A seller ships 500 units via personal vehicle to a local retailer. On the way, they hit another car. Their personal auto insurer denies the claim, business use isn't covered. The other driver sues. The seller pays $47,000 out of pocket for injuries and property damage. Their personal auto policy? Worthless. Their business assets? Now at risk. This scenario plays out dozens of times a year because sellers confuse personal auto insurance with commercial coverage.

Pay-as-you-sell general liability insurance designed specifically for eCommerce. Premiums starting from just $26 per mon...

Premiums from $26/month

Learn MoreWhy Commercial Auto Coverage Is A Real Risk For eCommerce Sellers - Not Just Trucking Companies

Your personal auto insurance explicitly excludes business use. A single delivery run in your own vehicle to move inventory or fulfill a local order could leave you personally liable for an accident - with no coverage and no protection from your insurer.

This gap isn't limited to logistics companies with dedicated fleets. Any eCommerce seller who drives a personal or business vehicle for inventory transport, deliveries, or business errands crosses into commercial territory the moment the trip serves a business purpose. Most sellers this coverage gap only after an incident occurs.

This guide walks you through when commercial auto liability becomes your responsibility, what it costs, and how it fits into your broader insurance strategy. You'll also explore how commercial auto coverage works alongside other protections and whether it's a requirement for your operation. Whether you're deciding if you need insurance for your ecommerce business or already managing multiple policies, understanding this exposure is essential to protecting both your business and personal assets.

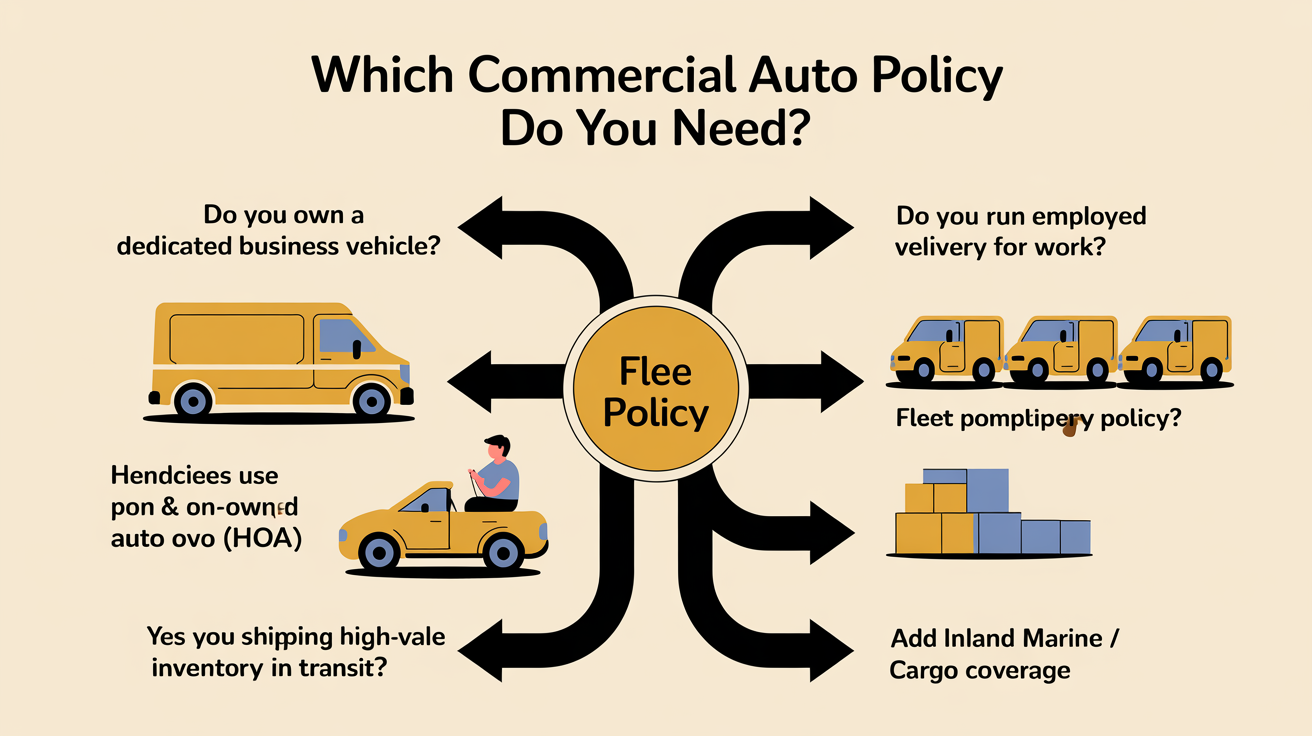

The Main Types Of Commercial Auto Coverage eCommerce Sellers Encounter

Commercial auto insurance comes in four distinct types. Each one covers different business structures and vehicle ownership scenarios.

