codes, current policy declarations and 3-5 years of loss runs/claims history. For each vehicle supply VIN, year/make/model, GVWR or class, ownership status (owned/leased/rented/personal/hired‑non‑owned), primary use (deliveries, service, commuting), annual and business mileage, garaging address, safety/anti‑theft equipment, registrations/titles and lease agreements. For each driver provide full name, DOB, driver’s license number and issuing state, years licensed, driving record (tickets, accidents, DUIs), employee/contractor status and any training or endorsements (CDL), plus your desired limits/deductibles and disclosure of hired/non‑owned vehicle exposures.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to eCommerce business insurance.

Related: What Is Not Covered By The Commercial General Liability (CGL).

Related: How Much Is Commercial General Liability Insurance? What It Covers.

Sources

- insureon.com

- travelers.com

- usnews.com

- progressivecommercial.com

- geico.com

- progressivecommercial.com

- nationwide.com

- constructioncoverage.com

- moneygeek.com

- kin.com

- bankrate.com

- progressive.com

- allstate.com

- insure.com

- bankrate.com

- nextinsurance.com

- quora.com

- allstate.com

- valuepenguin.com

- statefarm.com

- pgicentralflorida.com

- geico.com

- thehartford.com

- biberk.com

- geico.com

- progressivecommercial.com

- thehartford.com

- thehartford.com

- thehartford.com

- berxi.com

- vargasinsurance.com

- insuredbetter.com

- deloitte.com

- piainsagency.com

- score.org

- progressive.com

- macombinjurylawyers.com

- bfg.law

- noblepagroup.com

- insureon.com

- thehartford.com

- forbes.com

- allstate.com

- nerdwallet.com

- thimble.com

- esportsinsurance.com

- coastgeneralinsurance.com

- ace.aaa.com

- checklistguro.com

- moneygeek.com

- thehartford.com

- assureful

- hippo.com

- progressive.com

- insureon.com

- marketwatch.com

- gocallhub.com

- cnbc.com

- insureon.com

- thelawspot.com

- withpocket.com.au

- uhc.com

- dealhub.io

- regulaforensics.com

- controlhub.com

- moensheehanmeyer.com

- payoneer.com