Your Coverage Assumption Is Probably Wrong Already

Here is the contrarian take. Paying your premium annually feels responsible. For most eCommerce sellers, it is actually the more expensive choice.

The typical annual-premium path for an eCommerce seller looks like this: a broker quotes $3,000, $4,000 annually based on a forecast the seller estimates at renewal. That number is locked in for 12 months. If the business triples by Q4, a common outcome for sellers who hit a TikTok moment or scale Amazon ads, the coverage limits do not move with it. The seller is paying the same premium for a policy that no longer matches the business it is meant to protect.

The reverse breaks the math too. Over-forecast and the seller pays for 12 months of coverage they never needed. Neither error gets corrected mid-year without an endorsement, paperwork, and usually a fee. The forecast model assumes stable revenue. eCommerce revenue is rarely stable.

This is the trap. Annual premiums lock you into a number you picked before the year began. Your November sales are not your February sales. Your premium should not pretend otherwise.

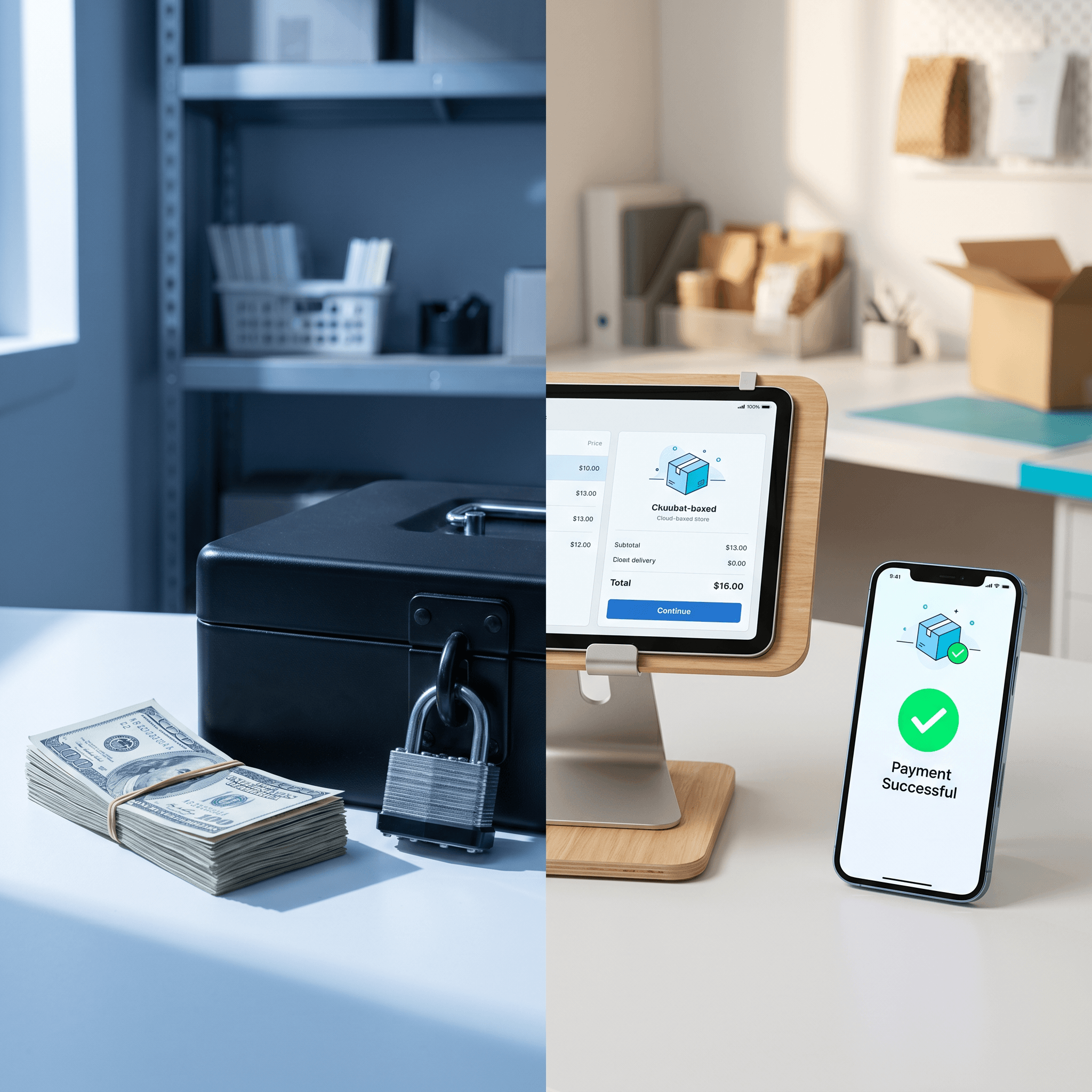

Monthly billing tied to actual sales solves this. Your premium reflects last month's real revenue. You can cancel with 30 days' notice if your needs change.

Before you renew anything, look at the three scenarios below. The billing model changes the math entirely.

Annual Versus Monthly Premiums Are Not Equal Choices

Most insurance comparisons treat this as a simple discount question. Pay annually, save a percentage. Pay monthly, pay a little more for flexibility. That framing misses the actual problem for eCommerce sellers.

Traditional commercial insurance is built on annual sales forecasts. You estimate revenue. Your broker quotes a premium. You pay upfront or finance it. The number is locked in.

This works for a restaurant with stable foot traffic. It works for a law firm billing at fixed rates. It does not work for sellers whose revenue moves.

Q4 alone can triple a seller's monthly volume. A single viral TikTok can double revenue in 72 hours. If your forecast was $600,000 and you finish at $1.1 million, your coverage limits did not grow with you.

The reverse is also true. Forecast too high, and you overpay for coverage you never needed. Neither error gets corrected mid-year without an endorsement, paperwork, and usually a fee.

