Your homeowner's insurance won't cover business claims, period. An LLC helps, but it's not enough without proper commercial coverage. You need four things working together: the right business structure, any required licenses, actual insurance policies, and compliance with your sales platform's rules. Miss any one of these, and your personal savings are at risk.

Why Your Business Structure and Insurance Must Work Together

Your homeowner's or renter's insurance explicitly excludes business-related claims. If a customer sues your eCommerce business, your homeowner's policy will deny the claim outright. You'll be personally liable for the full amount.

Many sellers think an LLC alone solves this problem. It doesn't. An LLC creates legal separation between you and your business, but that barrier only holds if you also carry commercial insurance. Structure and coverage work as a pair, neither is sufficient alone.

A lawsuit over a defective product, a customer injury claim, or property damage can easily cost $15,000 to $50,000 in legal fees and settlements. Without proper coverage, that money comes directly from your personal savings, investments, or home equity.

This guide walks you through how business structure and insurance connect. You'll learn why your homeowner's policy fails to protect business operations, how different business entities affect your personal liability, and what commercial coverage you actually need.

The Four Critical Layers of Protection: Structure, Licenses, Policies, and Platforms

Your coverage depends on four interconnected layers. Each one affects the others, and gaps in any single layer leave you exposed.

Layer One: Your Business Entity Structure

Whether you operate as a sole proprietor, LLC, or partnership fundamentally changes your personal liability exposure.

As a sole proprietor, you and your business are legally the same. A lawsuit against your business is a lawsuit against you personally. Your customers' lawyers can pursue your personal savings, home, and investments to satisfy a judgment.

An LLC creates legal separation between you and your business. If a customer sues and wins, the judgment typically stops at your business assets. Your personal finances remain protected. The cost is modest, $50 to $500 to form, plus annual renewal fees. For any seller generating consistent revenue, this protection pays for itself.

Layer Two: Business Licenses and Platform Compliance

Your sales platform may require specific insurance before you can legally operate.

Amazon requires sellers with gross monthly sales exceeding $10,000 to carry commercial general liability insurance. The minimum is $1 million per occurrence and in aggregate, with product liability coverage included. The policy must have a deductible not exceeding $10,000, be issued by an A-rated underwriter, and name Amazon.com Services LLC as an additional insured.

Etsy doesn't mandate insurance, but many sellers choose to carry it anyway. Understanding what your platform requires forces you to make a coverage decision whether you planned to or not.

Layer Three: Core Policy Types

eCommerce insurance isn't a single policy, it's a combination of coverages.

General liability covers bodily injury and property damage claims. A customer trips in your warehouse, or your delivery vehicle damages someone's fence, general liability covers it.

Product liability covers injuries or damage caused by products you sell. This includes imported goods and dropshipped items. You're legally liable for product defects in the distribution chain even if you didn't manufacture the product.

Median general liability premiums run approximately $850 per year. Basic coverage packages typically range from $1,500 to $2,000 annually depending on sales volume and product category.

Layer Four: Platform-Specific Requirements

Your sales channel dictates coverage requirements regardless of your business size. If you sell on Amazon and cross the $10,000 monthly threshold, you must obtain coverage within 30 days or face account suspension.

You must upload a Certificate of Insurance (COI) to Seller Central, and your insured company name must match your legal entity name, bank account name, and Amazon account name exactly. Discrepancies trigger account holds or suspension.

If you sell on multiple platforms, you may need to meet multiple sets of requirements. A single policy can cover sales across all channels, but confirm your policy explicitly covers the platforms you operate on.

