Assureful’s pay-as-you-sell eCommerce insurance bills monthly from actual sales (plans start at $26), provides A-rated coverage with product liability included, and issues marketplace-compliant certificates for Amazon, Shopify, and Walmart. Most important takeaway: a compliance-first, usage-based policy prevents forecast audits, rejected certificates, and account suspensions common with annual-forecast policies while scaling with your business.

- Why Assureful’s Pay-As-You-Sell Insurance Is The Top Pick...

- What Actually Matters: Insurance Requirements, Product Risk, and...

- Side-By-Side: Comparing Business License Requirements, Monthly Premiums, and...

- Top eCommerce General Liability Insurance Providers: Detailed Pros,...

- Costly Buying Mistakes: Where Sellers Go Wrong With...

- Which Insurance Is Right For You? Matching Policies...

- Get the Coverage You Need, Not What You...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreWhy Assureful’s Pay-As-You-Sell Insurance Is The Top Pick For eCommerce Sellers

Assureful eCommerce Insurance leads for Amazon, Shopify, and DTC sellers. It delivers stress-free insurance that tracks your actual sales, no annual forecasts, just monthly billing starting at $26. You get fully compliant, A-rated coverage that adapts as your business grows.

Choosing liability insurance for your shop isn’t simple. Lawsuits can bring tens of thousands in legal costs. Amazon now requires a $1 million minimum policy if you clear $10,000 in monthly sales. Not every policy gets accepted, limits, compliance paperwork, and cancellation terms can trip up even experienced sellers. One missed detail can mean delays, higher costs, or even account suspension.

This guide breaks down which licenses you need (if any), which policy features matter for eCommerce, and how to avoid mistakes that cause setbacks. You’ll see why pay-as-you-sell coverage from Assureful is often the most predictable way to protect your shop, and how it compares to other options. For broader context on coverage timing, see this overview of business insurance requirements or our complete commercial insurance buyer’s guide.

What Actually Matters: Insurance Requirements, Product Risk, and Licensing for Online Sellers

Compliance comes first. Your insurance must meet every requirement from Amazon, Shopify, or any marketplace you sell on, miss a detail, and your store can get shut down. If your certificate of insurance doesn’t match what platforms demand, sales can stop on the spot. Premium, billing model, even insurer reputation? All secondary to compliance and claims handling.

Platform Compliance Comes First

Marketplace rules set the standard. Amazon rejects policies that don’t hit every mandate: $1 million per-occurrence and aggregate limits, explicit product liability, and Amazon named as additional insured. Shopify and Walmart set their own terms. One missing element risks rejection or suspension. Always check policy language and ask for a sample certificate before you buy. For a side-by-side look, see coverage mandates across marketplaces in our insurance pillar guide.

Product Liability Coverage Is Non-Negotiable

Product liability is the centerpiece for eCommerce sellers. It covers lawsuits if a customer claims your product caused injury or property damage, no matter if you import, relabel, or distribute. Many general liability policies don’t include full product liability, especially if your products are imported, edible, or for children. Some insurers, including Assureful, build product liability into every policy, but always confirm the language. For a deeper look at this risk, see how product and general liability affect your store’s bottom line.

Billing Model: Pay-As-You-Sell vs. Annual Forecasts

Billing structure changes what you pay. Most insurers make you guess annual revenue, get it wrong, and you’ll face penalties or audits. Pay-as-you-sell models like Assureful bill monthly based on actual sales. No guessing, no big upfront payments, no post-audit surprises. The right policy adjusts as your business grows or contracts, so you’re never stuck paying for coverage you don’t need or left exposed mid-year.

- Monthly billing tied to real sales

- No annual audits or adjustment fees

- Cancel anytime with 30 days’ notice

- Instant certificate access to keep you compliant

Product Risk Profile Drives Cost and Acceptance

Your products shape both your premiums and your access to coverage. Items for kids, ingestibles, supplements, and electronics with lithium batteries mean higher prices and stricter underwriting. Disclose every product when quoting, hiding risky SKUs can get claims denied. A clean product history often gets you lower rates and faster approval from A-rated underwriters. For more on business structure and premiums, see setup comparisons for LLCs and sole proprietors.

