Many ecommerce sellers carry $1-2M liability policies (costing roughly $23, $42/month) that can be wiped out by a severe product claim, forcing inventory liquidation, sales suspension, or business closure when settlements and legal fees exceed limits. Use the checklist to calculate your largest plausible loss, audit platform and contract insurance requirements, gather current policy and loss-history documents, and decide whether higher limits (often $10-20M) are required to avoid catastrophic underinsurance.

- Missing a Step in High-Limit Liability: Why Oversight...

- Understanding High-Limit Public Liability Insurance: What You Need...

- Checklist: Deciding If $20 Million Public Liability Coverage...

- After the Checklist: Reviewing, Updating, and Documenting Your...

- The Real Value of a Thorough Liability Limit...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreMissing a Step in High-Limit Liability: Why Oversight Could Cost Your Ecommerce Business Millions

Miss a single step in liability coverage and your business could face devastating losses. A severe product claim can erase years of profit in one legal dispute. Most ecommerce sellers pay $23, $42 per month for $1-2 million in liability coverage, but settlements and legal fees often exceed those limits. When that happens, you could face forced inventory liquidation, sales suspension, or even permanent closure.

This checklist is built for ecommerce founders, Amazon and Shopify sellers, and online merchants with large contracts or strict platform requirements. Unsure if you need a $20 million public liability policy? Not clear what’s truly at risk if your cover falls short? Use these steps to assess exposure, understand compliance rules, and avoid mistakes that could jeopardize your business. Move from guesswork to a defensible, stress-free insurance decision.

Coverage requirements, risk triggers, compliance pitfalls, actionable next steps, the checklist breaks it down. If you’re questioning the real cost of missing a step, start by reviewing how much you should pay for business liability. For a side-by-side look at coverage options, see the complete liability policy comparison guide.

Understanding High-Limit Public Liability Insurance: What You Need to Know Before Deciding