So what is actually being compared here? Not just annual versus monthly payments. It is a static forecast against real sales data. One number you guessed in January versus what your platform actually recorded last month.

Assureful's pay-as-you-sell structure prices premiums on actual monthly sales. No annual forecast required. Coverage scales with revenue. The gap between these two models matters most for sellers with seasonal inventory spikes or fast growth trajectories, which describes most eCommerce businesses worth insuring properly.

Founders at Waterglider International described the setup as straightforward. Amazon compliance was immediate. No forecast negotiation, no upfront financing decision to stress over.

The billing model is not a footnote. It determines whether your policy fits your business in November the same way it fit in February.

The Real Numbers Most Sellers Never See

Here is the comparison most brokers skip. Not annual versus monthly payment schedules. The real comparison is a number you guessed versus a number your platform recorded.

Traditional policies price on forecasts. You estimate January revenue. The broker locks in a premium. That number does not move.

December arrives. Your actual sales are 40% above forecast. Your coverage limit stayed at February's guess.

A claim lands in December. The policy reflects a number from ten months ago. That gap is where sellers get hurt.

Now run the math in the other direction. Forecast too high in January. Overpay all year. No refund. No correction without an endorsement and a fee.

Assureful's pay-as-you-sell model removes both errors. Premiums bill on last month's actual sales. The floor is $26. That number matters. It kills the objection that stops most small sellers from buying coverage at all.

A seller doing $3,000 a month in revenue finally has a real number to weigh. Not a $4,800 annual quote based on a forecast she barely remembers writing. Twenty-six dollars. Billed on what actually sold. (https://www.underpriced.app/blog/reseller-insurance-guide-2026)

Monthly billing kills the second objection too. Sellers who feel "too small" for insurance are not thinking about a $26 floor. They are picturing the upfront check. Remove the upfront check, and the math changes completely.

Think of it like a SaaS subscription. Your bill reflects usage, not a projection. The mechanics work the same way here. Actual sales drive the number. Not a spreadsheet from last winter.

On average, premiums run 42% lower than comparable programs. Coverage stays compliant. No large upfront cost. No forecast negotiation.