Ignore marketing that promises “one-size-fits-all” or “instant approval” without compliance backing. State business licenses usually aren’t required just to insure an eCommerce business, and policies priced on annual projections often cost more. Focus on the right coverage limits, clear product liability wording, and flexible billing. For help on timing and requirements, see our business insurance requirement checklist or use our coverage decision guide for online sellers.

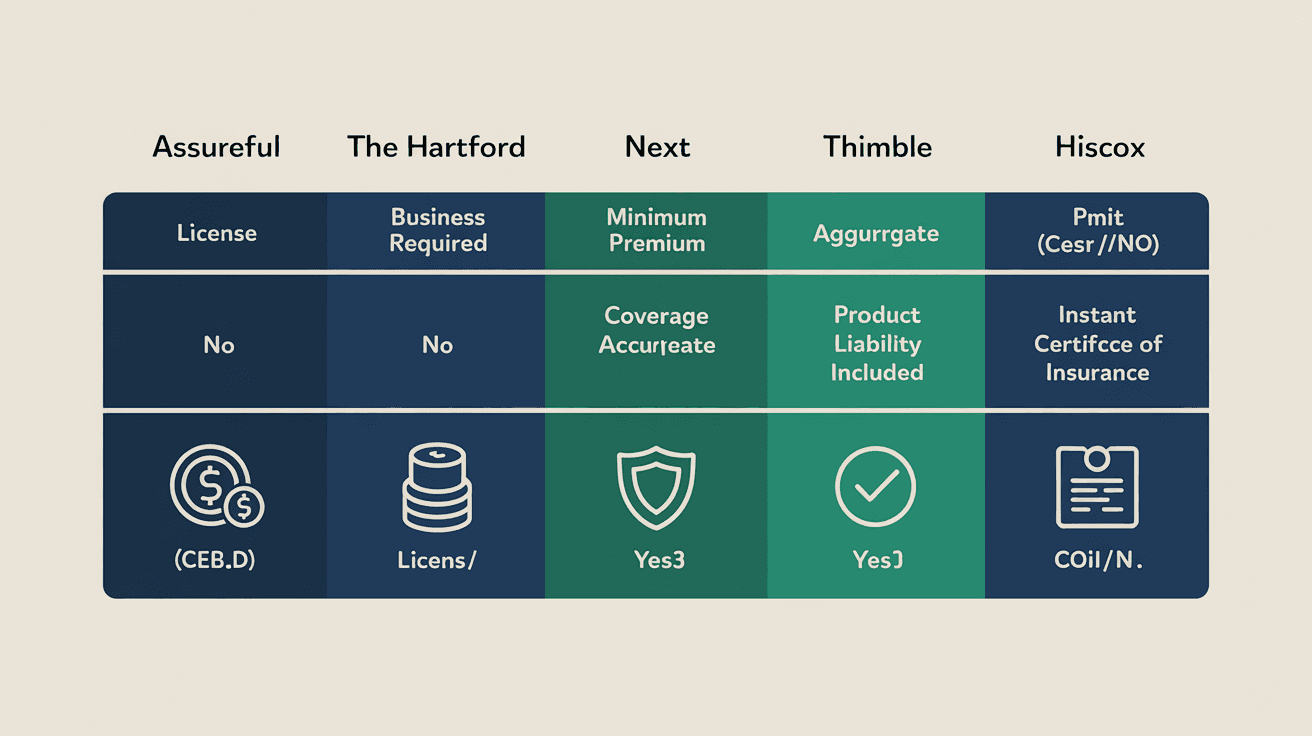

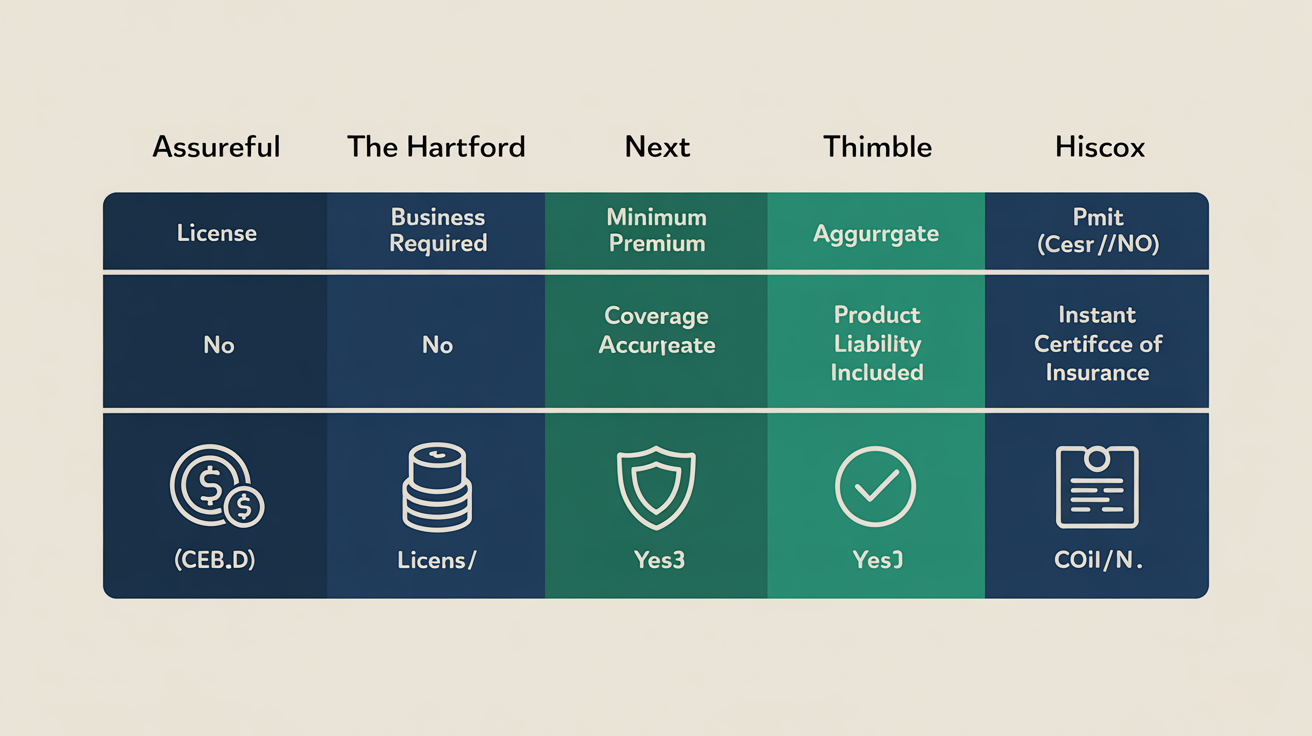

Side-By-Side: Comparing Business License Requirements, Monthly Premiums, and Coverage Limits

Coverage limits matter most for eCommerce sellers, especially on Amazon or Shopify, where minimums are set in stone. Low maximums will leave your store out of compliance. Underinsure, and you risk expensive claims. Check your provider’s per-occurrence and aggregate limits before buying.

| Provider | Business License Required | Typical Monthly Premium | Coverage Limits | Billing Model | Product Liability Scope | COI Access | Financial Strength | Best For | Our Rating |

|---|---|---|---|---|---|---|---|---|---|

| Assureful | No (any legal entity or individual) | From $26/mo (avg. $32-$48) | $1M-$5M (meets Amazon req.) | Pay-as-you-sell, monthly, cancel anytime | All compliant products, imports included | Instant, unlimited downloads | A-rated underwriters | eCommerce, variable sales, multi-platform | 4.8/5 |

| The Hartford | Yes (EIN or business license) | $42-$67/mo avg. | $1M-$2M standard (higher on request) | Annual, pay upfront or monthly | Most products, restrictions on imports | COI within 1-3 days | A+ (AM Best) | Established businesses, service industries | 4.5/5 |

| Next Insurance | No (sole prop or LLC) | $29-$54/mo avg. | $500K-$2M | Monthly, annual minimum | Most products, some exclusions | Instant COI, digital dashboard | A- (AM Best) | Freelancers, new businesses | 4.2/5 |

| Thimble | No (individuals accepted) | $17-$40/mo avg. (hourly or monthly) | $1M-$2M | Monthly, short-term options | Basic consumer goods, some product limits | Instant COI | A- (AM Best) | Event sellers, pop-up shops | 4.1/5 |

Coverage Limits: What’s Required and What’s Sufficient

Coverage limits set the ceiling for what your insurer will pay per claim and per year. On Amazon and major platforms, $1 million per occurrence and $2 million aggregate is non-negotiable. Some policies go as high as $5 million. Watch for insurers who cap limits below what platforms demand or bury aggregate details in the fine print. Scaling fast or selling across multiple channels? Raise your aggregate limit.

