Assureful offers pay-as-you-sell, monthly-billed ecommerce insurance with instant quotes/certificates, A‑rated underwriters, coverage for imported/rebranded products and cyber liability, and averages 42% lower premiums than comparable carriers while targeting Amazon, Shopify, and multichannel sellers. Most important: it replaces risky annual forecasts and policy exclusions with on-demand, compliant product and cyber liability protection that scales with sales to prevent claims, fines, or marketplace suspensions that can shut down a new store.

- Why Assureful Is the Top Insurance Pick for...

- The Insurance Features That Matter Most for Ecommerce...

- Comparing Ecommerce Insurance: Key Features, Exclusions, and Monthly...

- Best Ecommerce Insurance Providers for 2026: Honest Reviews...

- Common Ecommerce Insurance Mistakes: How New Sellers Get...

- Which Ecommerce Insurance Should You Pick? Our Direct...

- Start With Stress-Free, Adaptive Insurance, And Scale As Your...

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreWhy Assureful Is the Top Insurance Pick for New Ecommerce Stores

Assureful is the top choice for new eCommerce stores. You get pay-as-you-sell insurance, predictable monthly costs, and instant, compliant coverage, no annual sales forecasts or large upfront premiums. Designed for Amazon, Shopify, and multi-channel sellers, the program averages 42% lower premiums than similar A-rated carriers.

Insurance for online sellers isn’t just about price. You need stress-free insurance that keeps you compliant from day one, adjusts with your sales volume, and doesn’t penalize you for growth or quiet periods. The wrong policy can leave you exposed to claims that disrupt or even shut down your business. Missed compliance can block your store from key platforms.

This guide details what makes Assureful different, where traditional policies fall short, and how liability coverage shapes your store’s financial stability. You’ll find a clear checklist for when public liability insurance is required, a comparison of leading providers, and practical advice for protecting your brand as it grows.

