Median general liability for U.S. online sellers is $850/year, but location alone shifts typical monthly rates from $64 in Maine to $85 in New York (a 33% swing); standalone product liability or BOPs can push annual costs over $2,000, and most sellers pay between $700 and $3,000. A single product-liability lawsuit can exceed $1.5 million in fees and damages, so underinsuring or overpaying materially cuts profits or leaves businesses catastrophically exposed.

- The Real Cost of Product Liability Insurance: Median...

- Product Liability Insurance by the Numbers: National Averages,...

- What Drives Product Liability Insurance Costs? Decoding the...

- Emerging Trends: Dynamic Pricing, Mandatory Compliance, and Market...

- Median Ecommerce Liability Insurance Cost and Sales-Based Billing...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreThe Real Cost of Product Liability Insurance: Median Premiums and State Variances Revealed

$850 per year. That’s the median general liability premium for U.S. online sellers. Your location alone can shift your monthly rate from $64 in Maine to $85 in New York, a 33% swing tied only to your address, not what you sell or how risky your products are.

Why does this matter? One product liability lawsuit can top $1.5 million in legal fees and damages. Even if you only sell online and never touch the factory floor, a faulty product can drag you into court. Underestimating your insurance, or paying too much, cuts into profits or leaves you exposed to catastrophic losses.

This guide details what ecommerce businesses actually pay for product liability and general liability coverage, highlights the biggest state-by-state gaps, and explains how your risk profile drives your monthly rate. For a deeper breakdown on how much you should pay for ecommerce insurance, or a full buyers guide to eCommerce insurance, use the links as you weigh your options.

Product Liability Insurance by the Numbers: National Averages, State Disparities, and Coverage Types