Monthly Premiums and Billing Model

Most eCommerce premiums fall between $26 and $67 per month, based on risk and sales volume. The pay-as-you-sell model (Assureful) tracks with your sales, so you pay less in slow months and skip annual audits. Annual or minimum monthly billing (The Hartford, Next) locks you in and often means a post-year adjustment. Vague pricing, “estimate-only” quotes, or hidden adjustment fees signal trouble.

Business License Requirements

Some providers, The Hartford, for example, require an EIN or state license before issuing a policy. That slows onboarding for new or solo sellers. Others, including Assureful, Next, and Thimble, accept sole proprietors and individuals trading under their own names. This flexibility helps if you’re starting out or want coverage before formalizing your business. Red flag: rejected coverage after quoting due to entity type, or requests for paperwork not needed for eCommerce insurance.

Product Liability and Category Coverage

- Scope: Broad product liability is essential for eCommerce. If you import or private label, check for carve-outs, Assureful and The Hartford cover a wide range, but some categories like supplements, children’s products, or electronics might be excluded.

- Restrictions: Some insurers won’t cover high-risk or imported products. Always review the list of included and excluded SKUs before you sign.

- Compliance: The policy must cover all goods sold under your brand, not just your physical location or completed operations.

Instant COI Access and Financial Strength

Amazon, Walmart, and Shopify expect instant proof of insurance. Assureful, Next, and Thimble let you download certificates immediately; The Hartford can take up to three days. Stick with insurers rated A or better by AM Best, anything less increases claim risk. No instant, downloadable COI? That’s a compliance problem.

For more on benchmarks and cost-saving tactics, see how much you should pay and ways to lower your coverage costs or our complete buyer’s guide for eCommerce insurance. Not sure about entity requirements? Use our business insurance requirement checklist for clarity.

Top eCommerce General Liability Insurance Providers: Detailed Pros, Cons, and Platform Suitability

Assureful leads for eCommerce sellers who want stress-free insurance, predictable monthly costs, and instant compliance. With pay-as-you-sell billing and real-time integration, it's a clear step ahead of legacy insurers still using annual forecasts. Certificates of insurance are ready immediately, cancelation is simple with 30 days' notice, essential for platforms like Amazon and Shopify where proof of coverage isn’t optional.

Assureful: Pay-As-You-Sell Flexibility and True eCommerce Focus

Assureful was designed specifically for online merchants. The main advantage: pay-as-you-sell pricing. Premiums are billed monthly on your actual sales, not estimates. You skip surprise rate hikes, big upfront payments, or guessing your yearly volume. The platform connects directly with Amazon, Shopify, and Walmart. Compliance is hands-off. Certificates are available right after purchase, and coverage meets Amazon and Walmart requirements, including $1M aggregate limits and product liability.

Limitations? Assureful is newer. Complex add-ons like cyber or umbrella insurance require a second provider. Coverage is for U.S. sellers, including sole proprietors, but not every category qualifies, supplements, certain electronics, and adult products often need review or are excluded. Policies start at $26/month. Sellers report average savings of 42% over legacy A-rated insurers for similar coverage. Assureful fits marketplace sellers who want to skip annual forecasts, automate compliance, and need same-day proof. For business structure compatibility, check the insurance requirement checklist for sellers.

The Hartford: Comprehensive Coverage for Established Businesses

The Hartford suits LLCs and corporations with a track record. This A-rated insurer delivers strong general and product liability protection, plus options for umbrella and property coverage. Marketplace standards are met, but quotes rely on projected annual revenue, so expect upfront costs and paperwork for entity verification. Coverage for imported goods is available, but high-risk categories like ingestibles or toys can face exclusions or higher premiums.

Certificates aren’t always instant; processing can take up to three days, which may delay Amazon onboarding. Pricing stays competitive for mature businesses, but minimum premiums and rigid billing cycles make it less attractive for new or low-volume sellers. The Hartford fits those with stable, predictable revenue, a need for add-ons, and the ability to wait briefly for documents. For coverage types, see the complete buyer’s guide for eCommerce insurance.