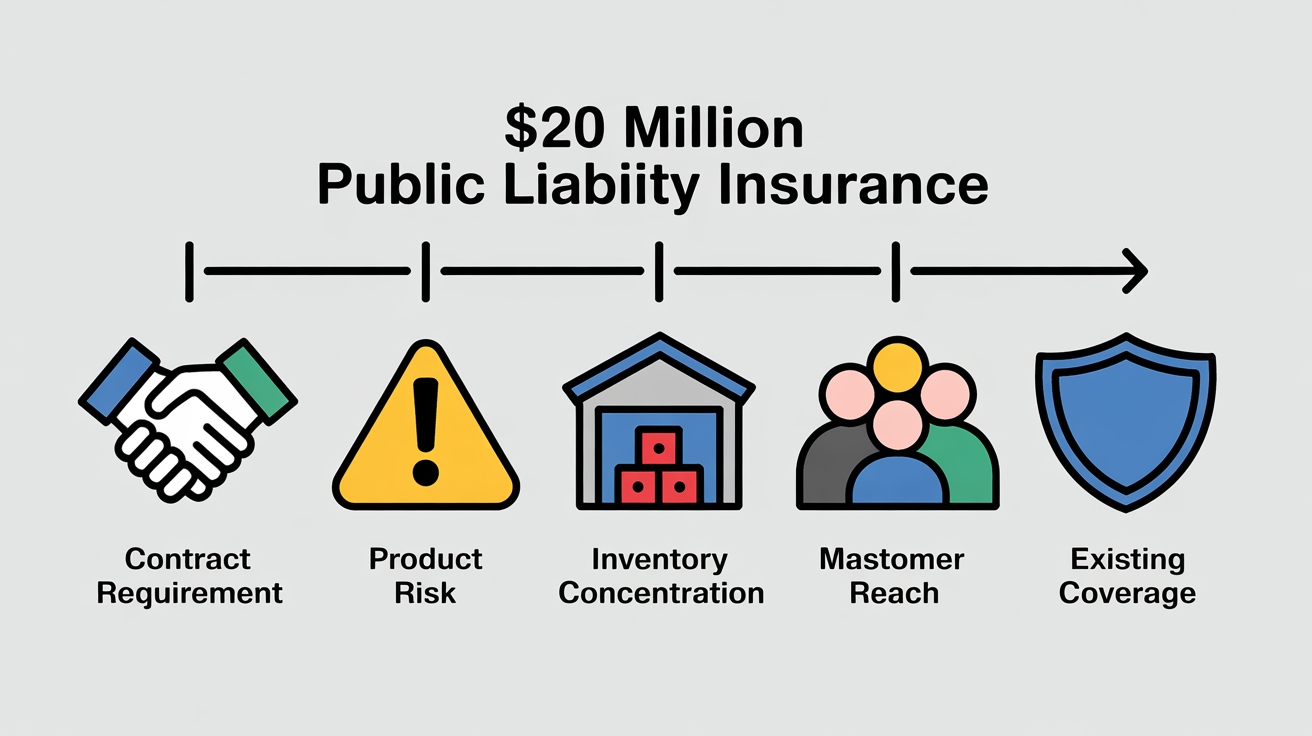

Standard liability policies for eCommerce usually max out at $1, $2 million. Some contracts, marketplace rules, or a single severe claim can require $10 million or $20 million in coverage. The right limit isn’t about your revenue. It’s about covering the largest plausible loss, product injuries, fire, mass recalls, or lawsuits with multiple claimants. If your supplier, big-box buyer, or Amazon contract specifies a high limit, being underinsured can void deals or suspend your account.

- Copies of all current insurance policies, general liability, umbrella/excess, product liability

- Major sales contracts and platform insurance requirements (Amazon, Walmart, wholesale customers)

- Loss history: recent claims, near misses, or incidents tied to your products

- Summaries of your product catalog, sales channels, and fulfillment model

Have your policy and contract PDFs ready. The checklist takes about 30-45 minutes if your documents are organized. For cost breakdowns by coverage level, see how much you should pay for business liability. For a direct comparison of high-limit insurance options, try our liability policy comparison guide.

Checklist: Deciding If $20 Million Public Liability Coverage Fits Your Online Business

Start with your single largest risk. Calculate the maximum payout if your product causes severe injury or major property damage, especially for children’s goods, ingestibles, or electronics. This potential loss can easily outstrip annual revenue and reach well over $10 million if mass claims, fire, or class actions are possible.

Marketplace and Contractual Triggers

- Audit all platform and wholesale insurance requirements. Review Amazon, Walmart, and major retail contracts for explicit liability limits. Many specify $1 million, but $10, $20 million is common for higher-risk or high-volume sellers. Miss the mark and you risk delisting or contract loss. Confirm unclear terms directly with the buyer’s risk team.

- Review every supplier and fulfillment partner agreement. Suppliers and logistics partners may require high limits to protect against shared liability. Focus on indemnity, hold-harmless, and insurance addenda in these contracts. Missing these terms can shift claim costs to you.

- Identify any regulatory insurance obligations by product category or geography. Certain products or jurisdictions, medical devices, children’s toys, mandate higher limits due to injury risk. Use published regulatory guides or consult local counsel to verify your obligations.

Quantifying Real-World Claim Severity

- Calculate your maximum foreseeable single-claim exposure. Picture your top-selling item causing multiple serious injuries or a fire. Recent catastrophic claims often settle above $5 million, with legal costs piling on. If your estimates top $1, $2 million, $20 million coverage deserves serious consideration.

- Map every product to a risk tier. Assign each SKU to a category: children’s goods, ingestibles, electronics, or general merchandise. Higher-risk categories face larger, more frequent claims. This mapping helps justify higher limits and informs your budget.

- Assess your aggregate risk, can multiple claims hit at once?. Some operations see isolated claims; others risk clusters (like a faulty batch causing dozens of injuries). Check your history and recall sector-wide incidents. If simultaneous claims are plausible, make sure aggregate limits match your total exposure.

Operational and Supply Chain Considerations

- Evaluate your fulfillment model for exposure amplification. If you self-fulfill or use third-party logistics, map how errors at a fulfillment center could multiply injuries or property losses. This operational risk often justifies higher liability limits.

- Scrutinize your overseas and domestic supplier controls. Weak or unverified quality controls, especially with imports, raise the odds of defects. If supplier vetting is minimal, higher coverage helps offset that vulnerability.