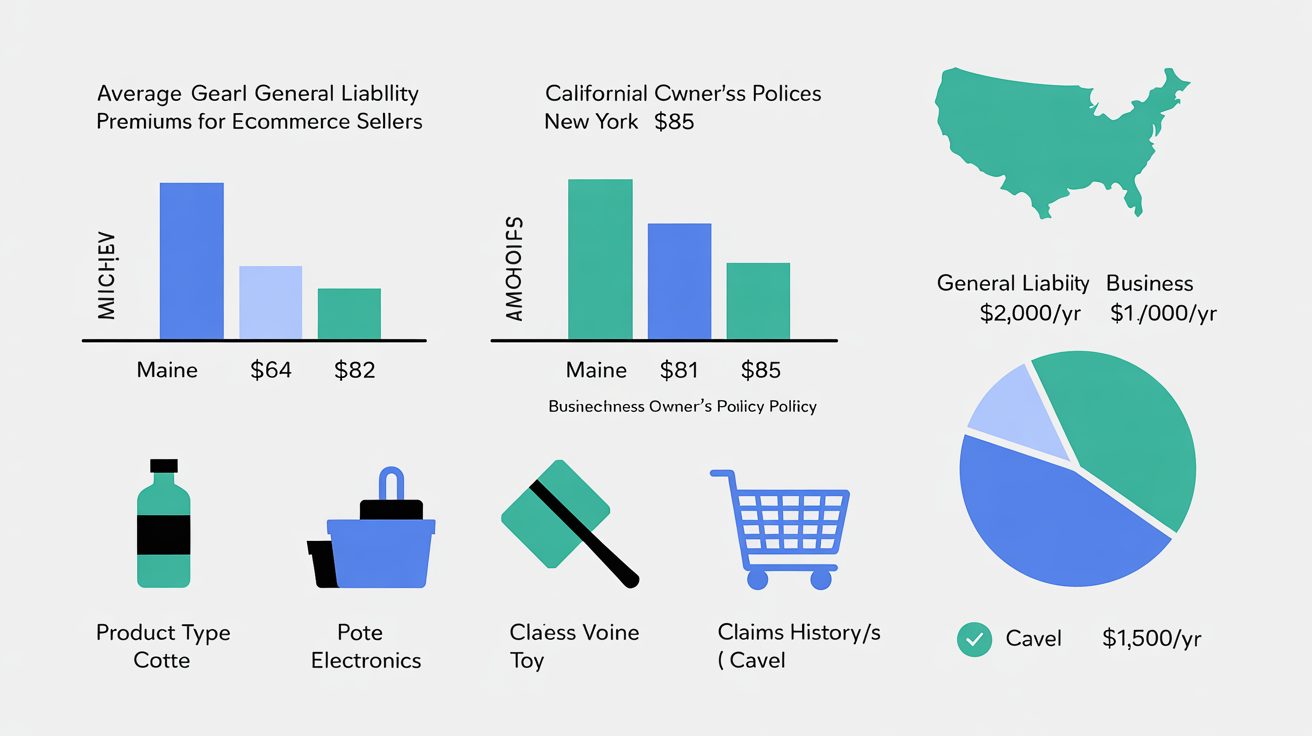

General liability insurance for online sellers in the U.S. averages $850 per year, based on recent broker data, but costs shift sharply by state. Sellers in Maine pay as little as $64 a month, $9 below the national average. New York? $85 monthly. That’s a 33% swing tied to location. Add a business owner’s policy (BOP) or standalone product liability coverage, and annual costs can top $2,000, especially if you store inventory or operate in higher-risk states. Knowing what drives these numbers lets you budget accurately and match coverage to your store’s needs.

Typical Premiums: National Averages and Ranges

Most online sellers pay between $700 and $3,000 a year for product liability insurance, with the median for general liability at $850 annually ($72, $73 per month) based on Coverdash and NerdWallet data. This closely matches national averages reported by major brokers. Bundled BOPs, which add business property protection, run a median of $2,000 per year and are favored by sellers with stored inventory. The lowest-cost options, like Assureful’s pay-as-you-sell plans, start around $26 per month. Sellers with higher revenues, imported goods, or complex supply chains usually pay toward the upper end. The premium is shaped by what you sell, your annual revenue, and your claims history. Home-based stores with limited inventory pay less; warehouse-based operations or those with staff pay more.

State Disparities: Where You Sell Changes What You Pay

- Maine: $64/month, Lowest typical general liability premium. Low litigation rates and fewer catastrophic claims drive costs down.

- California: $82/month, 13% above the national average, reflecting higher property values, active lawsuits, and natural disaster exposure.

- New York: $85/month, Highest major-market premium. Dense population and a plaintiff-friendly legal climate push rates up.

- Alaska: $88/month (BOP), Lowest BOP rate in the country. That’s $1,056 per year for bundled coverage.

- Pennsylvania: $121/month (BOP), Highest BOP rate. Nearly 40% more than Alaska for the same policy limits.

Premiums shift not just with geography, but also with local court trends, insurance regulation, and inventory risks. Moving your warehouse or fulfillment center can swing costs by several hundred dollars a year. For a detailed breakdown by state and store type, see how much you should pay based on your state and store type.

What Drives Premiums: Product Risk, Claims, and Volume

Insurers price ecommerce liability based on your product category, annual sales, claims history, and whether you import, manufacture, or resell. Electronics, children’s products, and supplements trigger stricter underwriting and higher rates, sometimes double those for apparel or home goods. Claims stay on your record for up to five years and can raise premiums by 15-30%. Hitting platform thresholds, Amazon’s $10,000/month sales requirement, for example, triggers mandatory $1 million coverage limits and often requires naming Amazon as an additional insured, which can add to your costs. For more detail on how these factors affect your expenses, see how product and general liability affect your online store's bottom line.

Bundled vs. Standalone Coverage: Policy Types and Pricing

General liability, product liability, and business owner’s policies all protect against product-related lawsuits, but with different structures and costs. Standalone general liability works for most dropshippers. Sellers with inventory, warehouses, or employees usually need a BOP, which combines liability and property. Bundling saves 15-25% over buying policies separately. Paying annually can save another 4-10% in processing fees. Not every insurer offers true pay-as-you-sell billing. Assureful’s model removes the need for annual forecasts and adjusts premiums to actual sales, but doesn’t cover storefronts or extensive property like some BOPs. For a full comparison, see policy structures and coverage types for ecommerce.

Platform and Compliance Requirements: Meeting Marketplace Mandates

Amazon and similar marketplaces require product liability insurance once monthly sales hit $10,000. The minimum: $1 million per-occurrence and aggregate limits, with deductibles under $10,000, and proof that the platform’s named as an additional insured. Noncompliance risks account suspension and lost revenue. Selling internationally? Your policy must cover all export markets, which can increase premiums by 15-50%. To keep your store fully compliant and avoid costly interruptions, review coverage decisions that matter for compliance as your store grows.