This pattern is common. A policy priced on a 2022 forecast does not adjust when 2024 revenue lands at $1.1M. The coverage never catches up, and most sellers never see the gap until a demand letter arrives.

Paying Upfront Locks You Into Forecasts You Cannot Trust

Here is the contrarian claim: the annual premium discount is not always the better deal. For eCommerce sellers, it is sometimes the more expensive mistake.

Traditional commercial insurance prices your policy on a forecast. You submit a number in January. The carrier prices on that number. Done.

But eCommerce does not move in straight lines. A TikTok video goes viral in March. A supplier in Guangdong ships late in Q3. A new product category doubles your SKU count by October. The forecast you wrote in January is fiction by August.

When reality outpaces that number, sellers end up underinsured. A claim lands, and the payout does not match the exposure. That is the gap. Most sellers never see it until something breaks.

Hiscox research found that most U.S. small businesses lack full coverage. The culprit is rarely indifference. It is a policy anchored to a projection that aged badly. (https://www.insurancebusinessmag.com/us/news/sme/most-us-small-businesses-lack-full-coverage--hiscox-555952.aspx)

The fix requires a midterm endorsement. That means paperwork, a fee, and a conversation with a broker who may or may not respond quickly. Most sellers skip it. The coverage gap widens quietly.

Now flip it. Forecast too high. Overpay twelve months of premium. No refund arrives at renewal. No automatic correction. You paid for coverage you did not need, on a volume you did not hit.

Both errors share the same root cause. The premium reflects a number from the past. Not what you are actually selling right now.

Assureful's billing works differently. Your premium is calculated on last month's actual sales. It adjusts automatically. No endorsement request. No broker call. No forecast negotiation at renewal.

That model removes the structural mismatch entirely. Coverage moves with the business. The business does not have to fit the forecast.

"You're not as covered as you think" is a sharper warning than most sellers expect. Because the policy exists. It's just priced on a version of your business that no longer exists either.

Usage-Based Monthly Billing Fits How Sellers Actually Sell

Here is the contrarian claim. Annual premiums are not cheaper. They are just hiding the true cost inside a forecast you made before you knew what you would sell.

The industry sells annual as stability. The math says otherwise. A 2024 Hiscox study found 77% of U.S. small businesses are underinsured. Most of those businesses pay annually.

The typical audit finding: premium anchored to a 2022 forecast, actual 2024 revenue 38% higher, policy limits unchanged.

She had paid on time every month. She still had a coverage gap. The annual model gave her twelve stale months. No way to self-correct.

Usage-based billing rewrites the contract. Assureful prices your premium on last month's actual sales. Billed monthly. No forecast. No renewal reconciliation.

Sell more in November. Premium reflects November. Sell less in February. Premium reflects February. The policy tracks the business in real time.

Premiums average 42% below similar programs. Policies are backed by A-rated underwriters. Coverage is Amazon and Walmart compliant from day one.

Quotes are instant. Assureful underwrites directly. The platform integrates with Shopify, Amazon, and Walmart. No third-party data sharing required.

Cancel with 30 days' notice. No cancellation penalty. No clawback on unused premium. The commitment matches the cadence of eCommerce itself.

This is the reframe. The question is not monthly versus yearly. The question is whether your premium reflects last year's forecast or this month's reality.

Switching to sales-based billing takes about nine minutes through a direct underwriter. Coverage then moves with the catalog, which is what the 77% under-coverage gap actually needs.

One Month of Actual Sales Beats Twelve Months of Guesswork

The contrarian take: annual premiums are not cheaper, they are just older. You are paying today's rate for last January's guess.

When a demand letter is already open, a current policy tied to actual sales responds. An annual policy priced on last year's forecast typically argues the exposure first.

If you bought your policy in a rush to clear a Seller Central request, open that Google Drive folder tonight. Find the declarations page. Check the sales figure your premium is anchored to.

Then pull last month's Shopify or Amazon payout report. If the two numbers do not match, your coverage does not match your business.

