Skipping proper eCommerce business insurance can destroy your business overnight: one in three small businesses faces an event that triggers an insurance claim, the average legal dispute costs $82,000, and platforms like Amazon require at least $1M general liability once you hit $10,000/month, one missing certificate of insurance (COI) can suspend accounts and freeze payouts. Many sellers mistakenly rely on homeowners or renters policies that exclude business inventory and liability; check platform and state mandates, secure appropriate commercial coverage, keep COIs current, and consider pay-as-you-sell solutions like Assureful to stay compliant and avoid catastrophic financial and legal exposure.

- Why Skipping Business Insurance Can Cost You Everything:...

- Three Costly Mistakes: Overlooking Requirements, Relying on Homeowners...

- Hidden Traps: Underinsuring Growth, Overlooking Cyber Threats, and...

- A Seller’s Checklist: Habits and Systems to Prevent...

- The Biggest Risk: Ignoring Insurance Requirements Leaves Your...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreWhy Skipping Business Insurance Can Cost You Everything: The Real Legal and Financial Impact

One in three small businesses faces an event that triggers an insurance claim, and the average legal dispute costs $82,000 out of pocket. A single lawsuit or account suspension can end an eCommerce business overnight.

eCommerce platforms are tightening insurance rules. Even a small compliance gap can freeze your payouts, suspend your account, or leave you personally responsible for injuries from your products. It’s not just profits at risk, your ability to keep selling can disappear without warning.

This guide breaks down the most common and expensive mistakes sellers make with online business insurance. Ignoring platform requirements, underestimating product liability, or choosing the wrong policy can mean lawsuits, lost sales, or being forced to shut down. You’ll get practical fixes: who needs coverage, how to meet marketplace mandates, and how solutions like Assureful’s pay-as-you-sell model keep you protected and compliant, no annual forecasts needed. For details on policy selection, see our complete insurance buyers’ guide for eCommerce sellers.

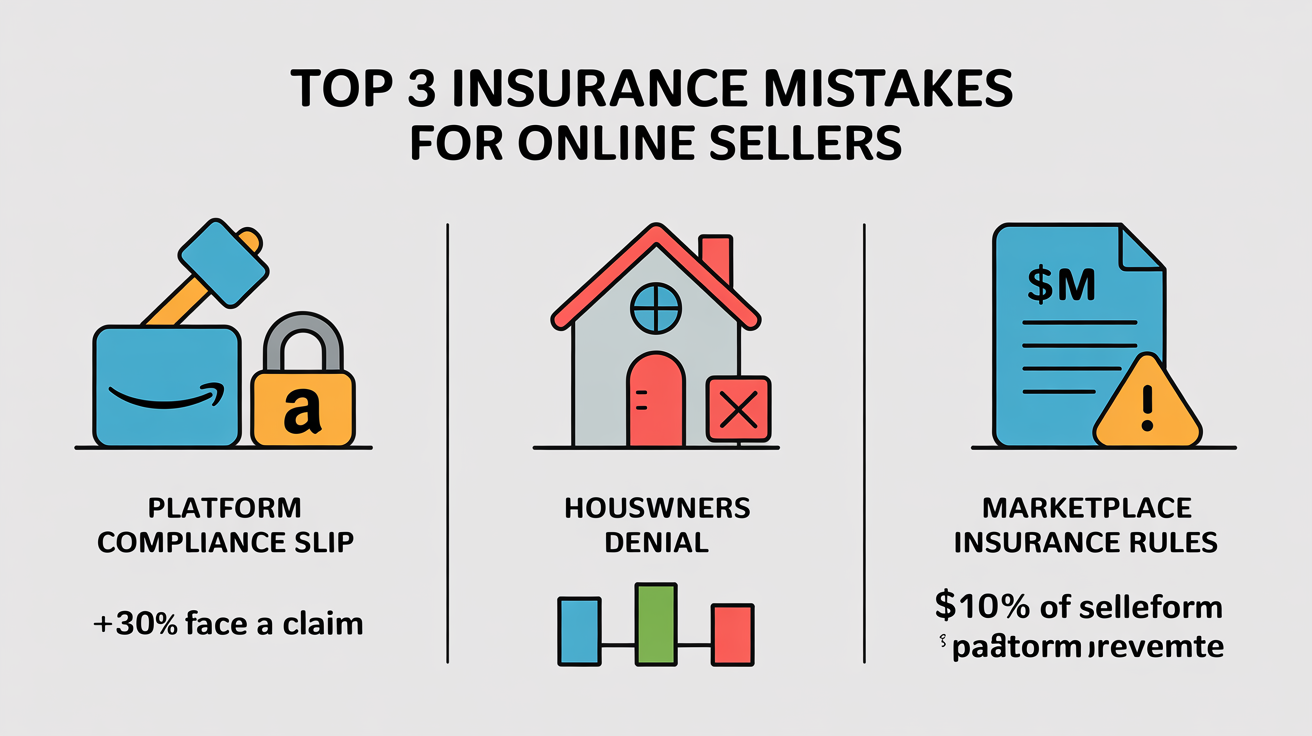

Three Costly Mistakes: Overlooking Requirements, Relying on Homeowners Insurance, and Ignoring Platform Rules