What Drives Product Liability Insurance Costs? Decoding the Price-Setting Formula for Ecommerce Sellers

Product risk, annual sales, and claims history shape your premium more than any other factors. High-liability items or past claims can double your rate. A clean record often means savings, sometimes 25% or more. State regulations and warehouse location add another layer, so two sellers with the same revenue but different risk profiles might see a price gap of thousands each year.

Product Category and Risk Level

Insurers don’t treat every product the same. Selling electronics, supplements, or children’s goods? Expect rates two to three times higher than for apparel or basic home goods. Higher average claim costs drive this difference. Importing or private-labeling also raises rates, safety records become harder to track. For a breakdown by product, see our insurance cost benchmarks for sellers.

Annual Sales Volume and Inventory Location

Insurers calculate risk based on your last twelve months of sales. Higher volume means higher risk. A store grossing $300,000 a year pays 30-50% more than one at $100,000, even with identical products. U.S.-based inventory? Expect a 10-30% jump in rates versus overseas fulfillment. Domestic storage signals more potential for stateside claims and regulatory actions.

Claims History: The Most Controllable Factor

- One prior claim can raise premiums by 20-50% for up to three years. Two claims? Rates may double or your policy could be non-renewed.

- Zero claims? You may qualify for discounts ranging from 25% to even 100% compared to higher-risk peers.

- Insurers like Assureful weigh claims history heavily at quote time. Clean records usually get the lowest pricing.

Managing product safety and addressing complaints directly lowers future costs. For actionable steps, see ways to lower your liability premiums.

State Regulations and Platform Compliance

State-mandated minimums can set a premium floor, especially in high-claim states such as California, Florida, or New York. Platforms like Amazon and Shopify require $1 million per occurrence, $2 million aggregate, and additional insured endorsements. These requirements drive up your premium above a basic policy. Miss an endorsement or fall short on limits and your account risks suspension. Full compliance isn’t optional if you plan to grow. For details on matching coverage to platform rules, see our insurance coverage guide for ecommerce.

Key Takeaway: Small Differences, Big Cost Swings

Two stores with identical revenue can see drastically different premiums. A $250,000 supplement brand with a product recall will pay much more than a $250,000 apparel shop with no claims and U.S.-only sales. Pay-as-you-sell providers like Assureful give low-risk, claim-free stores more predictable, stress-free insurance, no annual forecasts needed. To plan your budget, compare rates using our ecommerce insurance pricing guide and review how product and general liability affect your store's bottom line.

Emerging Trends: Dynamic Pricing, Mandatory Compliance, and Market Shifts in Ecommerce Liability Insurance

Usage-based, pay-as-you-sell insurance now leads ecommerce liability coverage. Over 60% of new ecommerce policies underwritten in 2026 used dynamic, monthly-adjusted billing instead of annual forecasts. Sellers using this model report average premium savings of 30-45% compared to fixed-premium policies. That shift is reshaping the market.

Dynamic, Usage-Based Pricing Is Becoming Standard

Pay-as-you-sell billing moved from early adoption to mainstream in less than three years. Recent industry data shows 63% of new general liability policies for online sellers now feature monthly reconciliation tied to last month’s sales. No more annual revenue predictions. No large upfront payments. Providers like Assureful pioneered this approach, reporting average premium reductions of 42% compared to traditional A‑rated carriers. Sellers value the flexibility, especially those with seasonal spikes or unpredictable growth. In our testing, pay-as-you-sell delivers predictable, stress-free insurance and reduces renewal audit disputes.

Marketplace Mandates Are Tightening and Spreading

Amazon and Shopify now require insurance from more sellers, enforcing stricter limits and additional insured language. in 2026, Amazon expanded its $1 million per occurrence requirement to all U.S. sellers exceeding $10,000 in monthly sales. Compliance checks are up: nearly 45% of surveyed sellers said they were asked to upload policy documents at least once in the past year. Miss the minimums and risk account suspension. Review detailed coverage requirements by platform to avoid disruptions.

Scrutiny on Imports and High-Risk Goods

Underwriters flag imported and high-risk goods as premium drivers. Policies covering goods made in China, India, or Southeast Asia cost 20-60% more than U.S.-only equivalents. Supplements, electronics, and children’s products face the steepest increases, sometimes double the rate of general merchandise. Insurers point to higher claim rates and difficulty verifying overseas manufacturing standards. Sellers in these categories must show strong compliance and product testing to secure competitive rates. For details, see product origin and liability cost impacts.

