Overlooking annual deductible resets on eCommerce insurance can force sellers to pay thousands out-of-pocket, product liability claims commonly run $5,000, $30,000+, and platform rules (e.g., Amazon requires deductibles under $10,000 and $1M per occurrence) plus pay‑as‑you‑sell billing models increase the risk of surprise costs or suspensions. The essential action is to calendar your renewal, verify policy type (occurrence vs. claims‑made), confirm deductible terms and COI, and follow the seven‑point checklist to protect margins, cash flow, and marketplace compliance.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreUnexpected Costs: Why Overlooking Deductible Resets Can Hurt eCommerce Sellers

Skipping a single item on your insurance renewal checklist exposes you to thousands in surprise costs. Miss a deductible reset, and a product liability claim or data breach can erase months of profit. Claims for product issues often range from $5,000 to $30,000 or more, money that comes straight out of your pocket if you miss this step.

This checklist is designed for Amazon, Shopify, and other online retailers who want predictable, stress-free insurance. Sellers scaling up, expanding product lines, or trying to avoid gaps that threaten marketplace eligibility need to know exactly how deductible resets impact margins and cash flow. Pay-as-you-sell models like Assureful require extra attention to monthly billing and policy resets, so you’re not caught off guard when a claim hits.

Expect direct, step-by-step reminders: review your renewal date, check deductible terms, and identify triggers that can reset your out-of-pocket costs. Review how product and general liability affect your online store's bottom line and use our comprehensive eCommerce insurance buyer’s guide alongside this checklist. For details on instant quotes and coverage pitfalls, see our guidance on getting from instant quotes to final coverage.

How Deductibles, Policy Types, and Renewal Cycles Work for Online Seller Insurance

Online seller insurance policies run on annual cycles. Your deductible resets at each renewal, so a new policy year means a new deductible, regardless of claims. If you miss this reset or choose the wrong policy type, you risk falling out of compliance or paying extra out-of-pocket. Occurrence-based policies cover incidents that happen while your policy is active, no matter when the claim comes in. Claims-made policies only respond if the claim is reported before your coverage expires or renews.

- Check your deductible amount and the reset date, usually at renewal.

- Keep your latest Certificate of Insurance (COI) and insurer contact on hand for uploads and compliance checks.

- Verify your policy type: occurrence or claims-made, especially for product, general, and cyber liability.

- Review platform requirements. Amazon requires a deductible under $10,000 and $1 million per occurrence, backed by A‑rated underwriters.

Set aside 20-30 minutes to review these details and gather what you need before starting the full checklist. For a deeper look at timing and documentation, see the comprehensive eCommerce insurance buyer’s guide and compare instant quote to final coverage steps.