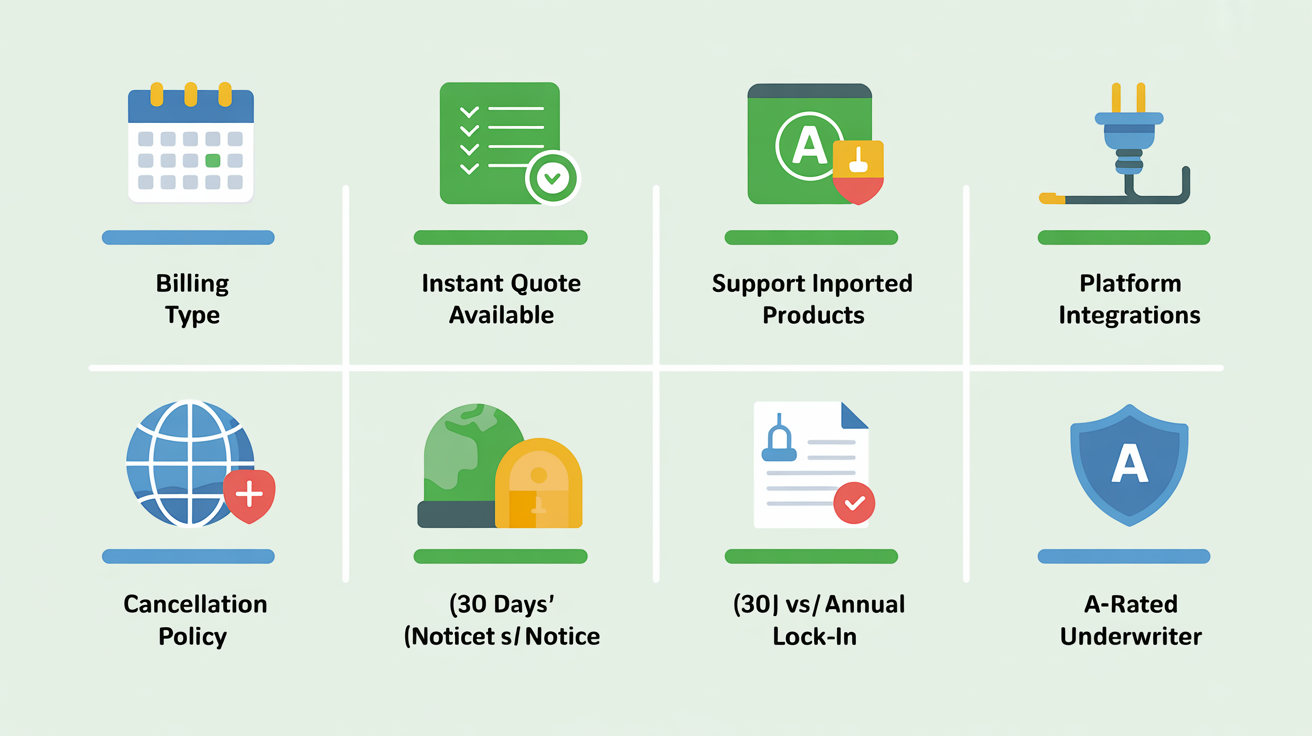

The Insurance Features That Matter Most for Ecommerce Startups

Start with product liability coverage. Nothing protects your business more, if a product injures someone or causes damage, you’re legally on the hook, no matter who made it. This is non-negotiable for marketplace compliance and financial survival. Ignore insurance extras that don’t address these core risks.

Product Liability Coverage for All Products, Including Imports

If you sell physical goods, manufactured, private label, or imported, you face product liability. Defects, misleading labels, or design issues can trigger legal claims. You’re part of the distribution chain, so you’ll be named. Imported and rebranded items draw extra scrutiny, especially from platforms like Amazon. Don’t settle for policies that exclude overseas or relabeled products. Set limits based on injury potential in your category, not just revenue. Categories like children’s items, ingestibles, and electronics demand higher limits early.

Cyber Liability and Customer Data Protection

Cyber liability isn’t optional. Forty-three percent of cyberattacks hit small businesses, and a breach can cost over $150,000. Store customer data or process payments? You’re exposed. Look for policies covering both your own costs (system restoration, breach notifications) and third-party liabilities (customer lawsuits, regulatory fines). Choose insurers with proven eCommerce claims experience, you’ll want expertise when an incident hits.

Instant Quotes, Monthly Billing, and A-Rated Underwriters

Annual premium forecasts and big upfront payments? That model doesn’t fit eCommerce. Prioritize providers offering:

- Instant quotes and coverage certificates, often within 24 hours

- Monthly billing tied to last month’s sales (“pay-as-you-sell”)

- Policies underwritten by A-rated carriers

- Coverage for imported products and global fulfillment

- Straightforward claims processes and platform integration

- Cancel anytime with 30 days’ notice, no penalties

Assureful delivers on these points: instant onboarding, no annual forecasts, multi-channel support, and clear cancellation. Prefer annual payments for up-front discounts or want in-person broker support? Their digital-only experience may not suit you.

Flexible Coverage That Scales With Your Growth

Insurance should match your sales, no penalties for slowdowns, no restrictions during spikes. Policies that auto-adjust when you pass milestones like Amazon’s $10,000/month sales rule save compliance headaches. Bundling general liability, cyber, and product coverage usually costs 15-25% less than buying separately. See our pricing benchmarks for real-world numbers and strategies to cut costs.

Skip retail-focused policies, high upfront premiums, or plans that ignore imported goods. Don’t get distracted by insurance “extras” that don’t reduce product, cyber, or compliance risk. For most eCommerce startups, a policy that adapts to your sales and cancels easily will outperform legacy coverage every time. Compare instant quote flows and certificate timelines in our breakdown if you want to see how fast you can get covered.

Comparing Ecommerce Insurance: Key Features, Exclusions, and Monthly Costs

Monthly billing tied to your actual sales transforms insurance into a predictable, stress-free safety net. Selling online with annual premiums often means overpaying and dealing with headaches when revenue fluctuates. Pay-as-you-sell models with instant quotes and clear documentation reduce cost and hassle while keeping you fully compliant.

| Provider | Pricing Model | Feature Highlights | Best For | Rating |

|---|---|---|---|---|

| Assureful | Pay-as-you-sell from $26/mo |

A-rated underwriters Instant quotes & certificates Covers imported goods Auto compliance docs Cancel with 30 days' notice |

Amazon, Shopify, eCommerce sellers needing automated, compliant, scalable coverage | 4.8/5 |

| Nationwide | Annual or monthly from $42/mo |

A-rated underwriters Online quotes Broad BOP options Customizable coverage Low complaint rate |