Miss a platform insurance requirement and your Amazon or eCommerce account can be suspended, sometimes for a single missing certificate. Even established sellers have seen payouts frozen over minor compliance gaps. An account suspension doesn’t just mean legal fees. It stops your sales pipeline, locks up inventory, and severs customer access immediately.

Ignoring State and Platform Insurance Mandates

Many sellers brush off business insurance, thinking mandates only target large brands. The reality: triggers like Amazon’s $10,000/month sales threshold often go unnoticed until a compliance alert lands in your inbox. Cross that line, and Amazon or Walmart require at least $1 million in general liability coverage. Miss the deadline, usually 30 days, and your store can be suspended. Now you’re exposed to lawsuits and locked out of the marketplace.

Check legal and platform insurance requirements for every market you serve. For Amazon, monitor your rolling monthly sales. Once you near $10,000/month for three straight months, secure general liability coverage and upload the certificate of insurance (COI) to Seller Central or your marketplace dashboard. Keep documentation updated for audits. For details on coverage triggers, see our hub on eCommerce insurance triggers.

Assuming Homeowners or Renters Insurance Covers Business Inventory or Risks

Plenty of new online sellers rely on personal homeowners or renters insurance, thinking it covers business property at home. Nearly all personal policies exclude business-related inventory and liability claims. If a fire destroys your stock or a product causes harm, your insurer will likely deny the claim, leaving you to cover losses and legal costs yourself.

- Check your current homeowners or renters policy for business exclusions.

- Get a business policy, like a pay-as-you-sell general liability policy, before listing inventory or shipping orders.

- Make sure your policy covers inventory (at home, in warehouses, or FBA) and product liability across all sales channels.

- Reassess coverage every year, or whenever you change suppliers, product lines, or fulfillment, to keep protection aligned with your risk.

Missing 'Additional Insured' and Policy Limit Requirements in Platform Terms

Marketplace rules often require the platform, such as “Amazon.com Services LLC”, to be named as an ‘additional insured’ on your policy, along with specific coverage limits and forms. Overlooking these details leads to frequent suspensions, especially after audits or customer claims. Common mistakes: missing endorsements, mismatched company names, or insufficient coverage on submitted certificates. Any of these can trigger a compliance hold.

Read your platform’s seller agreement closely. Work with an insurer who knows eCommerce, like Assureful or another specialist. Your policy must name the correct legal entity as additional insured, meet required coverage limits, and match your registered seller name and address. For Amazon, that means at least $1 million per occurrence, with Amazon.com Services LLC and affiliates listed. Upload your COI in the accepted format and keep documents current. For more on choosing coverage and showing proof, see our eCommerce insurance buyer’s guide.

Hidden Traps: Underinsuring Growth, Overlooking Cyber Threats, and Neglecting Product Liability

Growth brings hidden risk. Sellers who scale up often outpace their original insurance, leaving gaps that only show up after a claim. Skipping cyber protection is another common blind spot, cyberattacks target small online stores, not just big brands. Product liability also trips up established sellers, especially those offering new or imported goods.

Underinsuring After Sales Growth

Revenue climbs, but insurance limits stay stuck in the past. If coverage doesn't match your current sales or inventory, a single claim can drain profits fast. Some monthly pay-as-you-sell plans only update limits annually, so a sudden surge leaves you exposed. Miss one review and you might pay tens of thousands out of pocket.

Check your insurance quarterly. Compare declared limits to real sales, inventory levels, and any expansion into new products or fulfillment methods. With Assureful and similar providers, you can automate some updates, but you still need to confirm your coverage fits your business as it changes. For a step-by-step review, see our coverage review checklist for online sellers.

Skipping Cyber Liability for Small Stores

Cyber insurance isn't just for large retailers. Nearly half of cyberattacks hit small businesses, and even a minor breach can cost $1,500 or more to resolve. A ransomware attack, phishing incident, or hacked payment plugin can freeze operations, force legal action, or require you to notify every affected customer. General liability doesn't cover these losses.

- If you store customer data or process payments online, you need cyber liability coverage.

- Request a quote from your insurer or a specialist. Assureful can bundle cyber with your product policy.

- Look for coverage that includes business interruption, notification expenses, forensics, and extortion. Essentials, not extras.