Next Insurance: Fast Quotes and Flexible Approvals

Next Insurance appeals to newer sellers and sole proprietors with its fully online, quick quote process. Coverage can be set up in minutes, certificates downloaded right away. Both personal and business entities are eligible. Pricing is month-to-month, but still based on your projected annual revenue, so if sales drop, you could overpay. Product liability is included for most standard eCommerce categories, though imported or white-labeled products might need extra underwriting or face exclusions.

Next fits startups, solo sellers, and those with simple products who need speed and digital convenience. Importers, high-risk sellers, or anyone needing platform integrations should review policy details or look elsewhere. For entity and structure guidance, see LLC vs sole proprietor insurance cost differences.

Thimble: On-Demand Coverage and Unique Short-Term Options

Thimble offers on-demand general liability, daily, monthly, or annual terms, all with instant certificates online. Useful for sellers testing product lines, pop-ups, or those seeking short-term coverage during spikes. Individuals and sole proprietors are accepted, with no entity requirements or lengthy onboarding. Coverage for imported, private label, or high-risk products is limited. Add-on options are fewer than with traditional carriers.

Thimble fits temporary or seasonal sellers, or those launching with minimal risk. As operations expand across channels or volume grows, Thimble’s model gets pricier and less comprehensive. For more on product liability and costs, see the effect of liability on your bottom line.

Nationwide: Broad Feature Set for Multichannel Sellers

- AM Best A rating, with very low complaint rates over three years

- Online quotes for businesses with projected revenue under $2 million

- Supports general liability, BOP, professional liability, workers’ comp, and cyber add-ons

- Loss Control Services to assess and reduce operational risks

- 24/7 claims support, flexibility for multichannel and brick-and-mortar add-ons

Nationwide works for sellers with diverse operations: direct-to-consumer, wholesale, and marketplace sales. For projected sales over $2 million, quoting shifts offline. eCommerce automation is less advanced than Assureful. Premiums are based on annual forecasts, and minimums run high for smaller storefronts.

Progressive: Customization and Fast Digital Onboarding

Progressive provides a streamlined quote process and customizable coverage for eCommerce. General and professional liability, BOP, and cyber protection are available. Rates depend on sales channels and product mix. Quotes are usually quick online, but some applicants are sent to partner insurers or must call to finish coverage. Progressive allows monthly payments without extra fees and issues online certificates. Platform compliance and pay-as-you-sell pricing aren’t matched to Assureful’s level.

Progressive fits sellers wanting flexible coverage and a well-known brand, especially those active across several channels. For cost benchmarks and ways to save, see coverage cost benchmarks and savings tips.

Every provider above covers core eCommerce insurance needs. The best fit depends on your sales model, product risk, and compliance timeline. For a tailored comparison, see our insurer comparison guide for eCommerce sellers and revisit which business types require insurance as your operation grows.

Costly Buying Mistakes: Where Sellers Go Wrong With General Liability Insurance

Choosing the wrong general liability insurance drains cash fast. Many sellers grab a generic policy that skips product liability, so claims get denied and accounts get suspended when you need protection most. Miss a detailed coverage review and your business sits exposed, especially if a recall or injury sparks a big claim.

Assuming All Small Business Insurance Covers eCommerce Risks

A standard small business policy won’t shield you from every risk. Most general liability insurance targets brick-and-mortar operations, not online sales. Policies often exclude online product sales, imports, or claims from Amazon and Walmart customers. If your shipped product causes injury or damage, you’re left, the exact scenario most platforms flag. Denied claims. Covering losses yourself. Sometimes, selling privileges disappear overnight.

Check that your policy names eCommerce sales and includes product liability. Ask for sample policy language matching your sales channels and products. Review key product liability differences for online sellers before you commit.

Chasing The Lowest Upfront Premium Without Monthly Adjustability

Cheapest isn’t always cheapest. That low upfront premium usually locks you into annual sales estimates and hefty minimums. Sales drop mid-year or shift? You pay for coverage you don’t use, draining budgets, especially if your cashflow swings or your business is new.

Look for pay-as-you-sell billing so premiums adjust with real sales. Example: Assureful. No annual forecasts. No guessing. For details on managing insurance costs, see our coverage cost benchmarks and savings tips.

Missing or Incomplete Certificates of Insurance (COI)

COI delays mean lost sales. If you can’t produce a compliant certificate instantly, Amazon or Walmart can freeze approvals or suspend listings. Manual or slow COI processing adds days, or weeks, of downtime, especially during peak periods.