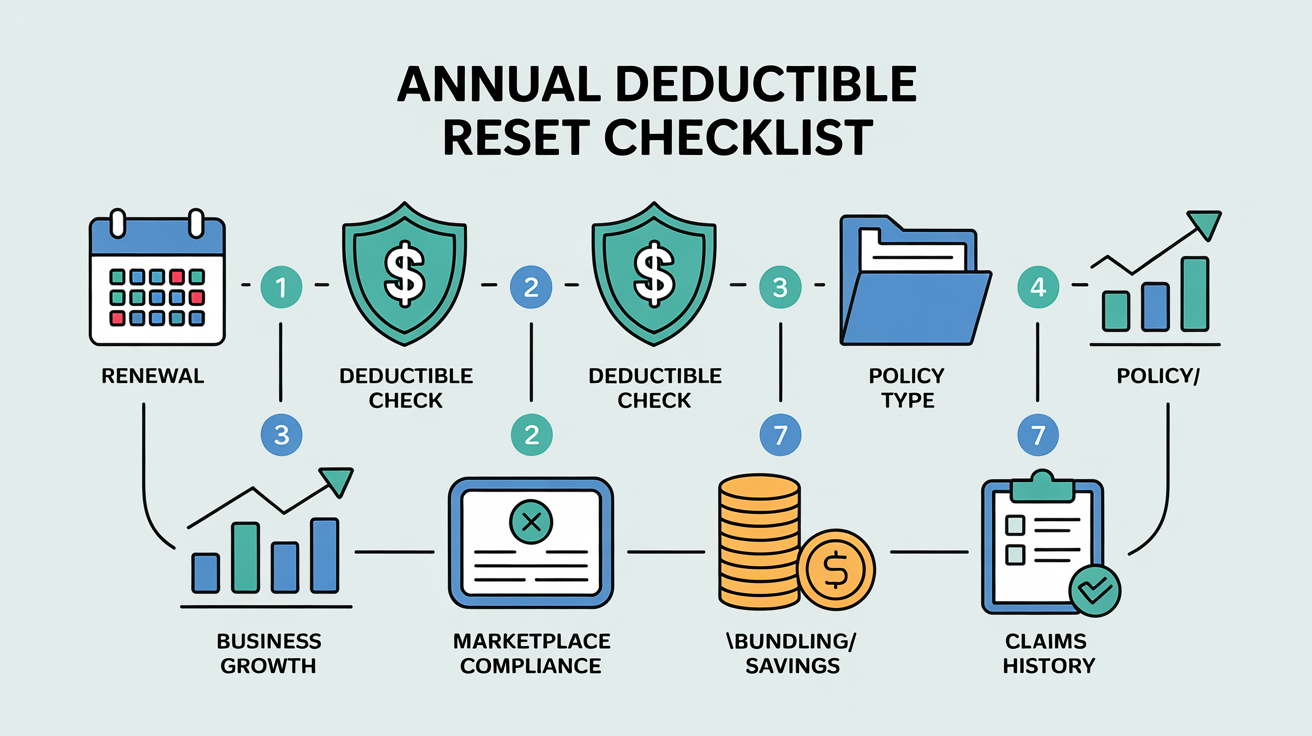

Annual Deductible Reset: 7-Point Renewal Checklist for eCommerce Sellers

Your insurance renewal date isn’t flexible, miss it and you risk Amazon suspension or denied claims. Mark your renewal on two calendars: 30 days before, and one week before expiry. Continuous coverage guards both compliance and your bottom line.

- Mark Your Policy Renewal Date, Twice. Enter your renewal date in your digital calendar and set a reminder on your phone. A missed renewal creates a coverage gap, violating marketplace rules and exposing you to claim denials. Set a 30-day alert to give yourself time to compare options and resolve paperwork or payment issues.

- Review Deductible Amounts and Reset Triggers. Deductibles usually reset annually, but pay-as-you-sell models can use rolling resets tied to your policy’s effective date. Read your renewal notice or ask your insurer for the exact reset date. Surprises here mean unexpected out-of-pocket costs when you file a claim.

- Verify Policy Type: Occurrence vs. Claims-Made. Occurrence policies cover incidents during the policy period, even if claims come later. Claims-made policies require both the incident and claim to happen within the coverage window. Selling products with long-tail risk, like electronics or supplements? Check your policy type and consider extended reporting if needed.

- Update Coverage for Business Growth. Hired staff? Added new channels? Crossed $10,000 in monthly sales? Each milestone changes your risk. Notify your insurer as soon as you expand. Waiting until renewal can void claims or leave you underinsured, especially with new categories or international markets.

- Confirm Certificate of Insurance Compliance. Amazon and similar marketplaces require a deductible no higher than $10,000, $1 million per occurrence, and their name as additional insured. Double-check your Certificate of Insurance lists all required entities and matches current limits. Upload the updated certificate to avoid seller suspensions.

- Evaluate Bundling and Payment Savings. Bundling (general liability, product liability, cyber) saves 15-25% compared to buying separately. Annual payments cut 4-10% in monthly fees and may trigger extra discounts. Compare bundled Business Owner’s Policies (BOPs) and annual billing, see if the numbers work for your business.