- Review policy limits and deductibles each year, or after any security issue, to keep up with store growth.

Assuming Product Liability Only Applies to Manufacturers

It’s a common myth: only manufacturers face product lawsuits. U.S. courts regularly name every company in the chain, brand, importer, reseller, if a product causes harm. This risk grows with imports, dropshipping, or third-party goods. If your policy doesn’t list every category you sell, you’re exposed. One mishap can mean six-figure legal bills and settlements.

Check your certificate of insurance. Every product category and brand in your store should appear there. Adding electronics or a new brand? Notify your insurer and get updated paperwork. Full compliance keeps you protected, especially with policies like Assureful’s that update monthly. For details on product liability and practical protection steps, see our guide on product and general liability for sellers.

Regular insurance check-ins and clear communication with your provider prevent the most expensive mistakes. For more on building stress-free insurance for eCommerce, see our comprehensive eCommerce insurance buyer’s guide.

A Seller’s Checklist: Habits and Systems to Prevent Insurance Mistakes Before They Happen

Insurance mistakes rarely come from a single oversight. They build when processes slip, missed compliance checks, outdated documents, or last-minute scrambling. Sellers with habits like scheduled audits and centralized records avoid expensive surprises. Simple steps, like calendar reminders and clear process ownership, go further than frantic catch-up ever will.

- Quarterly compliance audit: Set a recurring reminder every three months. Review sales volume, updated SKUs, and check platform insurance requirements, such as Amazon’s $10,000 monthly sales threshold for liability proof.

- Change-driven reviews: Add a product, hire staff, or start selling on a new channel? Block time that same week to update insurance documents and confirm you’re still meeting platform rules.

- Centralized documentation: Store certificates, policy details, and key emails in one cloud-accessible folder. Assign a backup so files stay current when someone’s out.

- Proactive communication: Pick one team member to monitor insurer and platform notices. Get ahead of deadlines, don’t wait for an urgent request to find missing paperwork.

- Annual risk assessment: Once a year, discuss your business structure, products, and coverage with your insurer. Pay-as-you-sell coverage like Assureful makes this faster, but expanding product lines or changing fulfillment still needs a policy update.

These habits keep audits stress-free, records accessible, and your coverage in step with your business. Over time, manual checks shift to automated alerts, files stay organized through staff changes, and compliance headaches don’t slow you down. For more on building compliant, stress-free insurance for eCommerce, see our comprehensive buyer’s guide and this overview on when to insure your business. To see how these habits shape pricing and flexibility, review how to compare online insurance options and our benchmarks for lowering your coverage costs.

The Biggest Risk: Ignoring Insurance Requirements Leaves Your Store, and Livelihood, Exposed

Overlooking insurance or settling for the bare minimum leaves your business vulnerable. One product injury claim, cyberattack, or compliance misstep can erase years of hard work. The odds aren't distant. Even a minor data breach or customer injury can spiral, legal bills, lost revenue, and a damaged reputation that’s tough to repair.

Most of this risk is avoidable. Use a recurring checklist to track business changes and marketplace requirements. That way, you catch blind spots before they become emergencies. Stay current on coverage, especially product liability and cyber, so you’re ready if a customer, regulator, or platform asks for proof or files a claim. Frequent reviews help you spot new exposures as you add products or scale up, keeping protection aligned with how you actually operate.

Treat insurance as routine maintenance for your business. Want details on timing and coverage? See our overview on when to insure your business or compare options in the comprehensive buyer’s guide. Smart preparation keeps your margins, your brand, and your peace of mind intact.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

How much does general liability insurance typically cost for a new eCommerce seller doing under $100K, $1M in annual sales?

About $500, $1,000 per year is typical for e‑commerce sellers in the <$100K, $1M revenue band, with Coverdash/NerdWallet reporting a median around $850/year (≈$70/month). Policies can range roughly $250, $3,000 annually ($20, $250/month) depending on state, product risk, limits and claims history. Expect higher costs if you add inventory or a Business Owner’s Policy (medians ≈$2,000/yr) or buy separate cyber/product liability (commonly $500, $1,500/yr each).

What exactly is a Certificate of Insurance (COI) marketplaces like Amazon require, what information must it include, and how do I upload it correctly to avoid suspension?

A COI is a one-page proof document (commonly ACORD 25) that shows your insurer, policy number, named insured, policy effective/expiration dates, types of coverage (Commercial General Liability and product liability when required), and the coverage limits; it must also show the insurer’s contact and the limits per occurrence and aggregate. Amazon normally requires minimum limits of about $1,000,000 per occurrence and $2,000,000 aggregate for liability (verify the exact limits in the insurance request you received), and it requires that “Amazon Services LLC and its affiliates” be named as Additional Insured (with a corresponding Additional Insured endorsement) and that the policy be primary/non‑contributory and include a waiver of subrogation if requested. To avoid suspension, obtain a proper endorsement from your carrier, save the COI+endorsement as a PDF (ACORD 25 preferred) and upload it in Seller Central (Settings > Account Info > Insurance or Business Information > Insurance), ensure the legal business name on the COI matches your seller account, and renew/upload replacements before expiration or if Amazon rejects the document.