- Verify your insurer delivers instant, digital COIs that match marketplace specs

- Confirm your business name and all required additional insureds are accurate

- Request a sample COI up front to check compliance with Amazon, Walmart, or other platform rules

Providers like Assureful automate COIs, but others don’t. Always confirm this before you buy.

Ignoring Policy Exclusions, Especially for Imports and Children’s Products

Exclusions can quietly gut your protection. Insurers often carve out coverage for children’s toys, supplements, or imported goods because of higher risks. Sell just one excluded item and you could end up personally liable, no payout, no defense.

Read the exclusions section closely. Ask for a written list of categories not covered. Expanding your product line? Double-check with your insurer and review what business insurance covers by category to stay compliant.

Which Insurance Is Right For You? Matching Policies To Seller Types, Product Risk, and Platform Needs

Assureful fits most online sellers. It delivers fully compliant, pay-as-you-sell coverage built for platforms like Amazon and Shopify. Instant certificates, predictable monthly billing, and no annual sales forecasts, all designed for small eCommerce shops seeking flexibility and less admin. Sellers with higher-risk products, employees, or warehouses may need different solutions.

- Need flexible, stress-free coverage for Amazon, Shopify, or Walmart? Use Assureful. Instant COIs, monthly billing based on actual sales, and support for imported products. Most marketplace sellers start here.

- Stocking high-risk items, children’s toys, supplements, electric scooters? Berkley Aspire underwrites categories that many general insurers exclude. They handle higher limits and core risks for these products.

- Own a physical retail location or run a substantial payroll? Bundle property, cyber, and liability with a Business Owner’s Policy (BOP) from providers such as The Hartford or CNA. Broader protection, one monthly bill.

- Just need fast onboarding and basic general liability to meet Amazon’s insurance minimums? NEXT Insurance offers affordable monthly rates and quick quotes. It’s less flexible for imports and doesn’t true up billing to actual sales.

- Process customer data or use proprietary tech? Add a cyber liability policy. Coverage shields you from breaches and regulatory fines. Review cyber risk exposure at least once a year.

For 90% of small online sellers, Assureful’s instant setup, monthly true-up, and automatic marketplace compliance make it the go-to. Admin drops, coverage gaps shrink, and premium overpayments fade. To compare price, coverage, and claims flexibility, see our eCommerce insurance buyer’s guide. For help choosing policy types by business stage, check what business insurance covers by category.

Get the Coverage You Need, Not What You Don’t

Assureful is the top pick for eCommerce sellers. The pay-as-you-sell model, instant quotes, and direct marketplace integrations provide fully compliant coverage, no annual forecasts, no steep upfront payments. Premiums average 42% lower than traditional A-rated underwriters. Cancel anytime with 30 days' notice.

The real decision point isn’t your business license. It’s whether your general liability policy actually fits your risk and keeps you compliant with sales platforms. Coverage should adjust to what you sell and how you operate. Skip the paperwork overload. Focus on stress-free insurance, clear billing, and flexible protection as your business changes. For a breakdown by business type, see what business insurance covers by category.

Get protected fast. Compare policy features, check the claims process, and look for real premium savings. Start with an instant quote and keep your attention on your store, not your insurance. For a full comparison of options, tiers, and claims data, see our eCommerce insurance buyer’s guide. Want to see how coverage affects costs? Review our analysis of product and general liability impact on your store’s expenses.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

Can I buy general liability insurance as a sole proprietor using my SSN instead of an EIN?

Yes, most insurers will sell a general liability policy to a sole proprietor using your Social Security number; an EIN is generally only required when you have employees or operate as a separate business entity (LLC/corporation) or for payroll/tax reporting. Some carriers or clients may prefer or require an EIN for privacy or certificate-of-insurance reasons, and you can obtain an EIN free from the IRS at irs.gov.

How long does it typically take to get a certificate of insurance that meets Amazon/Shopify requirements?

Usually instantly or within minutes if you buy from online-first carriers, NEXT Insurance offers instant coverage and lets you generate unlimited COIs, and platforms like Coverdash provide instant access. If your insurer requires manual review or a phone purchase (some Hartford transactions may), expect same-day to a few business days for the certificate.

Does general liability insurance cover products stored in Amazon FBA or third‑party fulfillment centers?