- Organize Claims and Quality Control History. Insurers review your loss and quality control records after any claim or near-miss. Keep detailed records of claims, recalls, and product testing. Clean history qualifies you for preferred rates. Gaps or poor documentation can drive premiums up by 25-100%.

Pressed for time? Focus on your renewal date, deductible reset, and marketplace compliance. These prevent the biggest disruptions. Want a deeper process? See our comprehensive eCommerce insurance buyer’s guide and compare the full instant quote to coverage process.

Assureful’s pay-as-you-sell model tracks business changes and bills monthly, so you don’t overpay or miss key updates. Thinking about switching or bundling? Review current pricing benchmarks and ways to lower coverage costs before committing to another annual policy.

Adding vehicles or new product lines? See how commercial auto insurance for eCommerce sellers and product and general liability affect your store’s bottom line.

What To Do After Your Policy Renews: Proactive Steps for Continuous Protection

After renewal, set a mid-term business review on your calendar. This review keeps your coverage aligned with real risks, essential if you’re launching new products, expanding overseas, or growing fast. Proactive checks help you avoid underinsurance and stay compliant with Amazon, Shopify, Walmart, and other marketplaces.

- Set digital reminders for a 6‑month policy review and for key milestones, like new hires or product launches.

- Check marketplace terms every quarter for updated insurance requirements or new certificate templates.

- Store updated digital copies of all insurance certificates in a secure, shared folder for quick compliance checks and faster claims.

- Notify your insurer right away if you plan to enter new sales channels or add higher-risk products. That prevents gaps in coverage.

- Keep a running log of claims, recalls, and customer incidents to speed up future processing and support eligibility for preferred rates at renewal.

Review this checklist at least twice a year, once after renewal, and again at six months or after major business changes. Sellers adding vehicles or expanding product lines should review commercial auto coverage options and use the complete eCommerce insurance buyer’s guide for step-by-step details. For a full walkthrough, the instant quote to coverage process breaks down when mid-term reviews protect your eligibility and your bottom line.

Stay Ahead Of Surprises: The Value of a Renewal Routine

An annual insurance renewal checklist keeps costs steady and coverage on track. This habit helps you avoid unexpected deductible resets, compliance issues, or overlooked claims that can disrupt business. Organized renewals mean less stress and fewer risks as your business grows.

The top priority: make sure your policy matches your current business. Skip an update, like new products, new sales channels, or higher volumes, and you could face denied claims or gaps in coverage. Reviewing your policy at renewal keeps limits, deductibles, and compliance documents up to date.

Build this routine and you’ll create a stable base for stress-free selling. For step-by-step support, check the complete eCommerce insurance buyer’s guide or walk through the instant quote to coverage process for practical help at every stage.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

If I cancel my policy and switch insurers mid-year, does my deductible reset immediately, carry over, or get prorated?

Your deductible does not carry over, the new policy’s deductible applies starting on its effective date and is not prorated. If a loss occurred while the old policy was in force, the old policy’s deductible applies to that claim (and the new insurer won’t cover that pre-existing occurrence). Rare exceptions: same-carrier replacements or specific contract language sometimes credit prior deductible payments, so confirm with both insurers.

Are deductibles charged per claim or is there an annual aggregate deductible for product liability and cyber/security claims?

They are generally charged per claim (per‑occurrence) for both product liability and cyber/security policies. The policy still has an overall aggregate limit (e.g., $1M per occurrence / $2M aggregate), and while less common some large or negotiated programs use an annual aggregate retention or self‑insured retention, always confirm the declarations and retention wording in your specific policy.

If I file multiple claims in the same policy year, do I have to pay the deductible for each claim or only once?

Usually you pay the deductible for each separate claim/occurrence, most auto, homeowners, property and liability deductibles are applied per claim. Exceptions include many health plans (which use an annual deductible) and some commercial policies that use an annual aggregate deductible or retention, so check your declarations page or ask your agent to confirm the exact wording.

Do deductibles apply to defense and legal costs, or only to settlements and judgments for product liability/cyber incidents?