Standard Commercial Auto - For Business-Owned Vehicles

This is the foundational policy for any eCommerce seller who owns a vehicle used for business purposes. Whether you're driving a van to pick up inventory, making local deliveries, or transporting goods to fulfillment centers, a standard commercial auto policy covers vehicle damage, bodily injury, and third-party liability from accidents that occur during these business trips.

Personal auto insurance explicitly excludes business use. The moment your vehicle is "on the clock" for inventory transport or deliveries, your personal policy won't respond to a claim. A standard commercial auto policy fills that gap by insuring the vehicle itself and protecting you from lawsuits if you cause an accident.

Hired And Non-Owned Auto - For Employee And Rental Vehicle Exposure

If your employees use their personal vehicles for business errands - picking up supplies, collecting returns, or making local deliveries - you have liability exposure even though you don't own the vehicle. Hired and non-owned auto coverage explains when your store needs this protection and how to add it to your existing business policy.

This coverage is typically purchased as an add-on (called an endorsement) to your commercial auto or general liability policy. It protects your business from lawsuits arising from accidents in employee personal vehicles or rented vehicles used for work. Without it, an accident in an employee's car could create a gap between their personal coverage and your business liability.

Fleet Policies - For Multiple Business Vehicles

As your eCommerce operation scales and you add multiple delivery vans or inventory transport vehicles, a fleet policy becomes more cost-effective than insuring each vehicle individually. Fleet policies simplify administration and often offer better rates as your vehicle count grows.

Small business auto insurance cost guides for fleet vs individual pricing help you determine when consolidating into a fleet policy makes financial sense. Most carriers recommend fleet coverage once you reach three or more vehicles, though this varies by insurer and your local market.

Inland Marine And Cargo Coverage - Goods In Transit

Commercial auto insurance covers the vehicle and liability from accidents, but not the goods inside. If inventory is damaged, lost, or stolen while in transit, that's a separate coverage area called inland marine or cargo insurance.

This distinction matters because a collision that damages both your van and the products inside requires two separate claims - one under commercial auto and one under cargo coverage. Many eCommerce sellers overlook this gap until they experience a loss and realize their vehicle policy doesn't cover the merchandise. A $15,000 shipment damaged in a collision leaves you paying the full amount out of pocket unless you have cargo coverage in place.

4 Practical Decisions Every Seller Faces When Choosing Commercial Auto Coverage

Before you buy commercial auto insurance, you need to answer four core questions about your operation and location. These decisions determine which coverage types you need, how much you'll pay, and whether you're actually protected when a claim happens.

Decision 1: Do You Own the Vehicle or Use Personal and Rented Vehicles?

If you own a delivery van or cargo truck registered to your business, you need a standard commercial auto policy. That policy covers liability and physical damage for vehicles you own and operate.

But if your employees or you drive personal vehicles for business errands - picking up inventory, making local deliveries, returning items - your personal auto insurance won't cover business use. You'll need hired and non-owned auto coverage as an add-on endorsement to fill that gap. This extension protects you from liability claims when someone drives a vehicle your business doesn't own. Without it, an accident in an employee's personal car could leave you exposed to a lawsuit that neither their personal policy nor your business policy covers.

Decision 2: Do Your Employees Drive for Business?

Every employee with a valid license is typically covered as an additional insured under your commercial auto policy when they drive a company vehicle. But their driving history, claims record, and the frequency of vehicle use affect your premium.

If employees regularly drive for deliveries, client visits, or supply runs, you should expect higher premiums than a business with occasional vehicle use. Some insurers also factor in motor vehicle reports (MVR) for your key drivers. Be ready to provide employee names and driving histories when you apply, and notify your insurer if driver rosters change significantly.

Decision 3: How Much Inventory Do You Ship and What's Its Value?

Commercial auto insurance covers the vehicle and your liability for accidents, but not the goods inside. If you transport $5,000 worth of inventory and it's damaged, stolen, or lost in transit, your auto policy won't cover the merchandise - only the vehicle damage and third-party liability.

As your eCommerce business scales and you add local delivery or inventory transport, you need to decide whether to add inland marine or cargo coverage alongside your auto policy. This becomes critical if you regularly transport high-value products. Without it, a collision that damages both your van and its contents leaves you paying out of pocket for the inventory loss.

Decision 4: What Are Your State's Minimum Requirements and How Do Rates Compare?