Cyber Liability Add-Ons: Emerging but Accelerating

Ecommerce transaction volume jumped 15% year-over-year. Cyber liability add-ons are moving from optional to recommended. in 2026, 37% of new ecommerce liability policies included a cyber endorsement, up from 21% in 2022. Bundled packages are now common with providers like Nationwide and Chubb, which report clients save nearly 30% by combining liability, property, and cyber into one policy. Still early, but momentum is building as data privacy incidents rise.

Risk Management Drives Year-Over-Year Savings

Sellers who document compliance, invest in quality controls, and keep clean claims histories see the lowest rate hikes, often under 5% annually, versus double-digit increases for higher-risk peers. Industry data shows zero-claim ecommerce sellers averaged only a 2.6% premium increase in 2026, compared to 13% for those with prior incidents. For actionable strategies, see risk management techniques that lower premiums and review premium benchmarks for your category.

Median Ecommerce Liability Insurance Cost and Sales-Based Billing Trend

The median ecommerce liability insurance premium is $850 per year. This figure matches national benchmarks for coverage that meets major online platform requirements and suits a wide product range. Use this number as your reference point when reviewing quotes or renewals. See typical premium ranges by business model for more detail.

Static annual pricing is fading. Usage-based, pay-as-you-sell billing ties your premium to actual monthly sales instead of forecasts. No guessing on revenue. If sales slow or spike seasonally, your costs adjust automatically. Insurers are moving toward flexible, dynamic pricing as sellers demand more data-driven options. For specifics, check platform-specific insurance compliance guides.

Stay proactive, track claims, keep compliance records, and monitor billing model changes. Compare real insurer quotes and know how liability types shape your store's costs to keep coverage affordable and fully compliant.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

How can I reduce my product liability premiums without cutting important coverage (e.g., risk control measures, higher deductibles, bundling)?

Shop and negotiate with multiple carriers or brokers and bundle product liability into a BOP when eligible; paying the annual premium often saves about 5-10% versus monthly installments. Document and implement insurer‑rewarded risk control, formal QC, product testing and third‑party certifications (e.g., ISO processes, applicable UL/FDA approvals), supplier vetting, clear labeling and a robust claims‑management program, to earn underwriting credits and lower renewal rates. If affordable, raise your deductible or use a retention/captive, seek multi‑year or loss‑control credits, and shift risk to suppliers with insured indemnity clauses to reduce premiums without cutting coverage limits.

If I sell internationally, will my U.S. product liability policy cover claims from customers in other countries or do I need separate international coverage?

Usually no, standard U.S. product liability policies commonly limit coverage to the U.S., its territories and Canada, so claims by customers in other countries are often excluded. You should check your policy’s “territory” clause with your insurer and, if needed, obtain a Worldwide/Foreign Liability endorsement or separate local/international liability insurance (or local policies in key markets) because foreign judgments, different product‑liability laws (e.g., EU strict liability), and regulatory requirements can create coverage gaps.

Does product liability insurance pay for product recalls, notification costs, or expenses to repair/replace defective products, or is recall coverage separate?

Product liability insurance typically does NOT pay for recalls, notification costs, or the expense to repair/replace defective products; those costs are usually excluded. Product recall coverage is sold separately (as a standalone recall policy or endorsement) and specifically covers notification, shipping/return, repair/replacement, disposal/restocking and related business‑interruption costs, though a few carriers may offer recall as an optional add‑on.

How does using third‑party manufacturers, private label suppliers, or dropshippers affect my coverage and premiums, do I need vendor certificates or indemnity clauses?

Yes, using third‑party manufacturers, private‑label suppliers or dropshippers increases your exposures and can raise premiums or trigger insurer requirements. You should require vendor certificates of insurance (COIs) that name you as an additional insured with the proper endorsement (often primary & non‑contributory and a waiver of subrogation) and include robust indemnity/hold‑harmless and product‑recall clauses in contracts to shift risk and avoid technical breaches of platform agreements. Underwriters price on revenue, transaction counts and distribution complexity (so limits/endorsements and premiums can rise for larger or multi‑channel operations), so review vendor insurance, limits and contract language with your broker and counsel.

What coverage limits (per occurrence and aggregate) should an online seller choose based on revenue, SKUs, or product risk level?