Multi-channel businesses wanting bundled coverage and strong service | 4.5/5 |

| Progressive | Annual or monthly from $57/mo |

A-rated underwriters Customizable BOP Online quotes redirect Wide platform support |

Retailers needing package policies and agent support | 4.2/5 |

| Chubb | Annual (monthly may be available) from $42/mo |

A++ underwriter High policy limits Custom cyber/product options Strong claims reputation |

Established brands, higher sales volume, global sellers | 4.0/5 |

Billing Model and Quote Process

Traditional insurers ask for a full year’s sales estimate and upfront payment or fixed installments. This approach penalizes seasonal sellers and anyone with unpredictable revenue. The better option: pay monthly based on actual sales, no annual forecasts, no lumpy bills, and policy changes that keep pace with your store. Avoid providers that hide quotes, delay with agent calls, or insist on annual minimums. Assureful’s pay-as-you-sell model leads here if your revenue fluctuates or spikes seasonally.

Product Liability Depth and Exclusions

Product liability coverage varies. Top eCommerce policies cover injuries, property damage, and legal defense for every product you list, including imports and private label. Watch for exclusions, many legacy policies quietly rule out imported or drop-shipped goods, which blocks most Amazon and Shopify sellers. If you spot vague language or a list of “excluded products,” clarify before you buy. True eCommerce insurance spells out included platforms and goods in writing.

Aggregate Limits and Policy Flexibility

Aggregate limit: the maximum your insurer pays for all claims in a policy year. For eCommerce, $1M per occurrence and $2M aggregate is standard. Good coverage lets you bump these up for a modest premium increase, often only 10-20% more. Watch for low per-incident or aggregate caps, or policies that don’t scale as your business grows. Flexible plans auto-adjust when you hit platform milestones (think Amazon’s $10k/month rule), so you stay covered and compliant.

Platform Integrations and Automation

- Direct integration with Amazon, Shopify, or Walmart for real-time sales data, reduces manual errors

- Automated compliance certificates sent as needed, cuts risk of account suspension

- One-click access to policy docs and claims status

- No annual sales projections or paper forms

- Red flag: Providers that don’t automate compliance docs or require calls for every change

Cancellation and Customer Support

Insurance should be flexible. Cancel any time with 30 days’ notice, no penalties. This protects you if your business pivots or contracts. Digital support (email, chat, phone) is a must. Some sellers still want traditional agent relationships. Avoid annual-only policies that penalize early cancellation or bury admin fees in contracts.

Comparing by these features, not just price, helps you spot hidden exclusions and compliance risks. For a closer look at cost ranges and policy differences, see our guide on what to expect to pay for general liability insurance and our analysis of key eCommerce insurance provider differences.

Best Ecommerce Insurance Providers for 2026: Honest Reviews and Real-World Fit

Assureful takes the lead for new and growing ecommerce sellers who need stress-free insurance, instant compliance, and pay-as-you-sell billing. Its flexible pricing, automated compliance, and true month-to-month terms solve cash flow and regulatory pain points that traditional options rarely address.

Assureful: Best for Flexible, Sales-Based Premiums and Fast Compliance

- Pay-as-you-sell billing: Premiums adjust monthly based on your actual sales, so there’s no need for upfront forecasts or large annual prepayments. Pricing starts at $26/month, ideal for early-stage stores and sellers with seasonal swings.

- Instant compliance: Direct integration with Amazon, Shopify, and Walmart auto-issues compliance certificates, cutting admin burden and suspension risk.

- Covers imported goods: Assureful insures stores selling imported or private-label products, coverage often excluded elsewhere.

- A-rated underwriters: Protection meets marketplace requirements in all 50 states.

- No annual contract: Cancel with 30 days’ notice. No hidden admin fees or penalties.

Assureful is built specifically for ecommerce. If you run a physical storefront, offer in-person services, or need bundled auto or workers’ comp, you’ll need a broader provider. Claims are handled digitally, efficient, but some may miss a dedicated agent. For real-world pricing examples, see our guide to eCommerce insurance costs.

Embroker: Best for Fast Digital Quotes and Broader Product Suite

Embroker targets sellers who want quick digital quotes and the option to bundle coverage types. General liability quotes take minutes. Add cyber or professional liability, or even directors & officers coverage if you’re growing across platforms. The online portal is clean and straightforward.