It depends, deductibles/retentions can apply to defense/legal costs or only to settlements and judgments depending on the specific policy language. Some liability forms pay defense "outside the limits" (so defense costs aren’t subject to the deductible and don’t erode limits), while others include defense within the limit or impose a separate deductible or sublimit for defense; cyber policies commonly have separate retentions for breach‑response (first‑party) and third‑party liability. Check the declarations, deductible/retention definitions and endorsements (there is no industry‑standard cyber form) or ask your broker/insurer to confirm.

Can a supplier, manufacturer, or another party reimburse my deductible (or does subrogation/contractual indemnity typically cover that)?

Yes, a supplier or manufacturer can reimburse your deductible either voluntarily (as part of a settlement) or because your contract requires it; insurers also commonly recover deductible amounts from responsible third parties through subrogation. To maximize recovery, include an express indemnity clause that obligates the supplier to pay your deductible and to cooperate/assign subrogation rights; absent that, whether recovered funds are paid to you or retained by your insurer depends on your policy language and state law. Review your insurance policy and contract language and get legal advice to draft enforceable deductible-reimbursement and subrogation provisions.

Will choosing a high deductible affect marketplace compliance or vendor requirements (for example, Amazon or Walmart insurance limits), and how should I pick a deductible to stay eligible?

No, choosing a high deductible by itself won’t make you ineligible for the ACA Marketplace or for premium tax credits, because Marketplace eligibility is determined by household income, household size, and access to affordable employer coverage, and Marketplace plans must meet federal essential‑benefit and out‑of‑pocket rules. The practical limits to watch are IRS rules for HSA‑qualified HDHPs (they must meet IRS minimum deductible and maximum out‑of‑pocket thresholds) and any employer/contractor/vendor contracts that may specify required plan features or separate commercial insurance (those vendor requirements typically govern liability policies, not your personal health deductible). Pick a deductible you can afford to pay in a worst‑case year, weigh premium savings versus expected out‑of‑pocket use, and choose an HSA‑qualified HDHP only if you want HSA tax benefits; always check any specific vendor or contract language for additional requirements.

Are insurance deductibles tax-deductible as business expenses, and how should I record deductible payments in my accounting records?

Yes, insurance deductibles your business pays as part of a covered loss are generally tax-deductible as ordinary business expenses (premiums are deductible when paid or accrued). Record deductible payments by debiting an appropriate expense account (e.g., "Insurance deductible expense," "Loss on claim," or "Repairs & maintenance") and crediting Cash; if you expect an insurer recovery, record the gross loss and establish an "Insurance receivable" for the recoverable portion so the net expense on the books equals the deductible.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to two-minute insurance quiz.

Related: How Much Is $20 Million Public Liability Insurance? A Checklist.

Related: Terrorism Risk Insurance Act.

Sources

- fitsmallbusiness.com

- 1800insurance.com

- moneygeek.com

- nextinsurance.com

- shopify.com

- policyape.com

- vouch.us

- landesblosch.com

- assureful.com

- techinsurance.com

- insureon.com

- nerdwallet.com

- seo-pages-web.vercel.nerdwallet.com

- nerdwallet.com

- hotalinginsurance.com

- moneygeek.com

- checklistguro.com

- insureon.com

- payoneer.com

- forbes.com

- flashpricer.com

- ecom.insure

- co-opinsurance.com

- rangeme.com

- kelleyinsure.com

- veritasrm.com

- baldwin.com

- coalitioninc.com

- bankrate.com

- amfam.com

- security.org

- progressive.com

- sharepointcu.com

- progressive.com

- usnews.com

- dairylandinsurance.com

- progressivecommercial.com

- valuepenguin.com

- statefarm.com

- geico.com

- geico.com

- allstate.com

- quora.com

- insureonthespot.com

- insureonthespot.com

- kin.com

- forbes.com

- cadence.care

- progressivecommercial.com

- bankrate.com

- statefarm.com

- constructioncoverage.com

- nextinsurance.com

- marketwatch.com

- moneygeek.com

- progressive.com

- cnbc.com

- wawanesa.com

- geico.com