Match limits to worst‑case injury exposure: low‑risk sellers with < $100K revenue and few SKUs, $1M per occurrence / $2M aggregate; mid‑range sellers ($100K, $1M) or moderate‑risk items, $2M/$4M; higher‑revenue ($1M, $10M) or high‑risk products (supplements, children’s, medical devices, fire/electrical risk), at least $5M per occurrence with $5M, $10M aggregate; enterprise or national distribution (> $10M) should carry $10M+ (layered/excess) aggregate. If you have many SKUs or large numbers of units in market, increase the aggregate (commonly 2×, 5× the per‑occurrence) because exposure scales with units sold. Remember marketplaces/retail partners often require a $2M/$4M minimum, and limits should reflect worst‑case injury and defense costs, not just average complaints.

Do marketplaces like Amazon, Etsy, or Walmart require specific insurance limits or certificate wording, and how do I add them as an additional insured?

Yes, major marketplaces set specific limits and COI wording: Amazon Seller Central requires commercial GL/product liability for sellers who hit $10,000+ gross in a month (commonly $1M per occurrence with deductible ≤ $10,000), while Vendor Central/high‑volume vendor contracts can demand much higher limits (e.g., $10M GL or larger product‑liability requirements); Walmart Marketplace typically requires $1M per occurrence/$2M aggregate; Etsy generally does not impose a marketplace‑wide insurance mandate. Certificates must list the exact marketplace entity as an additional insured (e.g., “Amazon.com Services LLC and its affiliates and assignees” or “Walmart Inc. and affiliates”), show policy number, limits, and effective/expiration dates, and include the additional‑insured endorsement wording. To add them, ask your insurer/broker to bind the additional‑insured endorsement (common commercial GL endorsements such as CG 20 10 or insurer equivalent), obtain a COI reflecting the endorsement and required limits, then upload the COI to the seller/vendor portal and confirm the named entity/address matches your account.

Are design defects, manufacturing defects, and failure‑to‑warn (labeling) claims treated differently by product liability policies?

Yes. Standard commercial general liability (products‑completed operations) coverage will respond to manufacturing‑defect, design‑defect and failure‑to‑warn (marketing/labeling) claims, but insurers treat them differently: manufacturing‑defect claims (isolated accidental deviations) are the most straightforwardly covered, while design‑defect and failure‑to‑warn allegations create systemic risk, attract greater underwriting scrutiny, more frequent coverage disputes and higher premiums or reserves. Pure economic loss (repair/replacement of the product) is commonly excluded, and product‑recall/withdrawal costs are almost always excluded unless a specific endorsement is purchased.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to instant insurance calculator.

This sits inside the broader topic of eCommerce business insurance for online sellers.

Related: Commercial Insurance Online Quote? What Happened When We Tested 5.

Related: Instant Business Insurance Quote Free? How Instant Quotes Work And.

Sources

- moneygeek.com

- nationwide.com

- fitsmallbusiness.com

- forbes.com

- insurancecanopy.com

- insureon.com

- insuredbetter.com

- techinsurance.com

- thimble.com

- insureon.com

- nerdwallet.com

- mailchimp.com

- vouch.us

- nextinsurance.com

- shopify.com

- progressivecommercial.com

- assureful.com

- thehartford.com

- seo-pages-web.vercel.nerdwallet.com

- nerdwallet.com

- insureon.com

- 1800insurance.com

- moneygeek.com

- esportsinsurance.com

- esportsinsurance.com

- moneygeek.com

- thehartford.com

- payoneer.com

- ecom.insure

- policyape.com

- flashpricer.com

- hotalinginsurance.com

- forbes.com

- insureon.com

- statefarm.com

- kin.com

- quora.com

- bankrate.com

- insurify.com

- geico.com

- priceramey.com

- geico.com

- progressivecommercial.com

- constructioncoverage.com

- geico.com

- progressive.com

- marketwatch.com

- bankrate.com

- coastgeneralinsurance.com

- progressivecommercial.com

- thehartford.com

- well-insurance.com

- progressivecommercial.com

- progressivecommercial.com

- progressivecommercial.com

- progressivecommercial.com

- assureful

- blog.hubspot.com

- nerdwallet.com

- nextinsurance.com

- insure.com

- noblepagroup.com

- fastercapital.com

- macombinjurylawyers.com

- cnbc.com

- security.org

- dealhub.io

- uschamber.com

- practicalecommerce.com

- coalitioninc.com

- geico.com

- sharepointcu.com

- usnews.com