- Document your existing risk prevention and recall protocols. Batch testing, traceability, and recall readiness reduce the odds of a claim, but not its potential cost. Without strong controls, insurance is your only safety net.

- Benchmark your current limits and premium structure. Compare your coverage and rates to your sector’s typical range. Use tools like our liability cost hub and liability policy comparison guide to see what similar sellers carry. This keeps you from overpaying or underinsuring.

- Test the impact of pay-as-you-sell insurance models. Monthly-billed policies, such as Assureful’s, let you trial higher limits without upfront lock-in. Sellers with seasonal swings or scaling volume stay flexible.

Pressed for time? Prioritize (1) verifying all marketplace and contract requirements, (4) calculating your largest plausible claim, (5) mapping product risks, (7) reviewing fulfillment exposure, and (9) benchmarking current limits and costs. High-risk or fast-growing sellers should run these checks quarterly to avoid gaps that threaten your business. For a detailed breakdown of how product and general liability affect your store’s bottom line, see this detailed guide.

After the Checklist: Reviewing, Updating, and Documenting Your High-Limit Liability Strategy

Once you’ve completed your checklist, document your risk assessment and the reasons for your chosen liability limits. This protects you during audits, renewals, and future updates. Keep digital copies of coverage certificates, platform requirements, and key correspondence together in a secure, backed-up location.

- Write a summary of your risk decisions and coverage reasoning, highlight main exposures, selected limits, and why you chose them.

- Organize current and past compliance certificates and all policy documents in a digital folder for fast access.

- Set annual review dates, or check twice a year if you add sales channels or your revenue jumps 20% or more.

- Reach out to new or changing platforms and suppliers for updated coverage requirements at least twice a year.

- Monitor claims trends in your sector. If defect or recall rates climb, adjust your limits before problems hit.

Review your checklist every year, or anytime you launch new products, add sales channels, or see a major revenue shift. Expanding into new markets or changing your fulfillment model can affect your coverage needs. Use tools like our liability cost hub and the policy comparison guide for benchmarking. With pay-as-you-sell insurance models such as Assureful, you can adjust limits monthly, just be sure to document changes after major business events. For more ways to cut costs while staying fully compliant, see our guide on lowering your liability premiums without sacrificing coverage.

The Real Value of a Thorough Liability Limit Review: Confidence and Control

A careful liability limit review puts you in control. No more guessing, just clear, defensible choices. With up-to-date records and regular checks, you’ll avoid surprise gaps and stay fully compliant.

Verifying your policy limits against your business’s actual risks isn’t optional. Too many sellers get caught by exclusions or outdated limits when claims hit. Match your coverage to platform, vendor, and regulatory demands, your business keeps running, and you avoid costly interruptions.

Revisit this process every year, especially as you grow or your sales channels shift. Need benchmarks or want to compare? Use our liability cost hub and policy comparison guide for clarity and backup.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

What are the main differences between public liability and product liability insurance?

Public liability covers third‑party injury or property damage arising from your business activities or services (e.g., a customer slipping in your shop or a contractor leaving wires that cause a trip), while product liability covers third‑party injury or damage caused by goods you manufacture, supply or sell (including manufacturing or design defects and failure to warn). Public liability suits most businesses, especially those visiting client sites or doing manual work, whereas product liability is aimed at manufacturers, distributors and retailers and is often sold as an add‑on rather than standalone. Both cover defence costs and damages, are not usually legally required but are often contractually required by clients.

How can I estimate my maximum plausible loss for insurance purposes?

List the covered losses, then for each item calculate insurer payout = min(policy limit, verified loss − deductible − depreciation/subrogation); add any out‑of‑pocket for excluded or underinsured amounts to get your maximum plausible loss. Example: a $3,500 roof repair with a $1,000 deductible yields a $2,500 insurer payout; a $10,000 roof loss with a $1,500 deductible and $2,000 depreciation yields $6,500; also check separate sublimits (MedPay, rental) and ACV vs replacement‑cost rules.

Are there ways to lower premiums when buying high-limit liability insurance?