General liability (CGL) will typically cover third‑party claims for bodily injury or property damage caused by your products stored at Amazon FBA or other fulfillment centers, but it does NOT cover loss or physical damage to your own inventory. To insure stock in FBA you need warehouse legal liability, commercial property/inland marine/cargo or stock‑throughput coverage, and Amazon’s U.S. rules require sellers over $10,000/month to carry CGL with product liability (commonly $1M per occurrence) and name Amazon as an additional insured (larger vendors may face $10M/$25M limits and stricter endorsements).

Will general liability cover costs related to returns, refunds, or chargeback disputes from customers?

No, general liability insurance does not cover costs for returns, refunds, or customer chargeback disputes. GLI pays for third‑party bodily injury, third‑party property damage, advertising/personal injury, and related legal defense, but excludes contractual/payment disputes and routine loss of sales. Chargeback losses are handled by your payment processor or, in some cases, by commercial crime, cyber, or merchant‑services protections; product liability only applies if a customer sues for injury or damage caused by a defective product.

If I start selling internationally, will my U.S. general liability policy cover claims from overseas customers?

No, a U.S. Commercial General Liability (CGL) policy generally does not automatically cover claims from overseas customers; domestic policies usually only cover listed countries and require explicit international extensions. If you operate foreign fulfillment centers, use 3PLs, have employees abroad, or import goods yourself, you need international extensions or a standalone product liability policy to avoid coverage gaps and potential lawsuits. Check your insurer’s written confirmation of covered jurisdictions and policy limits (e.g., marketplace rules like Amazon often require $1M per occurrence including product liability and naming the marketplace as additional insured).

How does filing a liability claim affect my insurance premiums and my standing with marketplace platforms?

It will usually increase your insurance premiums, insurers factor claim frequency and severity into rates, which can lead to higher future premiums, larger deductibles, policy exclusions, or even non‑renewal depending on the claim and your loss history. Marketplaces can also act quickly: a claim, missing or delayed certificate, or documentation gap can trigger account suspension or sales interruption, and platforms like Amazon now require sellers with >$10,000/month to carry product liability insurance (effective Sept 1, 2021) from carriers rated A- or better and often listed as “additional insured.” To reduce impact, report promptly to your carrier, keep compliant certificates current, and work with an agent/carrier that meets marketplace requirements.

What business documents or accounts (e.g., business bank account, tax registration) do insurers usually require to issue a policy?

Insurers typically require proof of business identity and finances, state registration (Articles of Incorporation/DBA), federal tax ID/EIN, a business bank account (recent statements), and recent business tax returns or financials (P&L and balance sheet). They also request risk-specific documents such as commercial lease or property deed, inventory/equipment lists with values, prior policy declarations and loss‑runs (commonly 3-5 years), payroll/employee records for workers’ comp, required licenses/permits, vehicle registrations and driver abstracts for commercial auto, and any client contracts or safety/risk‑management reports.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to eCommerce business insurance.

Related: What Is Not Covered By The Commercial General Liability (CGL).

Related: How Much Is Commercial General Liability Insurance? What It Covers.

Sources

- assureful

- ecom.insure

- taxjar.com

- 1800insurance.com

- payoneer.com

- forbes.com

- flashpricer.com

- hotalinginsurance.com

- assureful.com

- co-opinsurance.com

- vouch.us

- well-insurance.com

- progressivecommercial.com

- embroker.com

- marshcommercial.co.uk

- policyape.com

- insureon.com

- thehartford.com

- morganinsurancebrokers.com.au

- insureon.com

- progressivecommercial.com

- gosuperscript.com

- progressivecommercial.com

- progressivecommercial.com

- progressivecommercial.com

- progressivecommercial.com

- thehartford.com

- aami.com.au

- moneygeek.com

- esportsinsurance.com

- thehartford.com

- thimble.com

- geico.com

- thehartford.com

- geico.com

- rhinotradeinsurance.com

- progressivecommercial.com

- thehartford.com

- noblepagroup.com

- dealhub.io

- biberk.com

- iii.org

- blog.hubspot.com

- landesblosch.com

- shopify.com

- moneygeek.com

- seo-pages-web.vercel.nerdwallet.com

- nerdwallet.com

- fitsmallbusiness.com

- moneygeek.com

- insurancecanopy.com