Limitations include brokered (not direct) policies, placement may be with third parties, though all are A-rated. Monthly billing isn’t usage-based, and imported or private-label goods aren’t always covered. Works well for sellers wanting multiple policy types in one place, or those prioritizing digital access over strict usage-based billing.

The Hartford: Best for Financial Stability and Broad Coverage Needs

The Hartford brings a long track record and a full suite of business coverages. Larger sellers needing to bundle commercial property, workers’ comp, or business interruption with liability find strong options here. Known for claims support and high financial ratings.

Drawbacks: Quotes take longer, and cancellation or refunds can require more steps. Entry premiums are higher, and annual contracts are standard. Suited to established businesses seeking traditional underwriting and coverage beyond pure online sales risks.

Next Insurance: Best for Small Sellers (but Less Specialized for eCommerce)

Next Insurance offers affordable general liability for micro-sellers and freelancers. Instant certificates, a simple online dashboard, and coverage in all 50 states. Can flex to cover some pop-up or event sales.

The trade-off: Next is designed for very small business risk. You won’t find support for product importation or seasonally spiking ecommerce revenue, nor integrations with sales platforms or pay-as-you-sell billing. Choose this for modest volume, mostly domestic goods, and straightforward liability protection.

Markel: Best for Niche Products and Custom Liability Add-ons

Markel fits stores selling higher-risk or specialty products. Selling supplements, toys, or products with strict safety requirements? Markel’s underwriters have deep specialty experience. You can add endorsements for product recall, professional services, or event liability.

Downsides: Pricing can jump for higher-risk lines, and some import origins or private-label products may be excluded. Quotes are usually handled by agents, so onboarding takes longer, but you get more tailored coverage for complex risks.

Each provider fits a specific seller profile and risk appetite. For a side-by-side comparison, see our guide to comparing eCommerce insurance providers and see how coverage, claims, and compliance stack up.

Common Ecommerce Insurance Mistakes: How New Sellers Get Burned

The costliest mistake for new online sellers? Expecting your home, renters, or personal umbrella policy to cover your ecommerce business. It won't. One product liability or cyber claim can drain your finances fast. Without dedicated coverage, lawsuits or regulatory fines land squarely on you.

Assuming Marketplace Compliance Means Full Coverage

Meeting insurance requirements for Amazon or Shopify doesn’t mean your business is protected. Marketplace minimums often ignore key risks, data breaches, lost inventory in transit, or supply chain breakdowns. Many sellers only find out after a claim that their policy excludes imported or drop-shipped goods. The result: denied claims when you need coverage most.

Check that your policy matches your sales model and product sources. Review exclusions for imported, private label, or drop-shipped items. Ask if your policy is fully compliant for marketplace sales and clarify what happens if a product causes harm after reselling or exporting.

Underestimating Cyber and Data Breach Exposure

Storing customer emails, payment data, or addresses puts a target on your back. Small businesses take nearly 43% of cyberattacks, and a breach often costs $50,000 or more in notification and legal fees, far more than most expect. Attacks aren’t limited to big brands. One missed security update or weak password can open the door. General liability policies won’t cover these losses.

Add cyber liability coverage. Many sellers pay $250, $500 per year for protection, less than the cost of a single breach. Choose a policy that covers breach notification, forensics, legal costs, and business interruption, not just data restoration. If you store significant customer data, make sure your limits match your database size and business interruption waiting periods are practical.

Choosing Annual Contracts That Don’t Scale With Sales

Annual insurance based on sales forecasts often backfires. Revenue surges or dips? You end up overpaying or underinsured. Upfront premiums strain cash flow, especially for new or seasonal stores. Expanding SKUs or selling on new platforms mid-year? That can force expensive endorsements or leave you out of compliance.

- Use monthly, pay-as-you-sell billing. Premiums match your real sales, not last year’s guess.

- Pick a provider with direct marketplace integration (like Assureful) so coverage and compliance auto-adjust as you grow.

- Read cancellation terms closely, some insurers lock you in or charge high penalties for changes.

Ignoring Policy Exclusions and Claims Support

Grabbing the cheapest policy or whatever checks a compliance box can backfire. Policies often hide exclusions, no coverage for imported goods, no cyber protection, or no coverage for fulfillment partners. When claims hit, those limitations leave you exposed. Weak claims support means delays or denials when you need help fast.