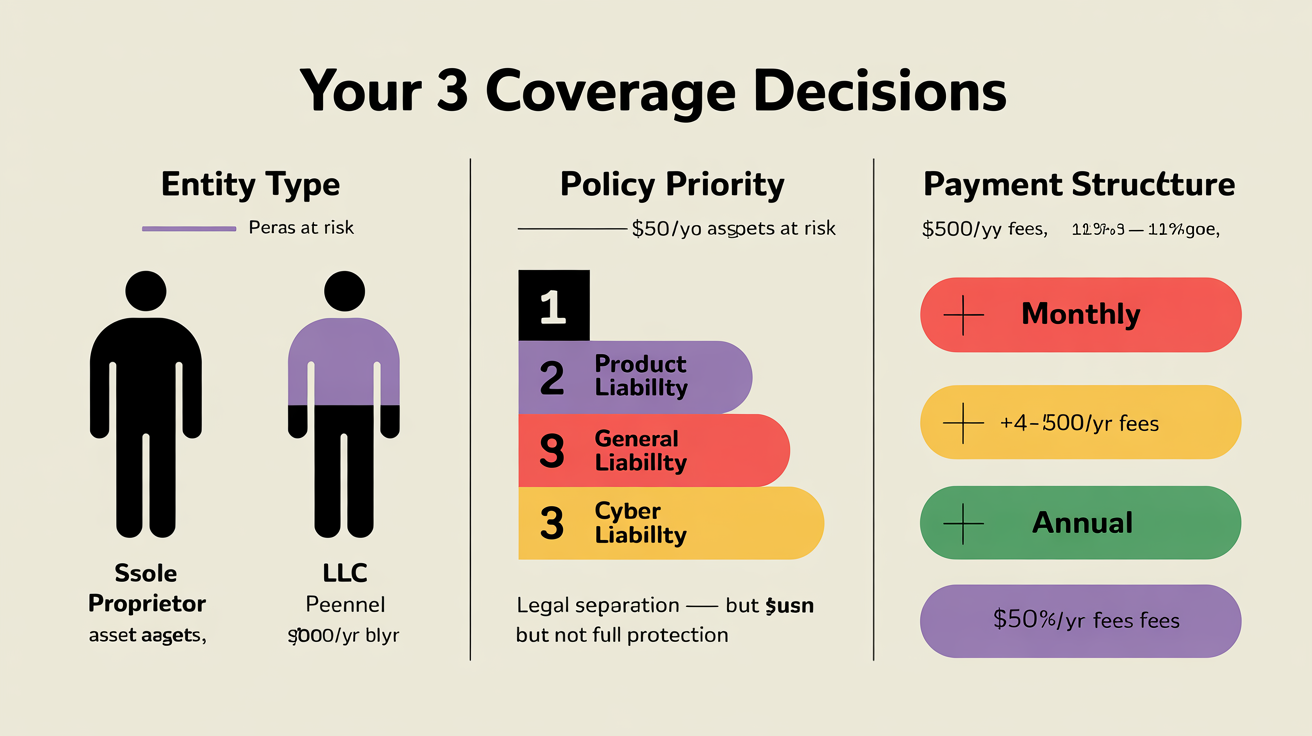

Three Coverage Decisions You'll Face, And the Tradeoffs at Each Step

You face three distinct coverage decisions. Each involves a tradeoff between cost, risk exposure, and operational complexity.

Decision One: Insure Yourself Personally or Form an LLC First

As a sole proprietor, every product liability claim reaches your personal assets. Customers' lawyers will pursue both your business assets and your personal wealth.

An LLC creates legal separation. If a customer sues and wins, the judgment typically stops at your business assets. This separation also signals credibility to suppliers and customers.

The tradeoff is straightforward. An LLC costs $50 to $500 to form, plus modest annual renewal fees. For any seller generating consistent revenue or handling customer data, the protection justifies the cost.

Decision Two: Which Policies to Prioritize First

Product liability and cyber liability are non-negotiable from day one.

You're legally responsible for product defects even when sourcing from third-party manufacturers. In 2021 alone, emergency rooms treated 11.1 million consumers for product-related injuries. Online sellers were named in many of those claims.

Cyber liability protects you when your store gets breached. Nearly 43% of small businesses experience a breach. Both policies activate within 24 hours and cost approximately $500 to $1,500 annually for basic coverage combined.

Once your sales reach $10,000 monthly, Amazon and other major marketplaces require $1 million in general liability coverage. Plan for this threshold now rather than scrambling for coverage after you hit it.

Starting with the essential trio, product, cyber, and general liability, positions you to scale without coverage gaps.

Decision Three: How to Structure Payment and Bundling

Bundling coverage types saves 15% to 25% compared to purchasing policies separately.

A Business Owner's Policy bundles general liability and commercial property insurance at a discount. Adding cyber and product liability compounds savings further. Shopping for bundled quotes takes the same time as shopping separately, so the savings are essentially free.

Paying annually instead of monthly eliminates 4% to 10% in processing fees and often qualifies you for an additional 5% to 9% discount. If you're paying $100 monthly ($1,200 yearly), switching to annual payment could save $140 to $190 per year.

The tradeoff is cash flow. You pay upfront rather than spreading payments across twelve months. For most sellers, annual payment is the right move.

Five Mistakes That Leave You Exposed

The costliest mistake most eCommerce sellers make is assuming homeowner's or renter's insurance covers business activity. It doesn't. These policies explicitly exclude business-related claims.

Structural mistakes compound cost mistakes. When you operate without proper coverage alignment or misunderstand what your policies cover, you expose your personal assets to lawsuits, account suspensions, and uninsured losses.