Yes, common levers are lowering aggregate limits (e.g., $2M → $1M), raising your deductible or self‑insured retention (e.g., $500 → $2,500), implementing safety/risk‑management programs, bundling policies (BOP), and requesting carrier discounts or paying the annual premium upfront. Raising a deductible typically trims premiums about 10-25% (one owner saved ~20% by moving from $500 to $2,500); lowering limits also reduces premiums but cuts coverage. Only use these tactics if your business can comfortably absorb the higher out‑of‑pocket exposure.

Can I meet a $20 million requirement by stacking a $1-2M primary policy with multiple umbrella/excess policies from the same or different insurers?

Yes, but only if you purchase properly sequenced excess/umbrella layers (a “tower”) that each attach above the $1-2M primary; you cannot reliably multiply coverage by buying several parallel umbrella policies unless each policy’s language and the insurers expressly allow stacking. Each excess must state its attachment point and whether it “follows form” or is non-contributory, and carriers commonly write excess layers (often up to $10M+ per policy) so you can reach $20M by combining layers from one or multiple insurers. Have your broker and coverage counsel review the “other insurance,” attachment, drop‑down and contribution clauses and obtain written confirmation from insurers that the tower will respond as intended.

Does a $20 million public liability policy cover product recall costs, or do I need a separate recall or crisis-management policy?

No. A $20 million public/product liability policy typically covers third‑party bodily injury, property damage and legal defense but almost always excludes product‑recall expenses (notification, retrieval/disposal, replacement, lost sales and crisis PR). You need a separate product‑recall policy or an endorsement, and often additional crisis‑management/contamination or business‑interruption cover, so confirm exact scope with your broker or carrier.

How long does it typically take to increase coverage to $20 million and what documentation do marketplaces or big buyers require for onboarding?

Typically 2-6 months: if carrier/reinsurance capacity already exists it can be done in 2-8 weeks for underwriting and endorsements, but sourcing new carriers/reinsurance, completing regulatory filings and product/document integration commonly pushes timelines to 3-6 months. Marketplaces and large buyers typically require an executed binder/COI, full policy forms and specimen endorsements, proof of carrier A‑rating and state licenses/NAIC numbers, audited financials (usually last 2-3 years), reinsurance agreements or capacity letters, loss runs and claims‑handling SLAs, producer/agency appointment paperwork, required state filings/certificates of compliance, plus technical onboarding items (SOC 2/ISO, API docs and test credentials) and W‑9/EIN.

Are legal defense fees paid in addition to the $20 million limit or do they reduce the available limit during a claim?

They typically reduce (erode) the $20 million limit unless the policy expressly states defense costs are payable in addition to limits (a "defense outside the limits" or similar endorsement). Check the declarations page and the "Defense Costs/Costs and Expenses" clause, if the policy doesn't contain an outside‑the‑limits provision you will be paying defense out of the $20M; obtain a written endorsement or broker confirmation if you need defense paid in addition.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to two-minute insurance quiz.

This sits inside the broader topic of eCommerce business insurance for online sellers.

Related: Do Deductibles Reset Every Year? A Renewal Checklist To Avoid Surprise Costs.

Related: Terrorism Risk Insurance Act.

Sources

- vouch.us

- esportsinsurance.com

- assureful.com

- aami.com.au

- marshcommercial.co.uk

- forbes.com

- thehartford.com

- policyape.com

- progressivecommercial.com

- morganinsurancebrokers.com.au

- thehartford.com

- embroker.com

- well-insurance.com

- insureon.com

- progressive.com

- piainsagency.com

- insureon.com

- esportsinsurance.com

- guardianlife.com

- aflac.com

- checklistguro.com

- wsj.com

- wsj.com

- pattersonlawfirm.com

- vpm-legal.com

- moneygeek.com

- insureon.com

- landesblosch.com

- progressivecommercial.com

- incubis.com

- pgicentralflorida.com

- allstate.com

- noblepagroup.com

- insureon.com

- geico.com

- constructioncoverage.com

- thehartford.com

- allstate.com

- chastain-assoc.com

- regulaforensics.com

- dealhub.io

- insurancecanopy.com

- insuredbetter.com

- thehartford.com

- travelers.com

- thimble.com

- allstate.com

- taxjar.com

- vargasinsurance.com

- insureon.com

- insureon.com

- geico.com

- insureon.com

- rginjurylaw.com

- thehartford.com

- perkinscoie.com

- nextinsurance.com

- forbes.com