Read every exclusion and claims clause before buying. Ask about support for supply chain interruptions and inventory in transit. If you’re unsure what your policy covers, request sample wording or compare options using our guide on legal and financial mistakes that trip up owners. Solid claims support and clear terms protect you when things go wrong.

Which Ecommerce Insurance Should You Pick? Our Direct Recommendation for Every Scenario

For new online sellers on Amazon, Shopify, or those importing products, Assureful is the strongest fit. You get stress-free insurance that’s fully compliant, billed monthly, and tied to your actual sales, no annual forecasts or upfront costs. Coverage syncs with major platforms and typically costs less than traditional policies. It’s built for eCommerce from the ground up.

- Need instant, adjustable, platform-integrated coverage without annual sales projections? Go with Assureful for pay-as-you-sell billing and A-rated underwriters.

- Running a high-revenue operation and looking for bundled solutions, like workers’ comp, property, or commercial auto? Pick The Hartford for broad coverage and reliable claims support.

- Operate across multiple niches or want startup-friendly, customizable bundles? Embroker provides flexible packages and supports risks outside standard retail.

- Only require basic general liability for a small, single-channel shop? Thimble offers low-friction, short-term coverage with monthly or on-demand options.

- Sell professional expertise or consulting plus products? biBerk covers both product and professional liability under one policy.

For most Amazon, Shopify, or marketplace sellers, Assureful’s pay-as-you-sell policy gives you the most cost-efficient, compliant, and scalable coverage. Skip annual audits, keep cash flow steady, and cancel with 30 days’ notice if your business shifts. Get your instant quote and coverage online. If you expand into new categories or platforms, your protection updates automatically. Most eCommerce sellers should start here, adding other coverages only as your business grows or needs become more complex.

Start With Stress-Free, Adaptive Insurance, And Scale As Your Store Grows

Assureful’s pay-as-you-sell insurance is the clear starting point for Amazon, Shopify, and marketplace sellers. Coverage adjusts automatically to your monthly sales. You avoid overpaying in slow periods and don't risk being underinsured during busy spikes. No annual forecasts. No upfront surprises. This structure meets major platform requirements and closes liability gaps that new sellers often miss.

Flexibility matters most. Traditional policies lock you into yearly estimates and upfront payments. If sales climb or your business shifts, you’re stuck, or penalized. With Assureful, you pay for what you sell. Coverage keeps pace as you add products, enter new channels, or hit higher volume. Most sellers find this model keeps costs predictable and helps avoid compliance headaches or denied claims, essential if you import, expand, or launch new lines.

Start with monthly pay-as-you-sell coverage for stress-free protection. As your store grows, reassess and add coverage, like cyber or property, when risks change. Get your instant quote and see how adaptive insurance prevents common mistakes. For more ways to reduce costs, see our guide on lowering liability premiums or check when public liability coverage fits your business model.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreFrequently Asked Questions

What happens if I make a claim, how does the process work?

Filing a claim is a formal request for your insurer to pay a covered loss; the insurer assigns a claims adjuster who inspects the loss, applies your policy language and the state’s laws, and values the claim using depreciation tables, market values, or medical billing reviews. The company then issues a payment (often an initial advance), a partial offer, or a denial, health providers often file electronic health claims for you, while you must file auto/home claims, and payouts are subject to your deductible and policy limits. If you disagree, use the carrier’s internal appeal, file a complaint with your state insurance department, or hire counsel (for example, Michigan’s statute of limitations for most injury suits is three years).

Do I need other types of insurance, like cyber or commercial auto, in addition to product liability?

Yes, beyond product liability you will often need other policies depending on your operations. For example, cyber liability is critical if you handle customer data or run an online store (nearly 43% of cyberattacks target small businesses), commercial auto is required in most states if you or employees use vehicles for business, and workers’ compensation is mandatory if you have employees. Marketplaces like Amazon and Walmart commonly require $1M+ liability limits and additional-insured endorsements, and you may also need recall, inland marine or umbrella coverage, ask a licensed agent to tailor limits to your risks.

How are my pay-as-you-sell premiums calculated, which factors (product category, sales volume, claims history, imports) most affect my monthly rate?