Mistake One: Assuming Homeowner's Insurance Covers Your Online Business

Homeowner's and renter's insurance policies have explicit business exclusions. If a customer is injured by your product or sues you for property damage related to your business, your homeowner's policy will deny the claim.

You are personally responsible for 100% of the judgment, legal fees, and settlements.

This applies even if your inventory is stored in your home, your office is in a spare bedroom, or you pack orders at your kitchen table. The moment you conduct business activity, homeowner's insurance no longer covers you.

Mistake Two: Believing an LLC Protects You Without Commercial Coverage

An LLC creates legal separation between your personal assets and your business assets. It reduces personal liability exposure, but it's not a substitute for commercial insurance.

If a customer sues your LLC and wins a judgment larger than your business assets, you may still face personal liability depending on your state's laws and the nature of the claim.

Additionally, many platforms including Amazon require commercial general liability insurance regardless of your business structure. An LLC alone won't satisfy those requirements and won't protect you from account suspension. You need both the structural protection of an LLC and the coverage protection of a commercial policy.

Mistake Three: Buying Coverage After Your First Sale

Insurance policies cover claims that occur during the policy period. If a customer is injured by your product on day one and you purchase coverage on day two, that injury is not covered.

The exposure began the moment your first listing went live, not when you uploaded your Certificate of Insurance to Amazon.

Many sellers delay purchasing coverage until they hit the $10,000 monthly sales threshold that triggers Amazon's insurance requirement. By then, you've already operated exposed for weeks or months. Buy coverage before you launch.

Mistake Four: Mismatching Your Insured Name With Your Platform Account Name

Amazon suspends seller accounts when the legal name on your Certificate of Insurance doesn't match your Seller Central account, your EIN, your bank account, or your business address.

These four elements must align exactly across all documents you submit to Amazon.

A mismatch triggers a compliance flag in Amazon's system. Even if you provide a valid Certificate of Insurance, Amazon will suspend your account until you resolve the discrepancy. Account reactivation can take 24 to 48 hours or longer, during which you earn zero revenue. Verify all legal names and addresses are consistent before you upload your COI to Seller Central.

Mistake Five: Operating Without Coverage on Platforms That Mandate It

Amazon requires all sellers with monthly sales exceeding $10,000 to maintain $1 million in general liability coverage with product liability included. This requirement has been in place for years, but enforcement became strict as of September 1, 2021.

Sellers who don't comply receive a notice and are given 30 to 60 days to upload a valid Certificate of Insurance. Failure to comply results in account suspension.

While suspended, you cannot list products, fulfill orders, or access your inventory. You lose all income until compliance is restored. Even after you upload a valid COI, reactivation isn't instantaneous and can take days. The cost of non-compliance far exceeds the monthly premium for coverage.

If you sell on Amazon and exceed $10,000 in monthly sales, coverage is not optional.

Where to Start Right Now

Your first decision is business structure. Whether you operate as a sole proprietor, LLC, or corporation determines how insurance protects your personal assets and which policies you can buy.

Start by comparing the liability exposure and tax implications of each structure. Understand which makes sense for your sales volume and risk profile.

If you've already chosen a structure but aren't sure what coverage you need, read about how product and general liability affect your bottom line. That breakdown explains what each policy covers, which gaps matter most for your business model, and how to size limits based on real downside instead of guesswork.

If you want immediate action, use the ultimate eCommerce insurance checklist for new store owners. Walk through each decision step by step.

If cost is your primary concern, general liability premiums average $42 per month across the industry. Your actual cost depends on revenue, product risk, and whether you carry imported goods. Sellers on Amazon or Shopify face mandatory coverage requirements tied to monthly sales thresholds, so platform-specific rules apply regardless of cost.

Once you've mapped your structure and know what you need, get your instant quote and move from protected to selling within hours.

Frequently Asked Questions

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to what business insurance an LLC needs.

Sources

- thecoylegroup.com

- thehartford.com

- godaddy.com

- geico.com

- mailchimp.com

- progressivecommercial.com

- firstbase.io

- strategylaw.com

- moneygeek.com

Next best step

Match the article to the buying page.

If you are comparing coverage or preparing for a quote, start with the page that matches where you sell and what you sell.

eCommerce insuranceFull buyer's guide for online sellers.Amazon seller insuranceProof of insurance and COI guidance for third-party sellers.Shopify insuranceCoverage planning for Shopify and DTC brands.Product liability by stateState-specific product liability context and requirements.Compare insurersSee how Assureful compares with traditional carriers.

Related buying paths

Find the category page behind the risk.

Amazon categories

Product liability guides for Amazon sellers

Shopify categories

Product liability guides for Shopify brands

Best-fit comparisons