Can I buy short-term or seasonal liability coverage (for holiday spikes) instead of a full annual policy, and how do premiums and waiting periods work?

Yes, you can buy month-to-month/seasonal liability coverage instead of a full annual policy: pay-as-you-sell products bill monthly based on last month’s sales, provide instant quotes and immediate coverage, and can be cancelled with 30 days’ notice. Premiums are usage‑based (no annual sales forecast or large upfront premium) and, for example, Assureful reports average premiums about 42% lower than similar programs; traditional carriers typically require annual forecasts and upfront or financed premiums. Verify policy specifics (per‑occurrence vs aggregate limits, deductibles, exclusions and any carrier-specific waiting or retroactive periods) before you buy.

If I operate a dropshipping business and never physically handle products, do I still need product liability insurance?

Yes, you can still be held liable as a seller even if you never handle the products, and many platforms (for example, Amazon requires sellers with over $10,000/month in sales to carry coverage) expect it. Product liability (often provided as products-completed operations within a Commercial General Liability policy) helps pay legal fees, judgments, or settlements if a product causes injury or damage, though product‑recall costs are typically excluded and require separate coverage. Talk to an insurance agent to choose limits and whether you need a standalone policy or an endorsement.

I formed an LLC, if I don’t carry business insurance, can I still be held personally liable after a customer claim or lawsuit?

Yes, an LLC usually shields your personal assets, but you can still be held personally liable in many situations. Courts or claimants can reach you if you personally commit a tort (fraud, negligence, intentional wrongdoing), personally guarantee loans or contracts, commingle personal and business funds or ignore LLC formalities (allowing “piercing the corporate veil”), or where statutes impose individual liability (e.g., workers’ comp, employment taxes, or professional malpractice rules). Not carrying insurance won’t itself dissolve the LLC shield, but it leaves the LLC without funds to pay claims and makes personal exposure more likely if creditors pursue owners to satisfy judgments.

What immediate steps should I take after getting an account suspension notice or a customer claim to preserve insurance coverage and minimize business disruption?

Preserve evidence and contain exposure immediately: take screenshots, save emails/chats/transaction logs, export server and audit logs, and temporarily suspend or limit the affected account to prevent further loss. Notify your insurer and broker right away per your policy’s reporting procedure (record date, who you spoke to, and what was discussed) and complete claim forms accurately, many policies have strict timelines and a recent audit found well-documented claims settled faster and for higher amounts (≈85% better). Mitigate harm (refunds, fixes, or access controls), keep detailed remediation records ready to upload, and involve your broker or lawyer for serious claims to protect coverage and minimize disruption.

I sell internationally from outside the U.S., what special insurance requirements or policy endorsements do marketplaces and US customers typically expect?

You must carry commercial General Liability and Product Liability (and often a commercial umbrella) with typical marketplace minimums of $1,000,000 per occurrence / $1,000,000 aggregate (Amazon requires this for many sellers, e.g., Pro Merchants or those with >$10,000/month) and a deductible generally ≤ $10,000, with proof provided within 30 days. Policies must include U.S. territory coverage or an international policy extension for fulfillment in the U.S./Canada/EU/UK, and marketplaces typically demand a clean Certificate of Insurance (and commonly require the marketplace to be named Additional Insured, primary & non‑contributory, and a waiver of subrogation). If local insurers won’t issue a U.S.‑compliant COI (a common problem for sellers with >$3M revenue or high‑risk products), options are using Marsh/marketplace insurance programs, a U.S. insurer, or forming a U.S. entity (LLC + EIN) to obtain the required COI.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

Related: What Is Not Covered By The Commercial General Liability (CGL).

Related: How Much Is Commercial General Liability Insurance? What It Covers.

Sources

- ecom.insure

- vouch.us

- insurancecanopy.com

- 1800insurance.com

- flashpricer.com

- fitsmallbusiness.com

- simplybusiness.com

- mailchimp.com

- hotalinginsurance.com

- rangeme.com

- nextinsurance.com

- forbes.com

- landesblosch.com

- shopify.com

- moneygeek.com

- assureful.com

- payoneer.com

- taxjar.com

- policyape.com

- embroker.com

- thehartford.com

- moneygeek.com

- seo-pages-web.vercel.nerdwallet.com

- nerdwallet.com

- chastain-assoc.com

- regulaforensics.com

- dealhub.io