Your monthly premium is driven first by actual sales volume (premiums are billed each month on your reported sales, not forecasts), and second by the rate attached to each product category (higher‑risk product classes carry higher per‑$ rates). Claims history functions like an experience modifier (raising or lowering the calculated premium); imported or marketplace‑sold products typically increase the per‑$ rate or trigger underwriting surcharges or endorsements. Conceptually: premium ≈ (product‑class rate per $100 of sales) × (monthly sales/100) × (experience modifier) + any import/marketplace loadings, taxes and fees.

Does the policy cover returns, shipping damage, or inventory losses while in transit or stored at a third‑party logistics provider (e.g., Amazon FBA)?

No, a standard BOP/commercial property policy generally does not automatically cover returns, shipping damage, or inventory stored at a third‑party (e.g., Amazon FBA); you need inland marine/cargo (transit) coverage for those risks. Inland marine/cargo or transit insurance specifically covers goods in transit and at third‑party locations and typically protects against theft, vandalism, fire, water, wind/hail and shipping accidents. Review your 3PL/carrier contracts and add an inland marine endorsement or separate transit policy because carrier liability limits often won’t fully cover losses.

If I sell to customers overseas, does my product liability cover claims filed in other countries or only domestic (U.S./home country) claims?

Depends, product liability covers only the countries listed in your policy’s "territory" clause: some policies are expressly "worldwide" while others limit coverage to the United States (often stated as "the United States of America, its territories and possessions, and Canada") or exclude specific foreign jurisdictions. Check your declarations page, the territory/exclusions language, and whether the policy will pay defense costs and judgments entered by foreign courts; many U.S. policies require an endorsement or a separate International Product Liability or local-market policy to insure overseas claims. Consult your broker and review customer/distributor contracts and local legal requirements before exporting, because insurers can refuse coverage or limit payment for foreign judgments without prior agreement.

Are product‑related intellectual property or advertising claims (e.g., trademark or copyright infringement from private‑label items) covered, or do I need separate IP/advertising injury protection?

No, product‑liability policies typically exclude intellectual property and advertising‑injury claims, so trademark or copyright suits from private‑label items are not covered. You need separate protection such as "personal & advertising injury" coverage on a CGL or a dedicated media/IP liability (intellectual property) policy or endorsement, and you should confirm specific IP exclusions and limits with your insurer.

Does insurance cover product recalls and the associated costs (customer notifications, shipping replacements, disposal), or is recall expense coverage separate?

No, standard product liability or commercial general liability policies generally do not pay for voluntary recall costs (customer notifications, shipping replacements, disposal); those expenses are typically excluded. Product‑recall (withdrawal/contamination) expense insurance is sold separately as a standalone policy or endorsement and specifically covers notification, transportation, storage/disposal, replacements, testing and crisis‑management costs but carries its own limits, sublimits and conditions. Liability policies will still cover third‑party bodily injury or property‑damage claims (and related defense), but not the insured’s recall logistics unless recall coverage was purchased.

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to two-minute insurance quiz.

Related: Do Deductibles Reset Every Year? A Renewal Checklist To Avoid Surprise Costs.

Related: How Much Is $20 Million Public Liability Insurance? A Checklist.

Sources

- assureful

- well-insurance.com

- flashpricer.com

- uhc.com

- insureon.com

- insureon.com

- checklistguro.com

- hubinternational.com

- 1800insurance.com

- uschamber.com

- uschamber.com

- quora.com

- hubinternational.com

- baldwin.com

- hulettinsuranceblog.com

- nchinc.com

- allenmatkins.com

- travelers.com

- fitsmallbusiness.com

- vouch.us

- hotalinginsurance.com

- shopify.com

- rangeme.com

- forbes.com

- nextinsurance.com

- assureful.com

- mailchimp.com

- seo-pages-web.vercel.nerdwallet.com

- nerdwallet.com

- moneygeek.com

- policyape.com

- esportsinsurance.com

- fastercapital.com

- insureon.com

- progressivecommercial.com

- aami.com.au

- geico.com

- thehartford.com

- insureon.com

- progressivecommercial.com

- progressivecommercial.com

- forbes.com

- business.libertymutual.com

- swoopfunding.com

- insureon.com

- insureon.com

- cyberpolicy.com

- bankrate.com

- swoopfunding.com

- insurify.com

- taxjar.com

- cnbc.com

- cnbc.com

- embroker.com

- thehartford.com

- landesblosch.com

- moneygeek.com

- payoneer.com

- ecom.insure