Get an instant quote at assureful.com. Nine minutes, last month's sales, 30 days' notice to cancel. Do it before the Tuesday email is yours.

Frequently Asked Questions

Does "annually" mean every 12 months?

Yes - "annually" generally means once per year (every 12 months). In health insurance, however, "annual" usually refers to the plan year rather than a rolling 12‑month interval: most deductibles reset on January 1 or the plan's first day, though some plans reset on dates like July 1 or October 1. Check your plan's Summary of Benefits and Coverage to see the exact reset date.

How do I get around dynamic pricing?

You can’t completely evade dynamic pricing, but you can minimize it by comparing sellers, using price‑tracking/alert tools, and buying in low‑demand windows or with refundable fares. Use Google Flights or Hopper for airfares, CamelCamelCamel/Keepa and Honey for Amazon/retail price history and coupons, and check prices in incognito or after clearing cookies - compare region rates with a VPN to avoid personalized surges. Also use refundable/price‑match policies to rebook if prices drop, and rely on loyalty programs or credit‑card travel protections to blunt surges.

What does Colonial Penn give you for $9.95 a month?

A guaranteed‑issue whole‑life “final expense” policy - a small, fixed death benefit with no medical exam and guaranteed acceptance (generally for ages 50-85) - offered by Colonial Penn for about $9.95/month. Coverage amounts vary by age and state but typically run in the low‑thousands (commonly $5,000-$25,000 depending on the plan and your age).

Is it better to have a $500 deductible or $1000?

Choose the $1000 deductible if you can comfortably pay the higher out‑of‑pocket cost because it will lower your premiums; choose the $500 deductible if you might struggle to cover $1,000 or you expect to file claims frequently. Insureon reports the average customer picks a $500 deductible, but insurers consistently advise selecting a deductible you can afford in a crisis.

If I switch from an annual policy to monthly billing midterm, will I get a prorated refund for the unused portion of my annual premium?

It depends: some insurers will prorate and refund the unused portion when you cancel midterm, while others treat the annual premium as fully or partially earned and won’t. If you switch to Assureful there’s no annual prepayment - Assureful bills month‑to‑month based on sales and allows cancellation with 30 days’ notice - but for any traditional annual policy you must check the policy’s cancellation/proration clause or ask your agent for the exact refund amount.

What documentation do insurers typically require each month to verify reported sales (e.g., Shopify/Etsy reports, bank statements, tax filings)?

Insurers typically require monthly supporting documents such as e‑commerce platform settlement reports (Shopify/Etsy daily/settlement detail), merchant‑processor statements (Stripe/PayPal), bank statements showing deposit activity and reconciliations, and POS or accounting exports (QuickBooks/Xero sales journals) that tie gross sales to deposits. They may also ask for sales tax returns (if filed monthly) or other tax filings, a month‑end sales reconciliation with variance explanations, and - for larger policies - a signed owner attestation or CPA review/audited financials and CSV/PDF exports for third‑party verification.

If my revenue spikes suddenly, am I automatically underinsured until the next monthly adjustment, and how fast can insurers raise coverage limits to match growth?

Not necessarily - with a usage‑based, month‑to‑month policy (e.g., billed to last month’s sales like Assureful) you generally aren’t automatically underinsured because limits adjust with reported sales; with traditional annual‑forecast policies you can be underinsured if revenue exceeds your forecast until an endorsement takes effect. Digital insurers can often raise limits instantly or by the next billing cycle (same day to 24-48 hours for instant‑quote products), while traditional carriers typically require an endorsement/underwriting review that can take several days to a few weeks (longer for large or complex increases). Promptly notifying your broker/insurer and providing updated sales documentation speeds the change.

For more on this topic, see our guide to instant insurance calculator.

This sits inside the broader topic of eCommerce business insurance for online sellers.

Related: Commercial Insurance Online Quote? What Happened When We Tested 5.

Related: Instant Business Insurance Quote Free? How Instant Quotes Work And.