Every state sets minimum liability limits for commercial vehicles. Some states require as little as $15,000 bodily injury per person, while others mandate $25,000 or higher. Your state, vehicle type, and industry classification all affect your baseline premium.

Rates for identical coverage vary by 30 to 40 percent between insurers, making comparison essential before you commit. How quotes really differ across carriers and coverage tiers shows you where savings actually hide. Once you know what type of policy you need, how to evaluate quotes from multiple providers walks you through the comparison process so you don't overpay for the same protection.

If your business is adding local delivery as a growth channel, review your coverage immediately. That operational shift triggers higher liability exposure and may require additional coverage types or higher policy limits than your current setup provides.

5 Commercial Auto Mistakes That Leave eCommerce Sellers Exposed

Personal auto insurance explicitly excludes business use. If you're delivering orders in your own car without commercial coverage and cause an accident, your insurer will deny the claim - leaving you personally liable for injuries, property damage, and legal fees. This single mistake costs sellers tens of thousands of dollars.

Here are the five most common and costly errors in commercial auto coverage:

- Using personal auto for business deliveries. Personal policies exclude commercial activity, triggering claim denials even for a single delivery run.

- Skipping hired or non-owned auto coverage (HNOA) when employees use their own cars for business. One employee errand without HNOA creates uninsured liability exposure.

- Confusing cargo or inland marine insurance with commercial auto. Commercial auto covers vehicle and bodily injury liability, not the inventory inside the vehicle - a gap that costs you the full value of damaged goods.

- Underinsuring a growing fleet. Sellers who add vehicles without updating their policy face coverage gaps and potential denial of claims on the new vehicle.

- Buying low-cost commercial auto without reading exclusions. Cheap policies often exclude hired vehicles, multi-driver scenarios, or specific business uses, leaving you exposed when you need coverage most.

The most damaging pattern is buying insurance piecemeal rather than as part of a coordinated coverage plan. You may have one policy covering your warehouse liability but a completely separate auto policy with conflicting exclusions. When a claim spans both areas - a delivery accident involving inventory, for example - neither policy pays because each one points to the other.

Review what cheap commercial auto policies actually exclude to understand where your coverage really ends. Then use nine key questions before you buy to audit your current setup and close gaps before they cost you.

Where To Start Based On How Your Business Moves Its Products

Your next step depends on whether you already move products yourself or plan to soon.

If you use your own vehicle for occasional deliveries or customer pickups, start by reading about hired and non-owned auto coverage. This single policy closes the gap between your personal auto insurance and business liability.

If you operate a dedicated delivery fleet or are comparing quotes across multiple insurers, focus on understanding the cost differences between covering individual vehicles versus a full fleet. This reveals where you'll actually save money as you scale.

If you're still deciding whether commercial auto makes sense for your operation at all, start with how product and general liability affect your online store's bottom line. That foundation matters first, because many sellers need general liability coverage before they need commercial auto. Understanding the distinction prevents you from buying the wrong policy in the wrong order.

Once you've picked your starting point and understand which risks each policy covers, layer in commercial auto as your fulfillment operations grow. General liability insurance - the kind built specifically for eCommerce sellers - starts at $26 per month with pay-as-you-sell billing that adjusts to your actual sales. That's your foundation. Commercial auto is the next logical step once you're moving inventory yourself. Stress-free insurance starts with knowing which policy covers which risk, and these articles help you make that distinction clear.

Frequently Asked Questions

Rohit Nair is the CEO and Founder of Assureful, an insurtech venture creating smart insurance products for ecommerce businesses. With a track record of launching and scaling successful ventures across health, wellness, ecommerce and consumer technology, with multiple exits and acquisitions, Rohit brings deep expertise in financial management, regulatory environments, and high-growth startups.

For more on this topic, see our guide to eCommerce business insurance.

Related: What Is Not Covered By The Commercial General Liability (CGL).

Related: How Much Is Commercial General Liability Insurance? What It Covers.

Sources

- nextinsurance.com

- constructioncoverage.com

- nationwide.com

- levertylaw.com

- directauto.com

- thehartford.com

Next best step

Match the article to the buying page.

If you are comparing coverage or preparing for a quote, start with the page that matches where you sell and what you sell.

eCommerce insuranceFull buyer's guide for online sellers.Amazon seller insuranceProof of insurance and COI guidance for third-party sellers.Shopify insuranceCoverage planning for Shopify and DTC brands.Product liability by stateState-specific product liability context and requirements.Compare insurersSee how Assureful compares with traditional carriers.

Related buying paths

Find the category page behind the risk.

Amazon categories

Product liability guides for Amazon sellers

Shopify categories

Product liability guides for Shopify brands

Best-fit comparisons